NAIC Compliance Framework for Insurers: Practical Guide for 2026

Insurers today face regulatory demands that are as complex as the products they underwrite. You know better than most how state-based regulation in the United States creates administrative strain, with each jurisdiction interpreting and adopting NAIC model laws differently.

That fragmentation drives operational work and oversight costs and complicates your preparation for regulatory exams.

In fact, 70% of insurers plan to spend more time on regulatory compliance this year than last, and nearly half were fined or issued refunds due to compliance errors. For compliance officers, risk owners, CIOs, and executives at US insurers, this is a persistent operational challenge. You need clarity on what “NAIC compliance” actually means in practice and a method to manage it as a system.

In this blog, we will explain the NAIC compliance framework for insurers, what it means for your operations, and how to build an audit-ready program that works.

Key Takeaways

- NAIC compliance for insurers is a continuous, state-driven program requiring clear ownership, consistent execution, and defensible evidence.

- Successful compliance depends on structuring requirements across financial governance, risk, cybersecurity, and market conduct domains.

- Regulators prioritize operational proof during exams, including control testing, remediation, and accessible documentation.

- A baseline-and-state-overlay approach helps manage regulatory variation without added complexity.

- Repeatable workflows and centralized evidence improve exam readiness and reduce regulatory risk.

Did you know? In 2025, insurers globally were managing over 4,500 separate regulatory compliance obligations each year, including solvency, anti‑money‑laundering, and policyholder protection requirements. A volume so high that experts say it makes automation and centralized tracking essential for staying audit‑ready.

What “NAIC Compliance” Means In The Real World

NAIC compliance becomes tangible only when regulatory expectations translate into day-to-day decisions, accountability, and proof. For insurance compliance software leaders, this is less about reading model laws and more about running a defensible, state-aligned compliance program that holds up during examinations.

Below Is What NAIC Compliance Looks Like In Practice:

- Standardized Guidance, Not Direct Enforcement: NAIC sets common regulatory compliance direction through model laws, frameworks, and accreditation standards. You use these as the baseline, but they do not function as directly enforceable rules.

- State-Level Interpretation and Enforcement: Each state department adopts, modifies, and enforces NAIC guidance differently. You must align compliance activities with how each regulator applies those expectations.

- Multi-Jurisdiction Obligation Management: NAIC compliance requires coordinating overlapping requirements across all states where you operate, without assuming uniform language, timelines, or documentation standards.

- Operational Proof Over Policy Intent: Regulators expect evidence of execution, assigned ownership, completed controls, testing records, and remediation, not just written policies or theoretical alignment.

- Continuous Readiness, Not Event-Based Compliance: Effective NAIC compliance functions as an ongoing operating model that supports exams, market conduct reviews, and leadership oversight at any time.

Also Read: Your Guide to Major Life Science Compliance Risks

While the NAIC compliance framework for insurers provides a clear structure on paper, many organizations struggle when it comes to translating those expectations into consistent, actual execution.

Why Insurers Struggle With NAIC-Aligned Requirements

NAIC-aligned compliance challenges rarely come from a lack of intent. They arise when operational complexity collides with regulatory expectations. As a compliance leader, you must demonstrate consistency, control, and accountability across the organization while meeting board expectations for transparency and examination readiness.

Below Are The Most Common Operational Risks Insurers Face:

- Multi-State Variation and Version Control: You must track different state adoptions, amendments, and effective dates while ensuring teams reference the correct regulatory version at all times.

- Fragmented Compliance Ownership: Responsibilities often span legal, compliance, IT, finance, and operations, creating gaps in accountability and inconsistent execution across functions.

- Unstructured Evidence Management: Evidence scattered across shared drives, inboxes, and audit binders slows response times and weakens confidence during regulatory examinations.

- Manual Regulatory Change Tracking: Relying on spreadsheets and institutional memory increases the risk of missed updates, delayed responses, and inconsistent compliance actions.

These challenges make it clear why insurers need to break the NAIC compliance framework into practical domains that can be operationalized, measured, and maintained over time.

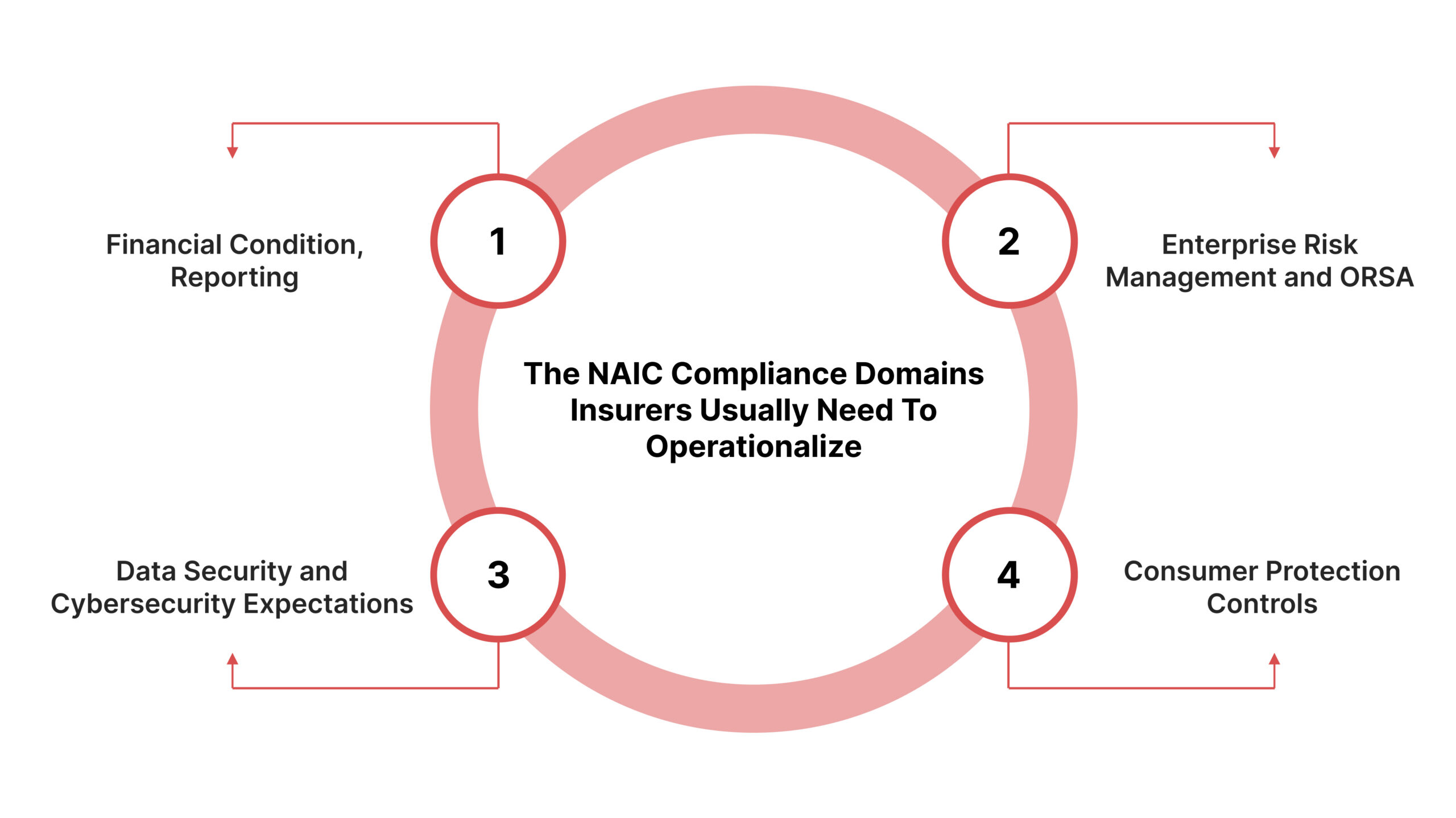

The NAIC Compliance Domains Insurers Usually Need To Operationalize

NAIC-driven compliance becomes manageable only when you organize obligations into clear, operational domains. Instead of treating requirements as isolated rules, insurers must group them into structured areas that align governance, risk, and daily execution across the enterprise.

Below Are The Primary Compliance Domains Insurers Commonly Operationalize:

Financial Condition, Reporting, and Audit Governance

This domain directly shapes regulatory confidence. State regulators expect clear oversight of financial reporting, strong internal controls, and documented audit governance. The NAIC Model Audit Rule often becomes the reference point regulators use to evaluate whether your financial governance operates with discipline and transparency.

Below Is What This Domain Requires Operationally:

- Model Audit Rule Alignment As A Governance Baseline: You must align financial governance practices with the expectations outlined in the NAIC Model Audit Rule, including management responsibility and oversight structure.

- Defined Internal Control Ownership and Testing: Financial controls must have named owners, documented procedures, and periodic testing results that demonstrate effectiveness over time.

- Structured Audit Committee Workflows: Audit committees are expected to review reports, approve remediation actions, and document oversight decisions through meeting records and formal approvals.

- Consistent Financial Reporting Evidence: You must maintain traceable evidence supporting financial statements, management assertions, and control effectiveness to respond confidently during examinations.

- Clear Issue Escalation and Remediation Tracking: Identified control weaknesses require documented remediation plans, timelines, and closure evidence to demonstrate accountability and follow-through.

Enterprise Risk Management and ORSA

Enterprise Risk Management and ORSA shape how regulators evaluate your ability to understand, monitor, and govern risk at an organizational level. ORSA is not a one-time report but a structured process that connects risk ownership, solvency assessment, and board-level oversight.

Below Is What Effective ORSA Operationalization Looks Like:

- Defined Risk Identification and Assessment Cycles: You must establish recurring processes to identify material risks, assess their impact on solvency, and document assumptions supporting those assessments.

- Clear Risk Ownership Across The Enterprise: Each significant risk requires an accountable owner responsible for monitoring exposure, updating assessments, and escalating concerns when thresholds are exceeded.

- Board-Level Review and Challenge Mechanisms: ORSA outputs must reach the board through structured reports that support informed review, discussion, and documented challenge.

- Integrated Solvency Impact Analysis: Risk assessments should clearly demonstrate how changing risk conditions affect capital adequacy and long-term financial stability.

- Consistent Reporting Cadence and Evidence Retention: You must maintain records showing when ORSA activities occur, who reviews them, and how leadership decisions align with documented risk insights.

With VComply’s Risk Ops, insurers can assign accountable risk owners, schedule recurring assessments, and maintain clear traceability. This makes enterprise risk management and ORSA outputs consistent, actionable, and board-ready.

Data Security and Cybersecurity Expectations

Data protection regulation has become a core regulatory concern as cyber incidents directly impact policyholders and market stability. NAIC’s Insurance Data Security Model Law sets expectations for how insurers govern security, detect incidents, and communicate with regulators when events occur.

Below Are The Core Operational Expectations Insurers Must Address:

- Documented Information Security Program Governance: You must maintain a formally approved security program that defines objectives, scope, accountability, and oversight aligned with your data sensitivity and risk profile.

- Risk-Based Safeguards and Control Implementation: Security controls should reflect assessed risks, covering administrative, technical, and physical safeguards without relying on generic or static control sets.

- Incident Detection and Investigation Processes: You are expected to identify security events promptly, investigate their scope and impact, and document findings using defined response procedures.

- Regulator Notification Readiness: Insurers must demonstrate the ability to assess whether incidents trigger notification obligations and support timely, accurate regulatory reporting when required.

- Ongoing Oversight and Evidence Maintenance: Regulators look for proof that security controls are monitored, tested, and updated, supported by records that show continuous oversight rather than reactive fixes.

Market Conduct and Consumer Protection Controls

Market conduct oversight directly reflects how your organization treats policyholders and distributes products. Regulators evaluate these controls through examinations that focus on consistency, fairness, and documented supervision. Weaknesses in this domain often surface during reviews of operational execution rather than policy design.

Below Are The Core Control Areas Regulators Commonly Examine:

- Claims Handling Consistency and Documentation: You must demonstrate standardized claims processes, timely decisions, and complete records that support fair outcomes and regulatory review.

- Sales and Distribution Oversight: Insurers are expected to monitor sales practices, agent conduct, and product suitability through documented supervision and corrective actions.

- Complaint Intake and Resolution Tracking: Complaint handling requires defined intake processes, root-cause analysis, resolution timelines, and evidence showing issues are addressed systematically.

- Record Retention and Accessibility Controls: You must retain policy, transaction, and communication records in accordance with regulatory expectations and produce them efficiently during examinations.

- Ongoing Management Oversight and Reporting: Leadership must receive regular visibility into market conduct metrics, trends, and corrective actions to demonstrate active supervision.

Also Read: Are You Audit-Ready? A Deep-Dive Guide for Internal Compliance Leaders

Once insurers understand the core NAIC compliance domains they must operationalize, the next challenge is applying the NAIC compliance framework for insurers across states that adopt the same model laws in different ways.

State Adoption: How To Handle “Same Model, Different Rules”

State adoption differences are where NAIC compliance becomes operationally demanding. While model laws create a shared foundation, each state applies its own scope, timelines, and enforcement expectations. Without a structured approach, insurers risk inconsistent execution, missed obligations, and increased examination findings.

Below Is A Practical Method To Manage State-Level Variation Effectively:

- Define Your Regulatory Operating Footprint: Start by documenting your state of domicile and every jurisdiction where you write business, including lines of coverage subject to state oversight.

- Establish A Common NAIC-Based Baseline: Create a core set of requirements derived from NAIC model guidance that applies across the organization, forming the foundation for all compliance activity.

- Layer State-Specific Regulatory Overlays: Identify state-level deviations from the baseline, capturing differences in scope, thresholds, timelines, and documentation expectations.

- Maintain Versioning and Effective Date Control: Track regulatory versions, adoption dates, and amendments to ensure teams operate against the correct requirements at all times.

- Assign Clear Ownership For Each Obligation: Designate accountable owners responsible for execution, monitoring, and updates to ensure no requirement is left unmanaged.

A Simple State Overlay Method

Managing state-level variation becomes far more effective when you apply a repeatable overlay method instead of rebuilding compliance efforts for each jurisdiction. This approach allows you to preserve consistency while addressing state-specific requirements in a controlled, auditable way that supports examination readiness.

Below Is A Practical Overlay Method Insurers Can Apply:

- Baseline Control Definition: Establish standardized controls that reflect core regulatory expectations and apply across all states, forming the foundation of your compliance program.

- State-Specific Requirement Mapping: Identify how each state modifies, expands, or limits baseline controls, documenting these differences clearly to avoid misinterpretation.

- Evidence Impact Assessment: Determine whether state variations require additional documentation, alternate testing, or supplemental records to support regulatory review.

- Reporting and Oversight Adjustments: Align reporting outputs and management reviews with state-specific expectations, ensuring leadership receives accurate visibility into jurisdictional compliance status.

Managing state-level differences within the NAIC compliance framework for insurers ultimately determines how well an organization performs when regulators evaluate its practices during examinations.

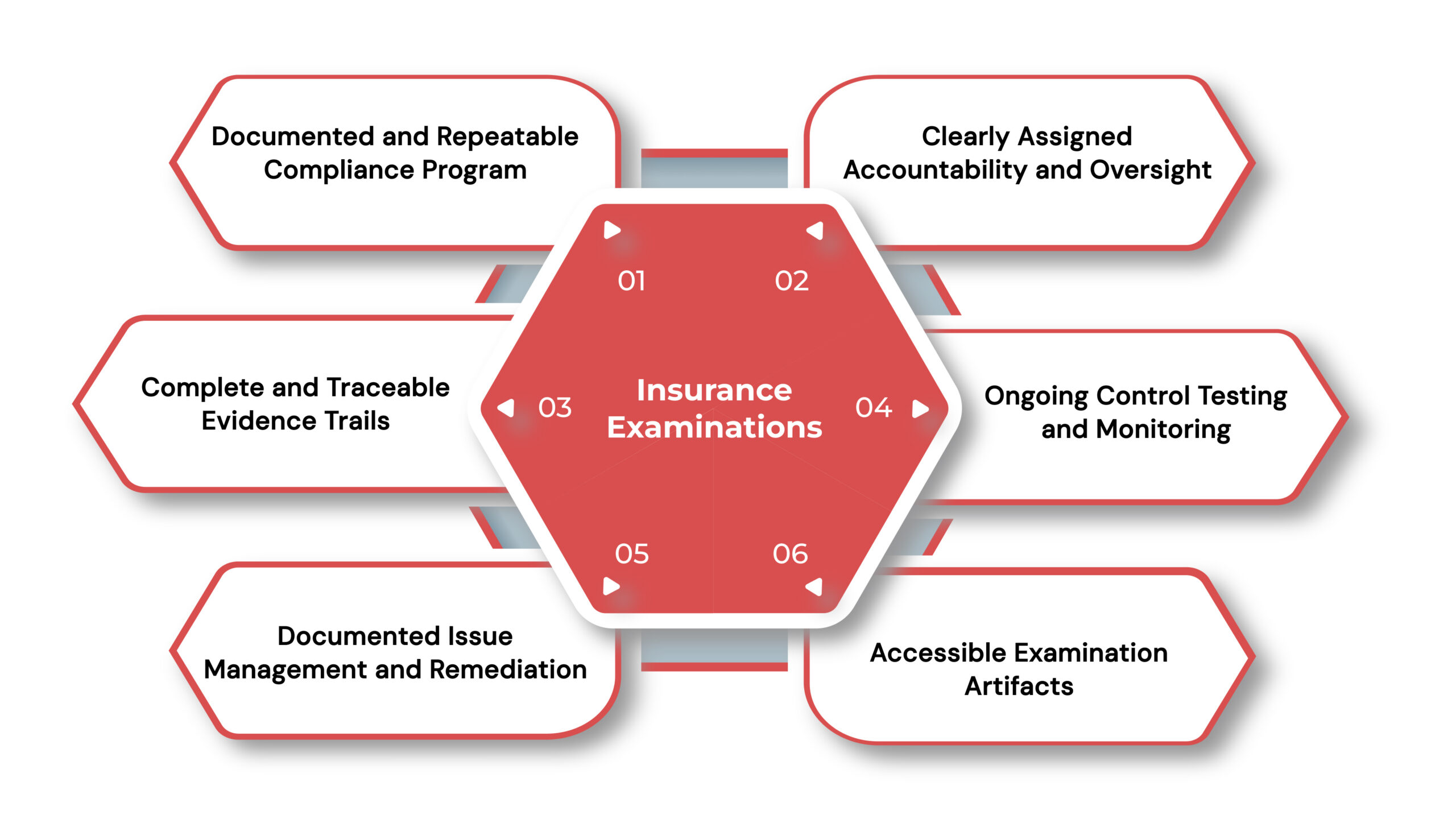

What Regulators Typically Look For During Insurance Exams

Insurance examinations focus on how effectively you translate regulatory expectations into consistent, defensible operations. Regulators are less concerned with intent and more focused on whether your compliance program functions reliably across business units, time periods, and jurisdictions.

Below Is What Regulators Commonly Evaluate During Examinations:

- Documented and Repeatable Compliance Program: You must demonstrate a structured program with a defined scope, documented procedures, and consistent execution rather than ad hoc compliance activity.

- Clearly Assigned Accountability and Oversight: Examiners expect to see named owners for requirements and controls, along with evidence of management and board-level supervision.

- Complete and Traceable Evidence Trails: Evidence should clearly show what was performed, when it occurred, who completed it, and how outcomes were reviewed.

- Ongoing Control Testing and Monitoring: Regulators look for proof that controls are tested periodically and that results inform corrective actions and improvements.

- Documented Issue Management and Remediation: Findings must include root-cause analysis, approved remediation plans, progress tracking, and closure evidence.

- Accessible Examination Artifacts: Typical requests include policies, risk assessments, testing results, incident records, and audit committee materials, all readily available for review.

These examination expectations highlight the need for a practical NAIC compliance framework for insurers that works consistently in real operations.

A Practical NAIC Compliance Operating Model

Sustainable NAIC compliance requires more than isolated controls or annual checklists. You need an operating model that produces consistent inputs, predictable outputs, and defensible results across states and examination cycles. A structured system allows you to scale compliance without increasing operational risk or manual effort.

Below Is A Practical Operating Model Insurers Can Apply:

- Defined Governance and Escalation Structure: Establish clear roles, cross-functional committees, and escalation paths so accountability and decision-making remain consistent across jurisdictions.

- Structured Requirement Mapping Framework: Translate NAIC guidance into specific obligations and map each obligation to documented, owned controls that support execution.

- Standardized Control Execution Cycles: Run controls through scheduled tasks, attestations, and recurring reviews to demonstrate consistency over time.

- Centralized Evidence Management Standards: Apply uniform naming conventions, retention rules, and audit trails to ensure evidence remains accessible and defensible.

- Formal Issue and Remediation Lifecycle: Track findings from identification through remediation and verified closure, preserving proof of corrective action.

- Leadership Reporting and Exam Outputs: Provide dashboards and examination-ready exports that offer clear visibility into compliance status and risk exposure.

VComply’s Compliance Ops centralizes NAIC obligations, assigns clear control ownership, and standardizes recurring workflows. This ensures your compliance program runs consistently and remains audit-ready across all jurisdictions.

With a practical operating model in place, the next step is turning it into action through a structured 90-day implementation plan.

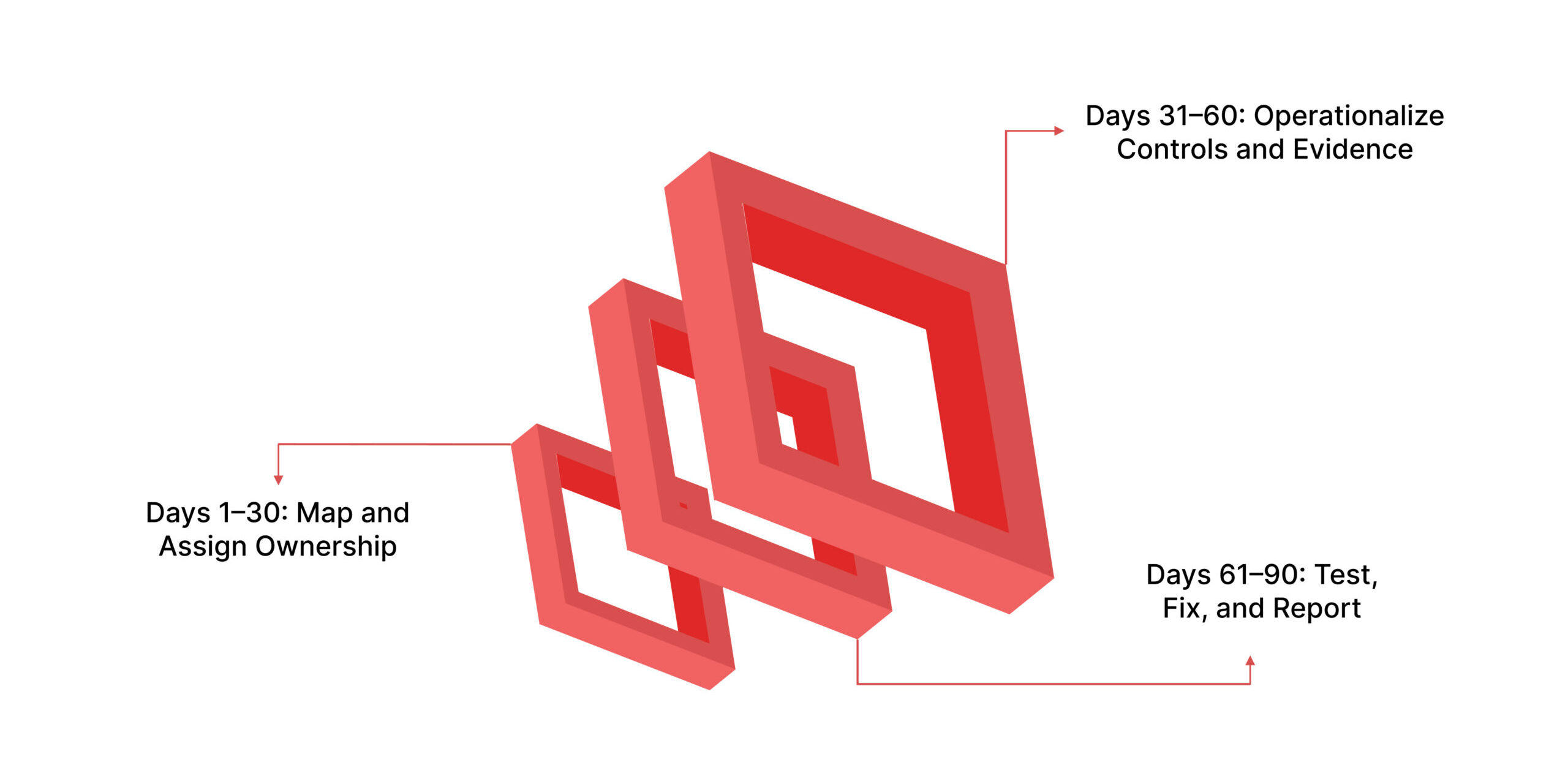

90-Day Implementation Plan For Insurers

Understanding NAIC requirements is only the starting point. Execution determines examination outcomes. A structured 90-day plan helps you move from fragmented compliance activities to a coordinated operating model that regulators can evaluate with confidence.

Below Is A Phased Implementation Approach Insurers Can Follow:

Days 1–30: Map and Assign Ownership

The first 30 days set the foundation for long-term NAIC compliance. Your focus should be on creating clarity around obligations, accountability, and documentation expectations. Without this groundwork, later execution and examination readiness become difficult to sustain.

Below Are The Key Actions To Complete In This Phase:

- Comprehensive Obligation Inventory Development: Compile all applicable requirements driven by NAIC guidance and state-specific adoptions, ensuring full visibility across lines of business and jurisdictions.

- Control Ownership Assignment and Accountability: Assign responsible owners to each control, clearly defining expectations for execution, review, and escalation.

- Standardized Evidence Definition and Criteria: Establish clear standards for what constitutes acceptable evidence, including format, frequency, retention, and review requirements.

- Alignment With Examination Expectations: Validate that mapped obligations and evidence standards align with how regulators assess compliance during examinations.

- Central Documentation Structure Setup: Create a consistent structure for storing obligations, ownership details, and supporting materials to support ongoing governance.

Days 31–60: Operationalize Controls and Evidence

With ownership and standards in place, the next phase focuses on execution discipline. This stage transforms defined requirements into routine activities that generate consistent evidence and reduce reliance on last-minute exam preparation.

Below Are The Core Actions To Execute During This Phase:

- Recurring Compliance Calendar Configuration: Establish scheduled control activities, reviews, and attestations aligned with regulatory timelines and internal oversight expectations.

- Standardized Evidence Capture Processes: Implement uniform methods for collecting, labeling, and validating evidence to ensure consistency and reliability across teams.

- Initial Control Performance Reviews: Begin evaluating whether controls operate as designed, documenting outcomes, and identifying early gaps.

- Cross-Functional Coordination Alignment: Synchronize activities across compliance, IT, finance, and operations to reduce duplication and execution delays.

- Early Documentation Quality Checks: Review evidence for completeness and clarity to confirm it meets examination standards before formal testing cycles.

Days 61–90: Test, Fix, and Report

The final phase validates whether your NAIC compliance program can withstand regulatory scrutiny. This period focuses on testing execution quality, resolving weaknesses, and establishing leadership visibility that supports confident examination engagement.

Below Are The Key Activities To Complete In This Phase:

- Mock Examination Readiness Review: Conduct a structured internal review that simulates regulatory examination requests, timelines, and evidence expectations.

- Tracked Issue Remediation and Validation: Addressed identified gaps through documented remediation plans, progress tracking, and verification of corrective actions.

- Formal Management Review and Sign-Off: Ensure leadership reviews findings, approves remediation outcomes, and documents oversight decisions.

- Established Reporting Cadence For Leadership: Create a regular rhythm for reporting compliance status, risk management, and remediation progress to senior management and the board.

- Exam-Ready Documentation Finalization: Confirm that evidence, reports, and supporting materials are complete, current, and accessible for regulatory review.

Also Read: Understanding the Purpose of a Policy Summary

Even with a solid 90-day plan, gaps in execution can derail the NAIC compliance framework for insurers, making it important to understand the most common mistakes before they happen.

Mistakes That Create NAIC Exam Pain (and How To Avoid Them)

NAIC examinations rarely fail because of missing intent. They fail when execution lacks consistency, visibility, or proof. Understanding common breakdowns helps you correct weaknesses before regulators identify them, reducing disruption and examination risk.

Below Are The Most Common Mistakes That Create Examination Challenges:

- Treating NAIC Guidance As Static Requirements: Assuming obligations remain unchanged leads to outdated controls and missed regulatory updates that surface during examinations.

- Operating Without A Central Source Of Truth: Dispersed policies and controls prevent consistent execution and make it difficult to demonstrate alignment across business units.

- Capturing Evidence After The Fact: Reconstructing evidence during exams weakens credibility and increases the likelihood of follow-up requests.

- Insufficient Third-Party Oversight Documentation: Limited visibility into vendor controls and assessments creates gaps that regulators often flag during reviews.

- Closing Findings Without Verified Proof: Marking issues as resolved without documented validation undermines confidence in remediation effectiveness.

VComply’s Case Ops lets you track findings from discovery to verified closure, maintain full audit trails, and coordinate cross-functional remediation. This reduces repeat examination issues and strengthens regulatory confidence.

Avoiding common NAIC exam pitfalls is only half the equation; the next step is measuring whether your NAIC compliance framework for insurers is actually working.

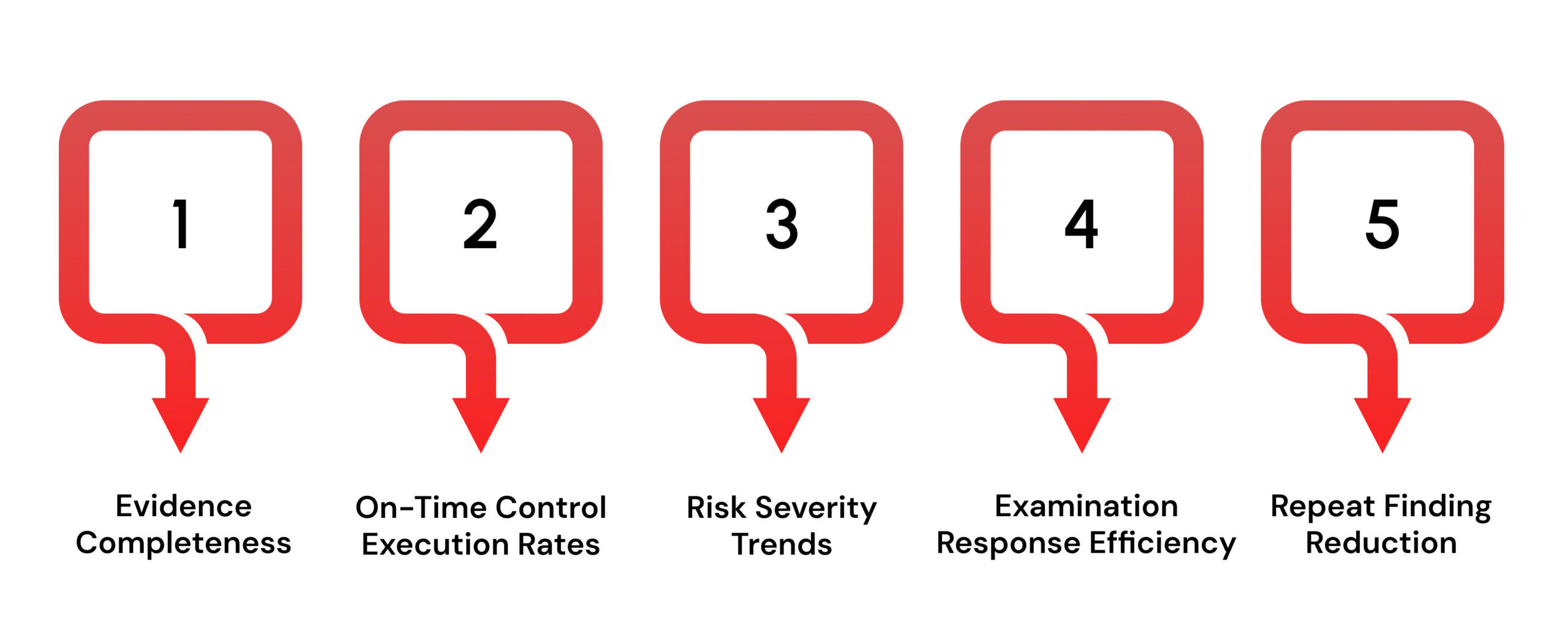

Metrics That Show Your NAIC Compliance Program Is Working

A well-run NAIC compliance program produces measurable outcomes, not assumptions. Metrics help you validate whether controls operate as intended, risks remain managed, and examination readiness improves over time. For leadership, these indicators provide objective assurance that compliance efforts deliver value.

Below Are Key Metrics Insurers Should Monitor:

- Audit Readiness and Evidence Completeness: Track whether required evidence is complete, current, and available on schedule for regulatory review.

- On-Time Control Execution Rates: Measure the percentage of controls completed within defined timelines to assess execution discipline.

- Issue Aging and Risk Severity Trends: Monitor how long issues remain open and whether high-risk control failures decrease over time.

- Examination Response Efficiency: Evaluate how quickly teams can assemble and deliver examination materials without disruption.

- Repeat Finding Reduction: Assess whether prior examination findings recur, signaling weaknesses in remediation effectiveness.

Tracking the right metrics shows how well your NAIC compliance framework for insurers is performing. Let’s look at how VComply helps put that framework into action.

How VComply Supports NAIC Compliance Programs For Insurers

Running NAIC compliance at scale requires a system that converts regulatory expectations into consistent execution. VComply acts as the execution layer that helps you operationalize NAIC-driven requirements across states while maintaining visibility, accountability, and examination readiness.

Below Is How VComply Enables Effective NAIC Compliance:

- Centralized NAIC Requirement and State Overlay Management: VComply provides a single system to organize NAIC-driven obligations and layer state-specific variations, allowing you to manage requirements without fragmentation or version confusion.

- Automated Ownership and Recurring Compliance Workflows: You can assign clear ownership, schedule recurring tasks, trigger reminders, and capture attestations, ensuring obligations are executed consistently and on time.

- Structured Evidence Collection With Full Audit Trails: VComply enables you to collect evidence as work occurs, maintain traceable audit trails, and preserve documentation that regulators expect during examinations.

- Integrated Issue and Remediation Management: Identified gaps can be tracked from discovery through remediation and verified closure, providing clear proof of corrective action and reducing repeat findings.

- Role-Based Reporting and Executive Visibility: Compliance leaders and executives gain tailored dashboards and reports that highlight compliance status, risk exposure, and readiness across jurisdictions.

- Unified GRC Operations Through VComply Ops Suites: VComply brings together ComplianceOps, RiskOps, PolicyOps, and CaseOps to support end-to-end NAIC compliance, covering regulatory execution, enterprise risk alignment, policy governance, and incident management within one connected GRC operating model.

Read Next: How to Build a Risk Register That Actually Guides Decisions

With the right systems in place, managing a strong NAIC compliance framework becomes more straightforward. See how VComply brings everything together in one place and supports consistent execution. Start a free trial to explore how it works in practice.

Final Thoughts

NAIC compliance is no longer a periodic obligation you address during examination cycles. It has become a continuous, operational discipline that demands consistency across states, clear ownership, and defensible evidence. When you treat the NAIC compliance framework for insurers as an integrated operating model, you reduce regulatory risk, improve exam outcomes, and strengthen organizational confidence.

This is where VComply delivers measurable value. By acting as the execution layer for NAIC-aligned compliance, VComply helps you translate regulatory expectations into day-to-day workflows, connect compliance with risk and policy governance, and maintain exam readiness without operational strain.

Book a demo with VComply to see how you can operationalize NAIC compliance with confidence and control.

FAQs

NAIC itself does not directly regulate insurers. However, states adopt NAIC model laws and enforce them through their insurance departments. If you operate in a state that has adopted a model law, compliance becomes mandatory under that state’s regulatory authority.

State insurance departments typically conduct financial or market conduct examinations every three to five years. The frequency may increase based on risk profile, prior findings, complaints, or significant operational or financial changes within the insurer.

Failure to meet NAIC-aligned expectations can lead to regulatory findings, corrective action plans, fines, increased oversight, or follow-up examinations. Persistent deficiencies may escalate to license restrictions or reputational damage with regulators and stakeholders.

NAIC accreditation ensures state insurance departments meet uniform regulatory standards. For insurers, this results in more consistent examination practices across states, but also higher expectations for governance, documentation, and financial and operational controls.

NAIC model laws are not legally binding unless adopted by a state. However, regulators may still reference them as best-practice benchmarks when evaluating governance, risk management, and operational maturity during examinations or supervisory discussions.