Strengthening ESG Controls: A Practical Guide for 2026

Every compliance officer, risk leader, CTO, and CEO knows that ESG reporting is no longer a “nice-to-have.” Your stakeholders, from investors to auditors, demand reliable, defendable, and transparent disclosures that stand up to scrutiny.

But when controls are informal, owners are unclear, and evidence is scattered across spreadsheets and inboxes, your ESG reporting becomes fragile and reactive instead of strategic and predictable.

You scramble to gather evidence. You risk investor distrust and audit objections. In today’s climate, 76% of investors say they trust sustainability information more when it is independently assured. Built on strong controls, your ESG metrics can become accurate, consistent, and audit-ready.

In this blog, we will define ESG controls, outline a strong control framework, walk through a step-by-step build approach, and explain how to test and monitor for ongoing reporting excellence.

Key Takeaways

- Strong ESG controls make reporting accurate, transparent, and audit-ready.

- Tailored controls for high-risk metrics and data patterns reduce errors.

- Clear governance and cross-functional ownership ensure accountability.

- Centralized evidence and monitoring keep metrics defensible and traceable.

- VComply operationalizes controls across all GRCOps, reducing manual work.

Did you know? Over 90% of investors surveyed believe corporate sustainability reporting contains unsupported or questionable claims, and about 85% say that if ESG disclosures were assured at the same level as financial audits, it would significantly boost their confidence in that data.

What ESG Controls Mean In Real Reporting Work

ESG controls define how you keep sustainability data dependable when it is reviewed, questioned, or examined. For compliance leaders, they turn ESG reporting from a narrative exercise into a governed, repeatable process that supports oversight, internal review, and external assurance expectations across state-regulated operations.

Below are the core components that make ESG controls work in practice.

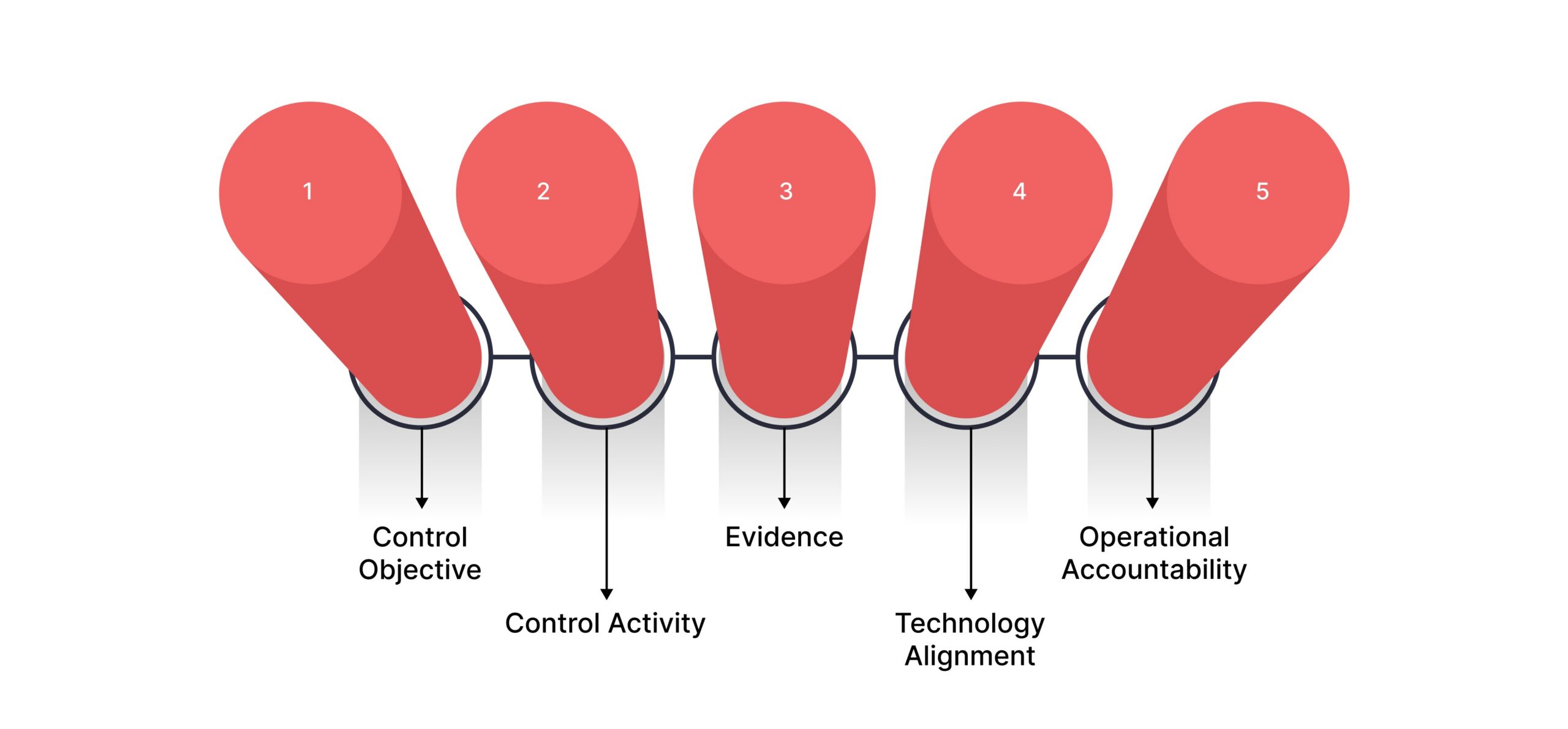

- Control Objective: The specific outcome the control is designed to achieve. In ESG reporting, a control objective may ensure emissions data is complete for all regulated entities or that social metrics align with approved definitions across states.

- Control Activity: The action you perform to meet the objective. Examples include management reviews of ESG calculations, required approvals before disclosures are finalized, or automated checks that flag missing or inconsistent data.

- Evidence: The documentation that proves the control operated as intended. This includes review sign-offs, calculation files, system logs, or approval records that stand up during audits or regulatory exams.

- People, Process, and Technology Alignment: ESG controls function across teams, workflows, and systems. Compliance, risk, finance, operations, and IT all play defined roles, with technology enabling accountability, consistency, and traceability at scale.

- Operational Accountability Across Reporting Cycles: Effective ESG controls assign ownership, frequency, and escalation paths, ensuring controls operate continuously rather than only at reporting deadlines.

With a clear understanding of what ESG controls entail, it’s important to see why they have become a board-level risk issue, demanding attention from leadership, auditors, and regulators alike.

Why ESG Controls Are Becoming A Board-Level Risk Issue In The US

ESG disclosures in the United States have moved beyond storytelling. Boards now view them as decision-grade information that influences capital allocation, regulatory confidence, and organizational credibility. Below are the reasons ESG controls now demand board-level attention.

- Disclosure Defensibility For Compliance Leaders: You are expected to demonstrate how ESG figures were produced, reviewed, and approved. Without structured controls and retained evidence, disclosures become difficult to defend during regulatory exams or assurance reviews.

- Risk Visibility For Enterprise Risk Leaders: ESG introduces new operational, climate, and social risks that require identification, monitoring, and escalation. Controls connect these risks to ownership and ongoing oversight instead of one-time assessments.

- System Integrity for Technology Leadership: ESG reporting relies on multiple data sources. Boards increasingly ask how data flows between systems, who has access, and how changes are tracked to prevent errors or unauthorized updates.

- Confidence and Predictability For Executive Leadership: CEOs need assurance that ESG disclosures will not trigger investor concerns or last-minute revisions. Strong controls reduce surprises and support consistent, board-ready reporting.

Also Read: ESG Disclosure Requirements in Canada: CSA and OSFI Compliance Explained

Given the growing board-level focus on ESG risks, organizations are turning to established control frameworks as a starting point to bring structure, consistency, and credibility to their reporting processes.

The Control Framework Most Teams Use As A Starting Point

When ESG reporting matures, most organizations look for a control structure that regulators, auditors, and boards already recognize. Rather than invent new governance models, teams adapt established internal control frameworks to bring consistency, discipline, and credibility to ESG reporting processes.

Below is how COSO-based internal control thinking supports ESG control design.

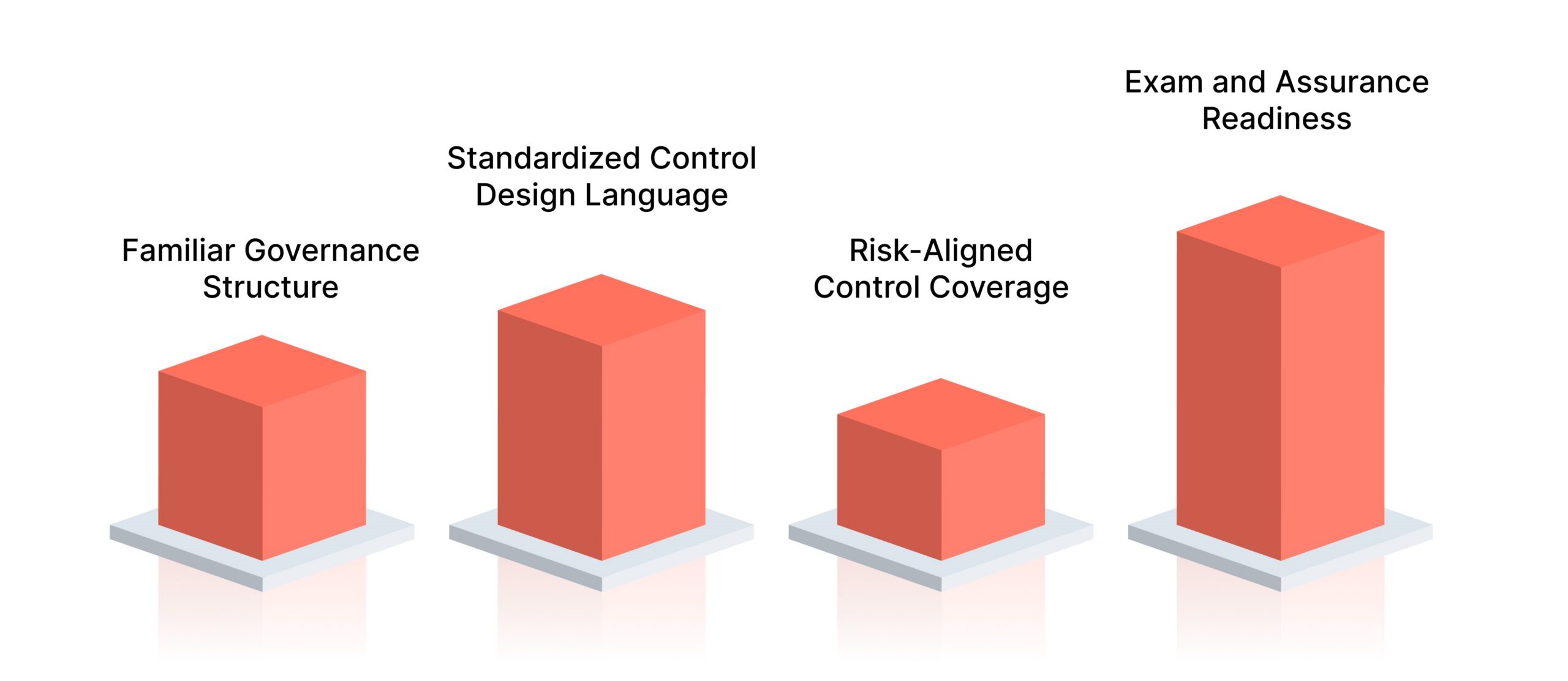

- Familiar Governance Structure: COSO principles align with frameworks already used for financial reporting and operational oversight. This familiarity helps you extend existing governance practices to ESG without retraining leadership or redefining accountability.

- Standardized Control Design Language: Using COSO terminology allows you to define ESG controls with clear objectives, activities, and monitoring expectations. This standardization improves clarity during internal reviews and external assurance discussions.

- Risk-Aligned Control Coverage: The framework encourages you to identify ESG risks first and then design controls that directly address them. This approach ensures controls focus on material exposures rather than generic checklists.

- Exam and Assurance Readiness: COSO-based controls create documentation and evidence structures that support exam inquiries and assurance testing, reducing the effort required to explain how ESG data is governed.

VComply Risk Ops helps you map ESG risks to owners, track exposure across business units, and monitor issues continuously. With automated alerts for high-impact metrics and a centralized view of risk trends, your team can act before issues escalate, ensuring board-level confidence in your ESG reporting.

The Five Control Components Applied To ESG Reporting

Applying internal control components to ESG reporting helps you move from ad hoc coordination to disciplined execution. These components provide a practical way to manage ESG data with the same rigor expected in other regulated reporting areas, while remaining adaptable to changing disclosure expectations.

Below is how each control component applies to ESG reporting in practice.

- Control Environment: Sets the tone for ESG accountability through defined policies, ethical expectations, and leadership oversight. For ESG reporting, this includes approved reporting principles, ownership structures, and clear expectations for data integrity.

- Risk Assessment: Identifies ESG-related risks that could lead to inaccurate, incomplete, or misleading disclosures. This step prioritizes controls around high-impact metrics, assumptions, and data sources across regulated entities.

- Control Activities: Establish the actions that prevent or detect reporting errors. Examples include management reviews, approval workflows, segregation of duties, and validation checks embedded into ESG reporting processes.

- Information and Communication: Ensures ESG data, methodologies, and control expectations are communicated consistently across teams. This includes standardized definitions, reporting guidance, and documented escalation paths.

While a solid framework provides structure, ESG controls can still fail in practice if gaps in ownership, evidence, or monitoring are not addressed.

Where ESG Controls Usually Fail

ESG reporting rarely fails because of intent. It fails because control structures do not keep pace with expanding disclosure scope and assurance expectations. Below are the most common control breakdowns you encounter in practice.

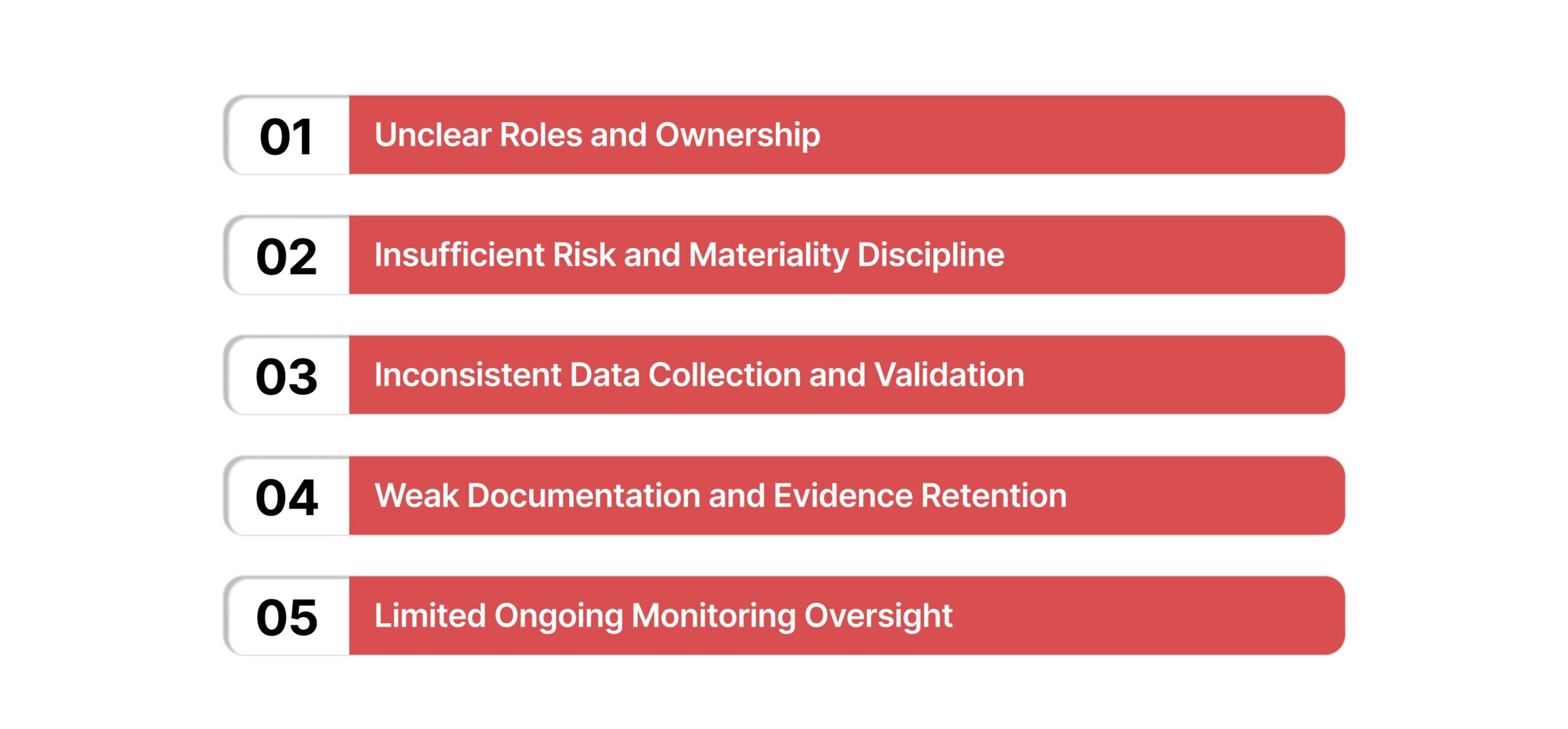

- Unclear Roles and Ownership: You lack formally assigned owners for ESG metrics and disclosures, leading to reliance on informal coordination and last-minute sign-offs that weaken accountability.

- Insufficient Risk and Materiality Discipline: ESG risks are identified at a high level but not translated into prioritized control requirements, leaving high-impact metrics without appropriate preventive or detective controls.

- Inconsistent Data Collection and Validation: Data is gathered using different methods across business units, with limited validation rules or review thresholds to identify anomalies before reporting deadlines.

- Weak Documentation and Evidence Retention: Supporting materials are stored across emails, shared drives, and spreadsheets, making it difficult to demonstrate how figures were reviewed, approved, or corrected.

- Limited Ongoing Monitoring Oversight: Controls are reviewed only near reporting deadlines, reducing visibility into recurring issues and increasing the likelihood of late-stage remediation.

These failures are fixable when you move to a structured, repeatable ESG control build.

Also Read: ESG Reporting Requirements for Renewable Energy Firms

Understanding where ESG controls commonly break down sets the stage for a practical, repeatable method to build stronger, more reliable controls.

Build ESG Controls Using A Practical, Repeatable Method

Building effective ESG controls does not require full maturity on day one. A phased approach allows you to establish control discipline early, strengthen weak areas over time, and support reporting confidence as expectations change.

Below is a staged method you can apply to build ESG controls systematically.

Step 1: Define Scope, Boundaries, and Material Topics

Effective ESG controls begin with clarity. Before you design controls, you need a shared understanding of what your organization is reporting, which operations are included, and which ESG topics truly matter.

Below is how to establish a defensible foundation for ESG controls.

- Define Reporting Scope Clearly: Identify which legal entities, business units, and regulated operations fall within ESG reporting. Scope decisions should reflect state-based licensing structures, operational footprints, and reporting obligations.

- Establish Operational and Value Chain Boundaries: Determine which internal activities and external touchpoints contribute to ESG data. This includes third-party administrators, vendors, and service providers that influence reported metrics.

- Identify Material ESG Topics: Focus on ESG areas that could influence stakeholder decisions or regulatory scrutiny. Materiality helps you determine where controls are required versus where lighter oversight is sufficient.

- Translate Materiality Into Control Priorities: Assign stronger controls, higher review frequency, and more detailed evidence requirements to material topics. Lower-risk areas can follow simplified control approaches.

- Document Decisions For Review and Assurance: Retain documentation explaining why certain topics and entities were included or excluded. This supports transparency during internal reviews and external examinations.

Step 2: Map The ESG Data Lifecycle End-to-End

Once scope and material topics are defined, you need visibility into how ESG data actually moves through your organization. Mapping the full data lifecycle exposes control gaps that remain hidden until reporting deadlines or exam requests force last-minute investigations.

Below is how to map the ESG data lifecycle with control relevance in mind.

- Identify All Data Sources: Document where ESG data originates, including operational systems, vendor reports, actuarial inputs, and third-party service providers supporting regulated entities.

- Define Collection Methods and Timing: Specify how data is gathered, who submits it, and when submissions occur. Inconsistent timing or manual handoffs often introduce completeness and accuracy issues.

- Document Calculations and Estimates: Capture how metrics are calculated, including assumptions, methodologies, and estimation techniques. This step is critical, where ESG metrics rely on judgment or proxy data.

- Map Review and Approval Handoffs: Identify each review point, approver, and escalation path. Errors frequently occur during handoffs when ownership or expectations are unclear.

- Align Reporting and Disclosure Outputs: Trace how reviewed data feeds dashboards, management reports, and external disclosures. This ensures reported figures reflect approved and finalized inputs.

- Define Retention and Traceability Requirements: Establish where data and evidence are stored, how long records are retained, and how they can be retrieved during exams or assurance reviews.

Step 3: Create A Risk and Controls Matrix For Priority Metrics

After mapping the ESG data lifecycle, you need a structured way to convert risks into enforceable controls. A risk and controls matrix creates discipline by linking each priority metric to ownership, evidence, and escalation, forming the foundation for consistent oversight and exam readiness.

Below is how to structure a defensible risk and controls matrix for ESG reporting.

- Define the Reporting Risk: Identify how a specific metric could become inaccurate, incomplete, or misleading. Risks should reflect operational realities, third-party dependencies, and judgment-based estimates.

- Set the Control Objective: Specify what the control is designed to prevent or detect. Clear objectives ensure controls address the actual risk rather than serving as generic checkpoints.

- Document The Control Activity: Describe the exact action performed, including reviews, validations, approvals, or reconciliations, along with how exceptions are handled.

- Assign Control Ownership and Accountability: Name the responsible owner and reviewer for each control. Clear accountability prevents delays and confusion during reporting cycles.

- Establish Frequency and Timing: Define how often the control operates and at what stage of the reporting process. This ensures controls run consistently, not only at period end.

- Specify Required Evidence: Document what proof demonstrates the control operated effectively, including reports, sign-offs, or system records.

- Define Escalation and Remediation Paths: Establish when issues must be escalated, who reviews them, and how remediation is tracked.

VComply’s Compliance Ops allows you to assign metric-level ownership, track control execution, and store evidence in one secure platform. By centralizing ESG control workflows, VComply ensures that controls operate consistently across reporting cycles, reducing manual work and audit preparation time.

Once ESG controls are built using a structured method, the next step is strengthening them in a way that maintains reporting efficiency and avoids unnecessary delays.

How To Strengthen ESG Controls Without Slowing Reporting

Strengthening ESG controls should make reporting smoother, not heavier. The most effective approach focuses on reinforcing high-impact areas first, where errors, judgment, or third-party data create the greatest reporting risk.

Below are targeted actions that strengthen ESG controls while protecting reporting timelines.

- Standardize Definitions First: Establish a single data dictionary that defines metrics, boundaries, assumptions, and calculation methods. Consistent definitions prevent rework and disputes during review and exam cycles.

- Assign Clear Ownership: Designate an owner, reviewer, and approver for each ESG metric and disclosure. Clear roles reduce delays and ensure accountability when issues arise.

- Build Evidence Into The Workflow: Require supporting documentation at the point of data submission. Capturing evidence early eliminates retroactive collection and strengthens audit defensibility.

- Add Exception Handling Controls: Define thresholds that trigger review when values deviate from expectations. Establish escalation paths and remediation steps to address issues before reporting deadlines.

- Automate Reminders and Approvals: Use automated notifications and approval workflows to replace manual follow-ups, reducing missed deadlines and dependency on informal coordination.

- Introduce Periodic Review Cadence: Apply monthly validation, quarterly management review, and final pre-release signoff to maintain continuous oversight rather than end-stage corrections.

Also Read: Why Policy Management is the Infrastructure of ESG

After learning how to reinforce ESG controls efficiently, it’s important to identify the core control types you should prioritize to stabilize reporting and ensure accountability from the start.

Core ESG Control Types You Should Design First

Before expanding ESG controls across the organization, you need a foundational control set that stabilizes reporting and supports oversight. Designing this core set first allows you to scale controls confidently without disrupting reporting cycles.

Below are the ESG control types most teams should prioritize early.

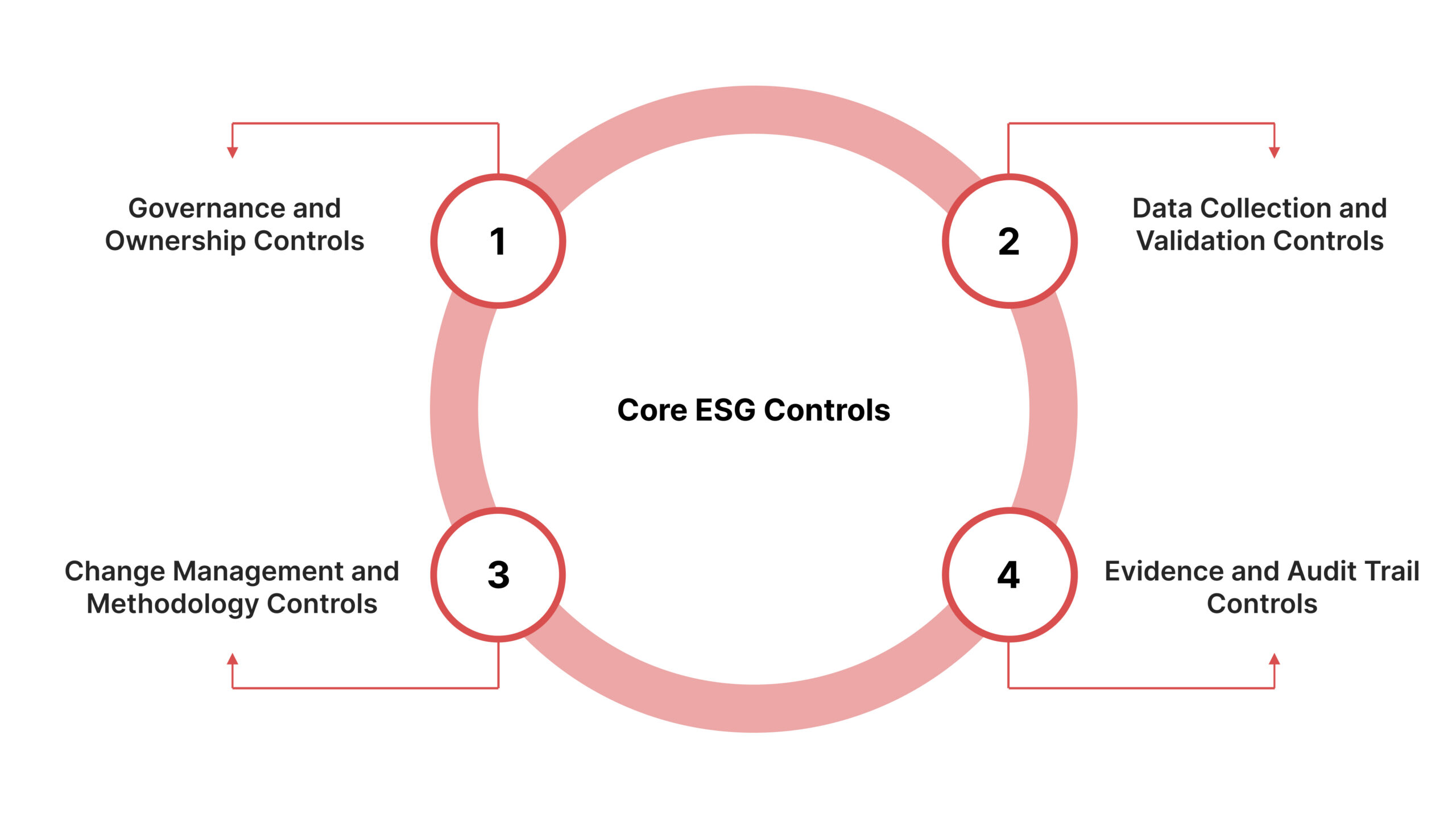

Governance and Ownership Controls

Governance and ownership controls establish who is responsible for ESG reporting decisions and how oversight is maintained throughout the reporting cycle. Below are the governance and ownership controls you should formalize first.

- Designate an ESG Reporting Owner: Assign a senior owner accountable for end-to-end ESG reporting outcomes. This role ensures alignment across functions and serves as the primary point of accountability during reviews and examinations.

- Assign Metric-Level Ownership: Name responsible owners for each ESG metric who understand data sources, assumptions, and operational dependencies. Metric owners manage accuracy and respond to validation or inquiry requests.

- Define Review and Approval Authority: Establish clear approvers for metrics and disclosures, including escalation paths when approvals are delayed or challenged.

- Set Oversight and Review Routines: Implement structured oversight meetings and review checkpoints to monitor progress, resolve issues, and approve changes before reporting deadlines.

- Formalize Cross-Functional Governance Expectations: Define the roles of compliance, risk, finance, sustainability, legal, operations, and IT. Clear expectations ensure coordinated execution, system integrity, and consistent application of controls across reporting cycles.

These controls create accountability structures that support reliable reporting and exam readiness.

Data Collection and Validation Controls

Data collection and validation controls protect ESG reporting from inconsistencies that often surface during reviews and exams. Below are the data collection and validation controls you should establish early.

- Standardized Data Input Templates: Use uniform templates that define required fields, formats, and units of measure. Standardization reduces interpretation risk across business units and regulated entities.

- Approved Metric Definitions and Assumptions: Require data submissions to follow approved definitions and assumptions. This prevents teams from applying inconsistent methodologies across reporting periods.

- Validation Rules and Tolerance Thresholds: Apply rules that flag missing, incomplete, or out-of-range values. Thresholds help you identify potential errors without reviewing every data point manually.

- Structured Review and Signoff Process: Implement defined review steps where submissions are evaluated for accuracy, completeness, and alignment with expectations before approval.

- Exception Identification and Resolution: Establish procedures for documenting, escalating, and resolving exceptions. Capturing how issues were addressed supports transparency and exam defensibility.

Change Management and Methodology Controls

Change management controls protect ESG reporting from unintended inconsistencies when assumptions, boundaries, or methodologies change. Below are the change management and methodology controls you should implement.

- Controlled Emission Factor Updates: Require formal review and approval before emission factors are updated. Document the rationale, effective date, and impacted metrics to preserve consistency.

- Boundary Change Governance: Establish approval requirements when reporting boundaries shift due to acquisitions, divestitures, or operational changes. Clear governance prevents unintended omissions or double-counting.

- Methodology Update Approval Process: Define when methodology changes are permitted and who must approve them. Require documentation explaining why the change was necessary and how it affects reported results.

- Version Control and Documentation Standards: Maintain versioned records of calculations, methodologies, and disclosures. Version control supports transparency and simplifies comparisons across reporting periods.

- Restatement and Correction Procedures: Implement structured processes to assess, approve, and document restatements. Retain evidence showing how issues were identified, corrected, and communicated.

Evidence and Audit Trail Controls

Evidence and audit trail controls determine whether your ESG reporting can withstand examination and assurance review. Below are the evidence and audit trail controls you should formalize.

- Define Acceptable Evidence Standards: Specify what qualifies as valid evidence, such as system reports, approval records, calculation files, or third-party attestations. Clear standards prevent inconsistent or incomplete documentation.

- Link Evidence To Metrics and Reporting Periods: Require evidence to be explicitly associated with the relevant metric, entity, and reporting period. This linkage supports efficient exam responses and assurance testing.

- Centralize Evidence Storage: Store all supporting documentation in a controlled, centralized repository. Centralization reduces retrieval time and limits the risk of lost or altered records.

- Enforce Retention Requirements: Establish retention periods aligned with internal policy and regulatory expectations. Retention standards ensure evidence remains available throughout review and examination cycles.

- Maintain Traceable Review and Approval History: Capture timestamps, reviewers, and approval decisions to demonstrate control over time. Traceability strengthens defensibility during audits and regulatory exams.

VComply’s GRCOps Suite integrates ComplianceOps, RiskOps, PolicyOps, and CaseOps in a single platform, enabling end-to-end GRC execution. Centralize evidence, track remediation, and gain real-time dashboards that keep your ESG disclosures accurate, traceable, and board-ready.

Now, it’s crucial to implement testing and monitoring processes to ensure ESG reporting remains accurate, consistent, and defensible over time.

Testing and Monitoring ESG Controls So Reporting Stays Defensible

Designing ESG controls is not enough. You need to demonstrate that those controls operate consistently over time. Testing and monitoring ensure that ESG reporting remains reliable between reporting cycles, withstands examination, and adapts as risks and expectations change.

Below is how to test and monitor ESG controls effectively.

- Differentiate Design and Operating Effectiveness: Design effectiveness confirms that the control is appropriately structured to address risk. Operating effectiveness demonstrates that the control actually ran as intended during the reporting period.

- Establish A Regular Monitoring Cadence: Apply monthly validation checks to identify issues early, conduct quarterly oversight to assess trends, and complete a final pre-release review before disclosures are issued.

- Document Control Testing Results: Record testing outcomes, identified issues, and remediation actions. Documentation supports transparency and provides a defensible record during exams and assurance reviews.

- Engage Internal Audit Strategically: Involve internal audit to perform independent testing, validate control design, and assess operating consistency without duplicating management activities.

Once ESG controls are tested and monitored, aligning them with existing SOX-style discipline can further strengthen consistency, accountability, and audit readiness.

Align ESG Reporting Controls With Existing SOX-Style Discipline

Many organizations already maintain SOX-based controls for financial reporting. You can understand this established infrastructure to bring the same rigor, accountability, and documentation standards to ESG reporting.

Below are practical ways to adapt SOX-style discipline to ESG reporting.

- Apply Disclosure Controls and Procedures to ESG Narratives: Use structured review and approval processes to ensure that narrative disclosures accurately reflect metrics, assumptions, and methodology changes.

- Implement Segregation of Duties for ESG Calculations: Assign separate individuals for data preparation, review, and approval of ESG metrics, reducing the risk of errors or unauthorized adjustments.

- Track Issues and Remediation Actions: Document control failures, assign owners for remediation, and maintain evidence of corrective actions to support audit and regulatory inquiries.

- Understand Existing Monitoring and Testing Protocols: Integrate ESG control testing into established SOX or internal audit cycles to streamline oversight and maintain consistent reporting discipline.

With ESG controls aligned to SOX-style discipline, the next step is seeing how a platform like VComply can operationalize these controls, centralize oversight, and ensure audit-ready reporting.

How VComply Helps You Operationalize ESG Controls For Reporting

For organizations, implementing ESG controls at scale requires a platform that centralizes ownership, evidence, and oversight while supporting repeatable, auditable processes. VComply serves as this execution layer, transforming ESG control management from fragmented spreadsheets into a structured, exam-ready system.

Below are the ways VComply operationalizes ESG controls effectively.

- Assign and Track Control Ownership Across Teams: Define responsibility for each ESG metric, control activity, and evidence submission. Assign due dates and escalation paths to ensure accountability across compliance, risk, finance, operations, and IT teams.

- Centralize Evidence Management and Audit Trails: Store all supporting documentation, approvals, and control test results in a single, secure system. Link each piece of evidence directly to the relevant metric, control, and reporting period to support defensibility during internal or regulatory audits.

- Integrate Risk, Control, and Remediation Workflow: Map ESG risks to associated controls and remediation tasks. Track issues from identification through resolution, ensuring that corrective actions are documented, assigned, and closed in a timely manner.

- Understand All Four Ops For End-to-End GRC Execution: Use ComplianceOps to enforce regulatory-aligned controls, RiskOps to monitor ESG risks continuously, PolicyOps to manage and update control documentation, and CaseOps to track incidents, exceptions, or reporting discrepancies, all within a unified GRCOps framework.

- Provide Leadership Dashboards and Reporting Insights: Deliver real-time dashboards that show control performance, evidence completeness, risk exposure, and remediation status. Leadership gains actionable insights that improve reliability, reduce manual follow-ups, and maintain audit readiness.

Also Read: ESG Compliance and Sustainability

VComply ensures that ESG control execution is consistent, traceable, and operationally integrated, reducing the administrative burden while increasing confidence in every ESG disclosure. Book a demo with VComply to see it in action.

Final Thoughts

Establishing strong ESG controls transforms reporting from a reactive, last-minute activity into a proactive, reliable process. By prioritizing high-impact metrics, tailoring controls to data patterns, and implementing continuous monitoring, organizations can ensure accuracy, transparency, and audit readiness for every disclosure cycle.

Platforms like VComply make operationalizing ESG controls seamless, centralizing ownership, evidence, and oversight while linking risks, controls, and remediation workflows. With structured execution across ComplianceOps, RiskOps, PolicyOps, and CaseOps, teams can enforce accountability and maintain consistent, board-ready reporting.

Sign up for a 21-day free trial and experience how VComply strengthens ESG controls while reducing manual work across your organization.

FAQs

An ESG control framework defines structured processes, responsibilities, and evidence standards for ESG reporting. It ensures consistency, accountability, and traceability, allowing organizations to manage ESG risks, produce accurate disclosures, and demonstrate readiness for audits or regulatory reviews while aligning with internal governance and compliance practices.

Organizations prioritize metrics based on materiality, regulatory requirements, and stakeholder expectations. High-impact metrics, operational significance, and investor relevance guide selection. Materiality assessments help allocate control resources efficiently, ensuring controls focus on metrics that could influence decisions or create regulatory or reputational exposure.

Companies often reference SASB, TCFD, GRI, or ISSB frameworks to guide ESG reporting. Selecting a standard helps define required metrics, disclosures, and evidence expectations. Organizations can map controls and processes to these frameworks, ensuring alignment, audit readiness, and consistency across reporting cycles.

A materiality assessment identifies ESG topics that could impact stakeholders or regulatory compliance. It combines quantitative data, risk analysis, and stakeholder input to prioritize metrics. Control efforts are focused on material topics, ensuring resources target high-risk areas while supporting defensible, decision-grade ESG reporting.

Third-party data should undergo verification through attestations, sampling, and reconciliation checks. Contracts should define reporting requirements, while exception workflows ensure the timely resolution of inconsistencies. Embedding these practices into ESG controls maintains data integrity and provides audit-ready evidence for all externally sourced metrics.