Internal Risk in 2026: Where It Starts and Why It Escalates

Internal risk often becomes clear only after the damage is visible. The warning signs usually appear earlier: repeated exceptions, weak approvals, incomplete records, unresolved control gaps, or issues that remain locally known but never formally escalated.

In March 2026, the U.S. Department of Justice released its first department-wide corporate enforcement policy for criminal matters, reinforcing a standard many compliance leaders already understand: scrutiny does not end at whether a policy exists.

Internal risk sits directly inside that problem. It develops when small breakdowns become tolerated, disconnected, or invisible to leadership. This guide explains what internal risk includes, where it appears first, why it becomes harder to contain, and what stronger oversight requires.

Before moving into how internal risk escalates, the fundamentals need to be clear.

TL;DR

- Internal risk originates inside the organization, usually through people, processes, systems, or weak control execution.

- It rarely becomes serious all at once. It builds when exceptions, ownership gaps, and unresolved weaknesses are allowed to sit inside routine operations.

- The real issue is not awareness alone. It is whether risk is identified early, assigned clearly, escalated properly, and reviewed with discipline.

- Strong internal risk oversight depends on reliable controls, defined accountability, usable reporting, and leadership visibility.

- Once those elements weaken, internal risk stops being an isolated operational issue and starts becoming a governance concern.

What Is Internal Risk?

Internal risk refers to exposure originating within the organization, through its people, processes, systems, governance practices, or internal controls. In practical terms, that includes more than misconduct. It can involve process failure, poor access discipline, inconsistent review practices, reporting gaps, control breakdowns, and management decisions that weaken oversight over time.

What makes internal risk difficult is not simply that it exists within the business. Familiar weaknesses are often absorbed into routine operations and treated as manageable until they begin to affect reporting, compliance, audit readiness, or decision-making.

Once ownership is unclear, escalation is uneven, or monitoring becomes fragmented, internal risk stops being a local problem and starts becoming a governance problem.

The next distinction matters because internal and external risks may both create disruption, but they do not respond to the same management model.

Internal Risk vs External Risk: What Changes in the Response

The distinction matters less as a definition exercise and more as a management decision. Internal risk usually demands stronger ownership, tighter controls, and better internal escalation, while external risk is more often managed through scenario planning, resilience, and response readiness.

| Dimension | Internal Risk | External Risk | Why It Matters in Practice |

|---|---|---|---|

| Source | Originates within people, processes, systems, governance practices, or internal controls | Comes from market, regulatory, geopolitical, environmental, or third-party forces | It tells you where direct intervention is possible and where it is not. |

| Controllability | Usually more influenceable through internal action | Often less controllable directly | It shapes whether your response should focus on prevention or on resilience. |

| Early signals | Often appears through workflow gaps, repeated exceptions, conduct issues, weak approvals, or stale reviews | Often appears through external developments, regulatory shifts, vendor disruption, or broader market events | It changes where monitoring attention needs to sit. |

| Ownership | Usually requires internal accountability, escalation, and follow-through | Often requires response planning, coordination, and readiness across functions | It clarifies who should act first and how quickly. |

| Management approach | Stronger controls, clearer oversight, regular review, and escalation discipline | External scanning, contingency planning, and coordinated response capability | It helps prevent the wrong response model from being applied to the wrong type of risk. |

The distinction becomes more useful once you look at where management attention should go first.

Internal risk usually calls for tighter ownership, stronger controls, and more disciplined escalation inside the organization.

External risk usually demands readiness, coordination, and response planning around forces you cannot directly control.

Also Read: Risk and Compliance: Understanding the Key Differences in 2026

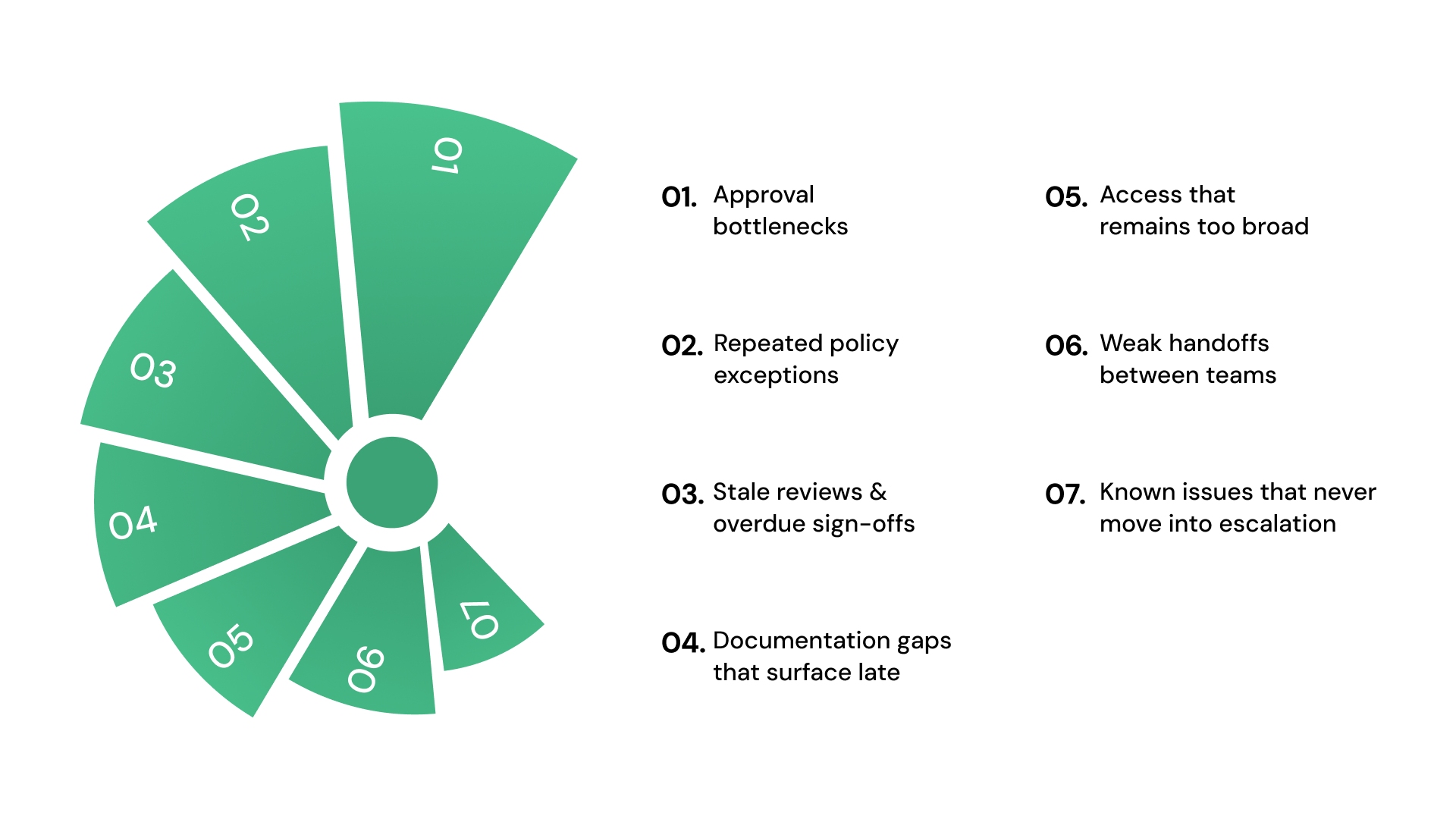

Where Internal Risk Starts Showing Up in Day-to-Day Operations

Internal risk usually shows up before anyone formally labels it as risk. In most organizations, it first appears as repeated friction within routine work rather than as a single visible failure.

Common early patterns include:

- Approval bottlenecks

Requests stay with the same reviewers for too long, steps are bypassed to keep work moving, and exceptions start to function like a second process. - Repeated policy exceptions

Teams know the stated rule, but deviations keep getting tolerated because stopping the work feels harder than carrying the risk. - Stale reviews and overdue sign-offs

Attestations, reviews, and checks remain open longer than they should, often completed only after reminders or just before scrutiny increases. - Documentation gaps that surface late

Records appear complete until someone has to trace what happened, who approved it, and whether the supporting evidence matches the action taken. - Access that remains too broad

Permissions continue long after the original need has changed, and no one rechecks whether access still fits the role. - Weak handoffs between teams

Work moves across functions, but accountability weakens at the point of transfer. Each team assumes someone else has taken ownership. - Known issues that never move into escalation

A recurring weakness is discussed informally, addressed locally, and treated as manageable without entering into a structured review.

What matters is not the presence of one delay or one exception. It is the recurrence of the same breakdown across approvals, records, reviews, or handoffs without a credible reduction in exposure.

Also read: Internal Control Weakness: How to Identify and Fix It in 2026

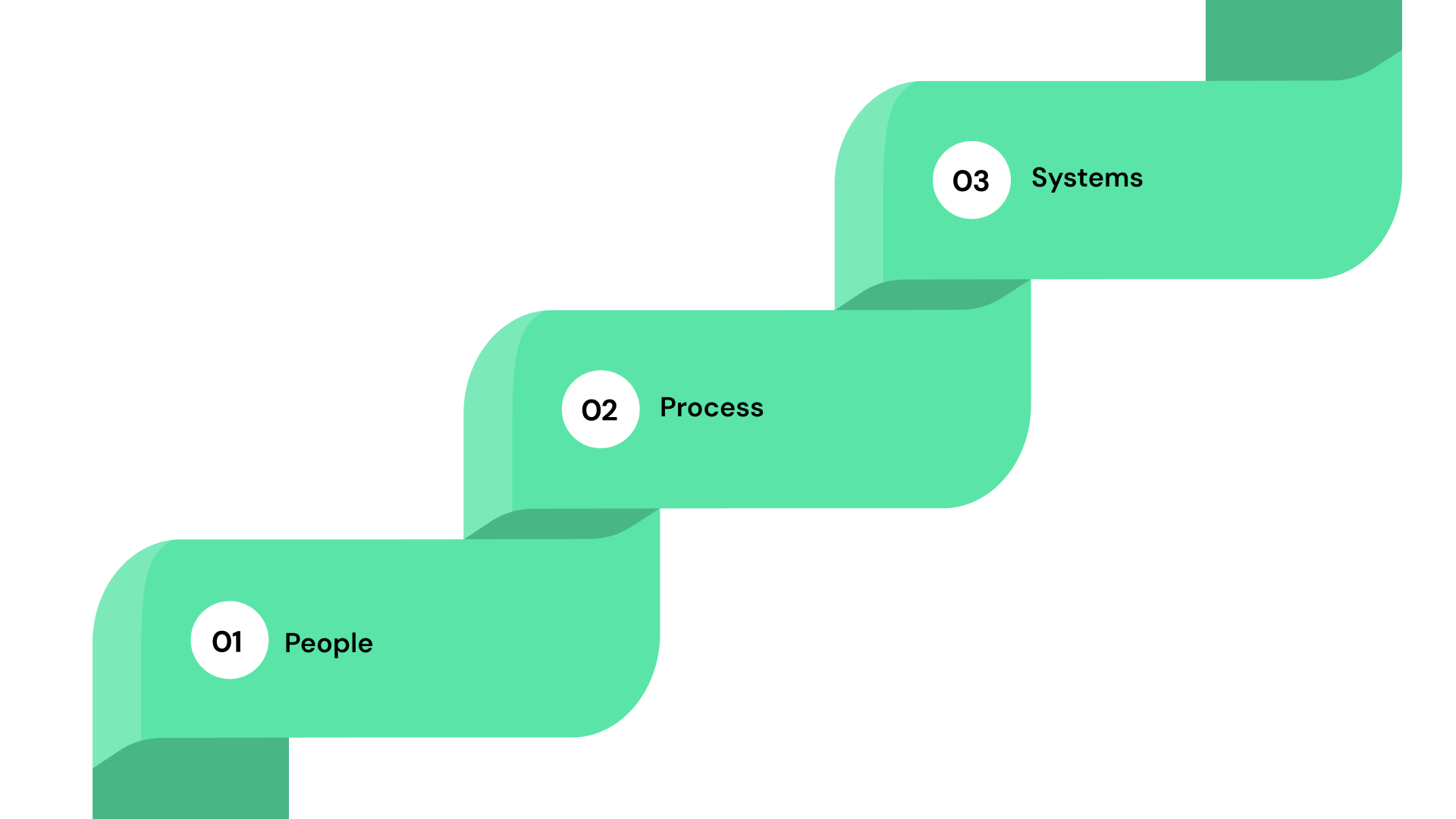

What Usually Sits Behind Internal Risk

Internal risk rarely comes from a single source. In most organizations, it begins with weaknesses in people, processes, or systems, and then becomes harder to manage when those weaknesses persist. Identifying the driver matters because it shows whether the weakness is contained, repeating, or becoming structural.

People

People-related risk is not limited to misconduct. It often begins with ordinary failures of judgment: human error, weak escalation decisions, poor training, or shortcuts that gradually become accepted as the norm. In higher-risk cases, it can also involve concealment, misuse of access, or insider behavior.

Process

Process-related risk arises when the formal workflow no longer aligns with how work is actually getting done. Weak approvals, incomplete procedures, inconsistent control execution, poor segregation of duties, and review failures all create room for exposure to build quietly.

Systems

Systems become a source of internal risk when the technology no longer supports clean control execution. Common signs include broad access, workflow gaps, fragmented records, unreliable monitoring, and data handling that makes it difficult to trace actions in context.

These drivers do not usually stay separate for long. A people issue may continue because the process does not force escalation. A systems issue may persist due to weak ownership. A process weakness may deepen because no one is reviewing whether it still works in practice.

Also read: How to Build a Risk Management Model That Produces Real Visibility

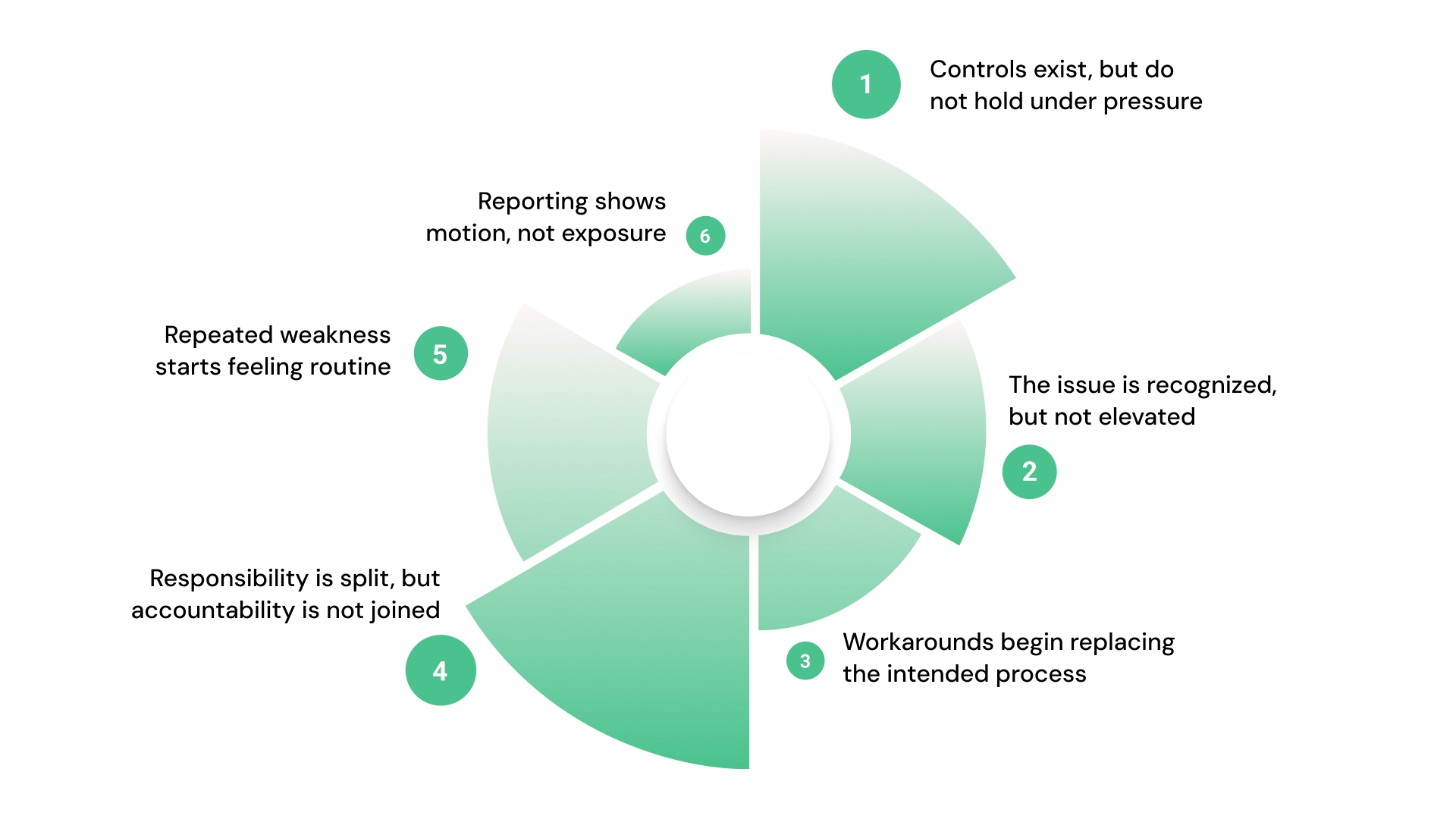

Why Internal Risk Gets Harder to Contain

Internal risk does not become harder to contain only because it is missed early. It becomes harder to contain when the organization recognizes the weakness but does not provide enough structure to address it.

Common reasons include:

- Controls exist, but do not hold under pressure: A control may be documented and formally assigned, yet still break down when deadlines tighten, exceptions increase, or teams begin treating required steps as optional.

- The issue is recognized but not elevated: A weakness may be understood within one team and still never move into broader review, keeping the response narrow even when the exposure is not.

- Workarounds begin replacing the intended process: Once the formal path is seen as too slow or too disconnected from reality, teams start solving around it rather than through it.

- Responsibility is split, and no one connects the full picture: Different functions may each see one part of the problem, the operational issue, the control gap, the reporting consequence, without anyone joining them into a single risk view.

- Reporting shows motion, not exposure: Leadership receives updates and open-item summaries without seeing how many exceptions, delays, or breakdowns are clustering around the same underlying weakness.

At that point, the problem is no longer only identification. The weakness is visible. What is missing is enough ownership, escalation, and structure around the response to reduce it.

What Strong Internal Risk Oversight Looks Like

Strong internal risk oversight depends on a structure that makes risk easier to own, review, escalate, and act on over time. The issue is not how much risk is discussed — it is whether known weaknesses move toward action before they become harder to govern.

- Clear ownership and review responsibility: Internal risk weakens quickly when everyone is involved, but no one is explicitly accountable. Strong oversight begins with knowing who owns the issue, who reviews it, and who is expected to act when conditions change.

- Defined escalation paths: A recurring weakness should not depend on personal judgment alone to move upward. Escalation works better when thresholds, review routes, and decision points are already clear before the issue surfaces.

- Controls that are monitored, not assumed: A documented control is not the same thing as a functioning control. Strong oversight tests whether controls are being followed, whether exceptions are increasing, and whether the control still holds under pressure.

- Regular review cadence: Risks are easier to manage when the review is routine rather than reactive. A defined cadence makes it easier to separate isolated disruption from patterns that are becoming structural.

- Reporting that leadership can act on: Leadership does not need more status volume. It needs reporting that shows where exposure is building, where ownership is weak, and where unresolved issues are clustering.

- Alignment across compliance, risk, and internal audit: Internal risk becomes harder to manage when each function sees only one part of the issue. Stronger oversight connects the control weakness, the operating consequence, and the governance implication into a single picture.

Helpful resource: Internal risk becomes harder to manage when ownership and follow-through are not captured consistently. VComply’s Risk Register Template gives you a practical way to document risks, assign accountability, and maintain visibility across review cycles.

When Internal Risk Becomes a Governance Problem

Internal risk becomes a governance problem when it stops being something a single team can correct on its own and starts affecting how leadership assesses exposure across the organization.

At that stage, the issue is no longer just whether a control failed or a process drifted. The larger question is whether the organization can still see risk clearly enough, prioritize it correctly, and show that oversight is working at a higher level.

Common signs include:

- The same weakness appears across multiple teams or units

What looked local is now showing up across different functions, workflows, or locations. - Leadership cannot see aggregate exposure clearly

Updates continue, but they do not show where risk is concentrating, how patterns are changing, or which issues remain unresolved long enough to matter. - Management and review functions are not working from the same picture

Compliance, risk, and internal audit may each identify part of the issue without producing a single clear view of the problem and its implications. - Corrective action loses credibility over time

Findings are recorded and responses noted, but confidence in the actual reduction of the weakness begins to decline. - Governance reporting shows activity without decision value

Leadership receives information, but not the kind that supports prioritization, challenge, or timely intervention. - Recurring breakdowns begin affecting assurance confidence

Once the same issues keep surfacing, the question shifts from whether the organization has controls to whether it can rely on them.

At that point, internal risk is no longer a test of one team’s ability to respond. It is testing the strength of the organization’s governance model.

How VComply Brings More Discipline to Internal Risk Oversight

The six oversight requirements above, clear ownership, defined escalation, monitored controls, review cadence, actionable reporting, and cross-function alignment, are process requirements. They are only as strong as the system that supports them.

When risk records, ownership assignments, review activity, escalation history, and control status are managed across disconnected tools, even a well-designed oversight structure becomes difficult to execute consistently and nearly impossible to audit when scrutiny arrives.

RiskOps addresses that gap directly. It gives risk teams a centralized environment where individual risk records carry explicit ownership, escalation paths are defined in advance, and the current status of each material exposure is visible across functions in real time.

When a weakness triggers a reassessment, the update occurs within the same system that holds the risk record, keeping the oversight process current rather than dependent on manual follow-up and fragmented tracking.

The result is an internal risk program where ownership, review, and escalation are traceable, not because someone assembled the record after the fact, but because the workflow produced it as a standard output.

Schedule a demo to see how RiskOps brings more structure and continuity to internal risk oversight.

Conclusion

Internal risk becomes difficult to manage when the organization cannot move cleanly from recognition to response. The issue is not whether weaknesses exist; it is whether ownership is clear enough, review is steady enough, and oversight is strong enough to keep those weaknesses from compounding before they become a governance problem.

If that is the gap your organization is working to close, start a 21-day free trial and see how RiskOps works in practice.

FAQs

It develops inside familiar workflows, decisions, and relationships, which means it is often absorbed into routine operations before anyone formally labels it as risk. By the time it becomes visible, it may already be embedded in how work is being handled.

Usually, because ownership is unclear, escalation stays too local, or the issue is managed through workarounds instead of formal follow-through. The weakness is known but not reduced, and the longer that continues, the harder it becomes to treat it as something requiring intervention rather than routine friction.

Reviews happen, updates are shared, and issues are discussed, but leadership still cannot see where exposure is building, what remains open, or which weaknesses are repeating across functions. Activity is visible; risk concentration is not.

Because the first signs usually appear inside one team, one process, or one control gap. The broader picture only becomes clear when the same weakness begins to show up across functions or to affect reporting, compliance, or assurance confidence.

A manageable issue can still be owned, reviewed, and corrected within the operating process. A governance problem arises when the organization can no longer rely on local fixes, as visibility, coordination, and decision-making must operate above the team level.

Oversight becomes more reliable when risk identification, ownership, review, escalation, and reporting operate as one connected process rather than separate activities. That is where structure matters more than intent and where a platform like RiskOps makes the difference, centralizing ownership, review cadence, and escalation into a single environment rather than leaving each element to be managed separately.