Step-by-Step Guide to AML/CTF Compliance Programs

An AML/CTF program is a comprehensive framework of controls, procedures, and strategies designed to prevent money laundering and terrorist financing. It helps businesses identify, assess, mitigate, and report suspicious financial activities. These obligations are applicable across various sectors, including fintech startups, legal advisory firms, real estate agencies, and cryptocurrency exchanges.

What does it take to stay ahead of money laundering risks without slowing down your business?

In the United States alone, the Financial Crimes Enforcement Network (FinCEN) reported identity-related suspicious activity remains a significant concern, with approximately 1.6 million reports, representing 42% of all filings, linked to identity issues and totaling $212 billion in suspicious activity. Businesses handling customer funds, assets, or high-value transactions are now expected to maintain AML/CTF programs that not only detect suspicious behavior but also prove accountability across internal teams.

Most companies aren’t failing due to a lack of intent; they’re failing because their compliance programs are fragmented, inconsistent, or built on outdated templates. Delayed reporting, unclear roles, poor documentation, or missed training deadlines can result in penalties, audit failures, or reputational damage.

Key Takeaways (TL;DR)

-

Learn how to build an effective AML/CTF program that prevents financial crime without slowing growth.

-

Understand why a risk-based approach, from due diligence to monitoring, strengthens compliance resilience.

-

Discover how real-time transaction tracking and reporting help detect suspicious activity early.

-

See how ongoing staff training and independent audits ensure consistent AML/CTF program effectiveness.

-

Explore how VComply automates AML/CTF compliance, streamlines reporting, and keeps your business audit-ready.

What is an AML/CTF Program?

An AML/CTF program is a formal set of controls, procedures, and strategies that a business implements to prevent money laundering and terrorist financing. It ensures your organization can identify, assess, mitigate, and report suspicious financial activity.

AML and CTF obligations apply across sectors, including fintech startups, legal advisory firms, real estate agencies, and cryptocurrency exchanges. If your business handles customer funds or facilitates high-value transactions, you’re likely required to comply with these regulations.

A well-built AML/CTF program includes:

- A written framework tailored to your business

- Appointment of compliance officers

- Staff training protocols

- Ongoing transaction monitoring

- Regular independent reviews

The structure and complexity of the program should align with the size, nature, and risk level of your business; however, every program must be risk-based and advanced, rather than merely reactive. Knowing what an AML/CTF program should look like is just the beginning. Now it’s time to map out exactly how to build one that works in practice.

Click here to download VComply’s free AML Policy Template.

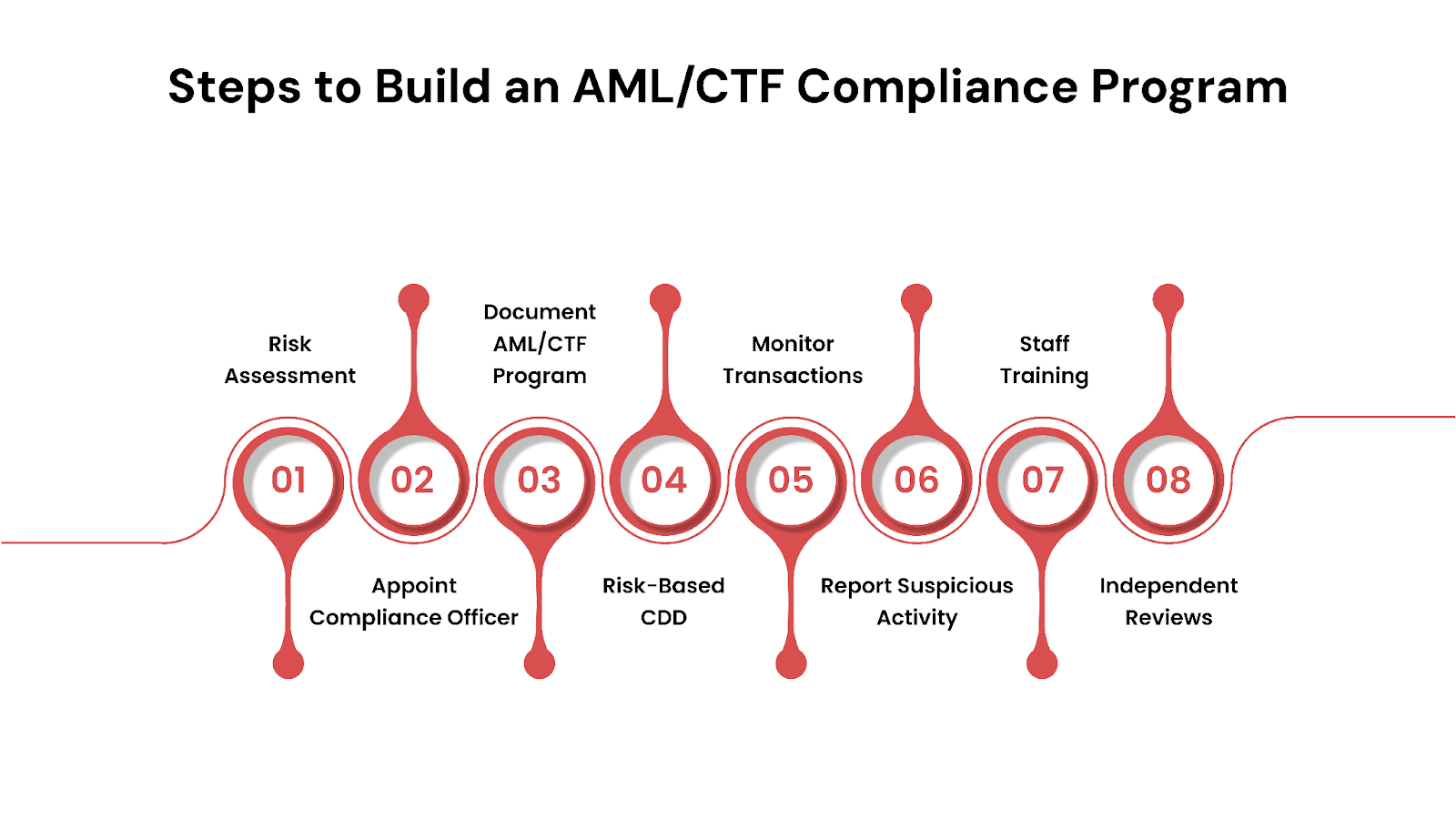

Steps to Build an AML/CTF Compliance Program

Designing a compliant and effective AML/CTF program involves more than templated documents. You must align people, policies, and technology around a shared goal: preventing financial crime without disrupting legitimate business.

Below are the key steps to build a robust AML/CTF program:

1. Conduct a Business-Wide Risk Assessment

Before writing any policies, it is essential to understand where your risk lies.

Begin by assessing the likelihood that your business will be targeted for money laundering or terrorist financing. This depends on your customer types, services offered, transaction channels, geographic exposure, and delivery models.

Key components to assess:

- Types of clients (e.g., politically exposed persons, offshore entities)

- Geographic risk (e.g., operations in or with high-risk jurisdictions)

- Products and services offered (e.g., high-volume or anonymous transactions)

- Delivery methods (online vs. in-person onboarding)

This risk assessment establishes the foundation for determining the level of rigor in your controls. Regulators will expect your entire program to reflect the findings in this document, so it must be thorough and regularly updated to ensure accuracy.

Read: The importance of risk assessment and risk management

2. Appoint an AML/CTF Compliance Officer

Every AML/CTF program needs a designated individual responsible for its implementation and oversight. This person acts as a bridge between regulatory authorities, senior management, and operational teams.

Core responsibilities include:

- Developing and updating AML/CTF policies: The officer ensures that internal policies stay aligned with regulatory changes and evolving financial crime risks.

- Overseeing internal compliance audits: They conduct or coordinate regular audits to assess the effectiveness of AML/CTF procedures.

- Monitoring suspicious activity reports (SARs): The officer reviews and assesses internal reports of suspicious behavior to determine whether regulatory reporting is required.

- Acting as a point of contact for law enforcement and regulators, they liaise directly with external authorities, providing requested documentation or clarifications during investigations or inspections.

The appointed officer must also be empowered with decision-making authority, access to company leadership, and continual training to respond effectively to new threats and compliance obligations.

3. Develop and Document Your AML/CTF Program

With risks and roles defined, it’s time to formalize the program itself. This involves drafting a clear, written document that outlines how your organization identifies, mitigates, and reports AML/CTF risks. Regulators will scrutinize not only the content but also whether it’s being applied consistently across departments.

Your documented program should include:

- Policies for customer due diligence and enhanced due diligence

- Risk classification matrices and control procedures

- Steps for monitoring and investigating transactions

- Procedures for suspicious matter reporting

- Internal governance, escalation paths, and review schedules

Avoid generic templates. Instead, customize the language and workflows to reflect your actual business operations, using insights from your risk assessment.

4. Apply a Risk-Based Customer Due Diligence (CDD) Approach

Customer onboarding is the frontline of AML/CTF defense. The program should define how you verify customer identity, screen for sanctions, and assess risk at the point of entry and beyond.

There are typically three levels of CDD:

- Standard Due Diligence: For low-risk customers, verify identity and understand ownership.

- Simplified Due Diligence: For very low-risk customers, less intensive checks are conducted.

- Enhanced Due Diligence (EDD): For high-risk customers, additional data sources, ongoing reviews, and senior management approval.

Common CDD elements include:

- Identity verification using government documents or biometric tools

- Screening against PEP (Politically Exposed Person) and sanctions lists

- UBO (Ultimate Beneficial Ownership) checks for legal entities

- Ongoing monitoring and periodic re-verification

Your approach must be adaptable. For example, onboarding a private client from a high-risk country will require a very different process from onboarding a local retail customer.

Read: A Complete Guide on Third-Party Risk Management

5. Establish Ongoing Transaction Monitoring Systems

After customer onboarding, the focus of your AML/CTF program should shift to continuously observing how those customers interact with your services. Ongoing transaction monitoring helps detect suspicious behavior as it happens, allowing you to respond before potential financial crimes escalate.

This process involves setting up systems, whether manual or automated, to track customer activity in real-time and flag anomalies that deviate from their usual behavior or industry norms.

Common red flags that may indicate suspicious transactions include:

- Large cash deposits without a clear source of income: Unexpected or undocumented funds, especially in high volumes, can be a sign of illicit activity.

- Frequent cross-border transfers to high-risk jurisdictions: Regular international payments to or from countries with weak AML regulations may warrant closer scrutiny.

- Structuring transactions to avoid reporting thresholds: Also known as “smurfing,” this involves breaking up large transactions into smaller ones to evade regulatory detection.

- Sudden spikes in account activity inconsistent with the customer profile: Unusual increases in transaction volume or frequency that don’t align with a customer’s known financial behavior can raise red flags.

These indicators should be clearly defined within your AML/CTF program and tied to actionable thresholds or rules. Smaller organizations might handle this monitoring manually, while larger firms often rely on AML software that uses predefined behavior models, machine learning algorithms, or statistical analysis to flag potential risks.

You should also establish a structured process for how alerts are handled:

- Who reviews the alert?

- How quickly must it be addressed?

- When is it escalated to compliance officers or authorities?

- What documentation must be maintained?

Clarity around these workflows ensures consistent action and accountability, key for both regulatory compliance and risk mitigation.

Read: Compliance Audits: A Guide to Ensuring Regulatory Adherence

6. Report Suspicious Matters Promptly

Suspicious transactions aren’t always obvious, but when they are, inaction isn’t an option. Your AML/CTF program must clearly define how suspicions are identified, handled, and reported. This is where most regulatory bodies draw a hard line: failure to report is treated as non-compliance, even if the activity turns out to be innocent.

Key steps include:

- Precise definitions of what counts as suspicious

- A direct, confidential path for employees to escalate concerns

- Internal validation and documentation

- Timely submission of Suspicious Matter Reports (SMRs/SARs)

Reporting suspicious activity is a high-stakes responsibility that needs precision, speed, and confidence. Your program should make that process second nature.

7. Train Staff on AML/CTF Responsibilities

A culture of compliance doesn’t happen without people. All staff, especially those in customer-facing roles, should receive AML/CTF training tailored to their specific responsibilities and updated annually.

Key training topics to cover:

- How to recognize red flags

- Steps for onboarding and verifying customers

- Internal reporting lines and escalation procedures

- Legal consequences of non-compliance

Make training engaging and measurable. Use quizzes, certifications, and real-life case studies. Maintain logs of completed training sessions for audit purposes.

8. Conduct Independent Reviews and Program Updates

No AML/CTF program is perfect on day one. Regular, independent reviews are crucial for evaluating the effectiveness of your controls and policies.

You can engage internal audit teams or external consultants to:

- Review CDD files for quality and completeness

- Evaluate how well transaction monitoring rules are working

- Test staff knowledge and incident handling procedures

- Benchmark your program against industry standards

Based on findings, you may need to revise your risk assessment, rewrite policies, or upgrade technology. Regulators expect this evolution and will view stagnation as a form of negligence. With so many moving parts, having a system like VComply that keeps everything organized and visible can make all the difference.

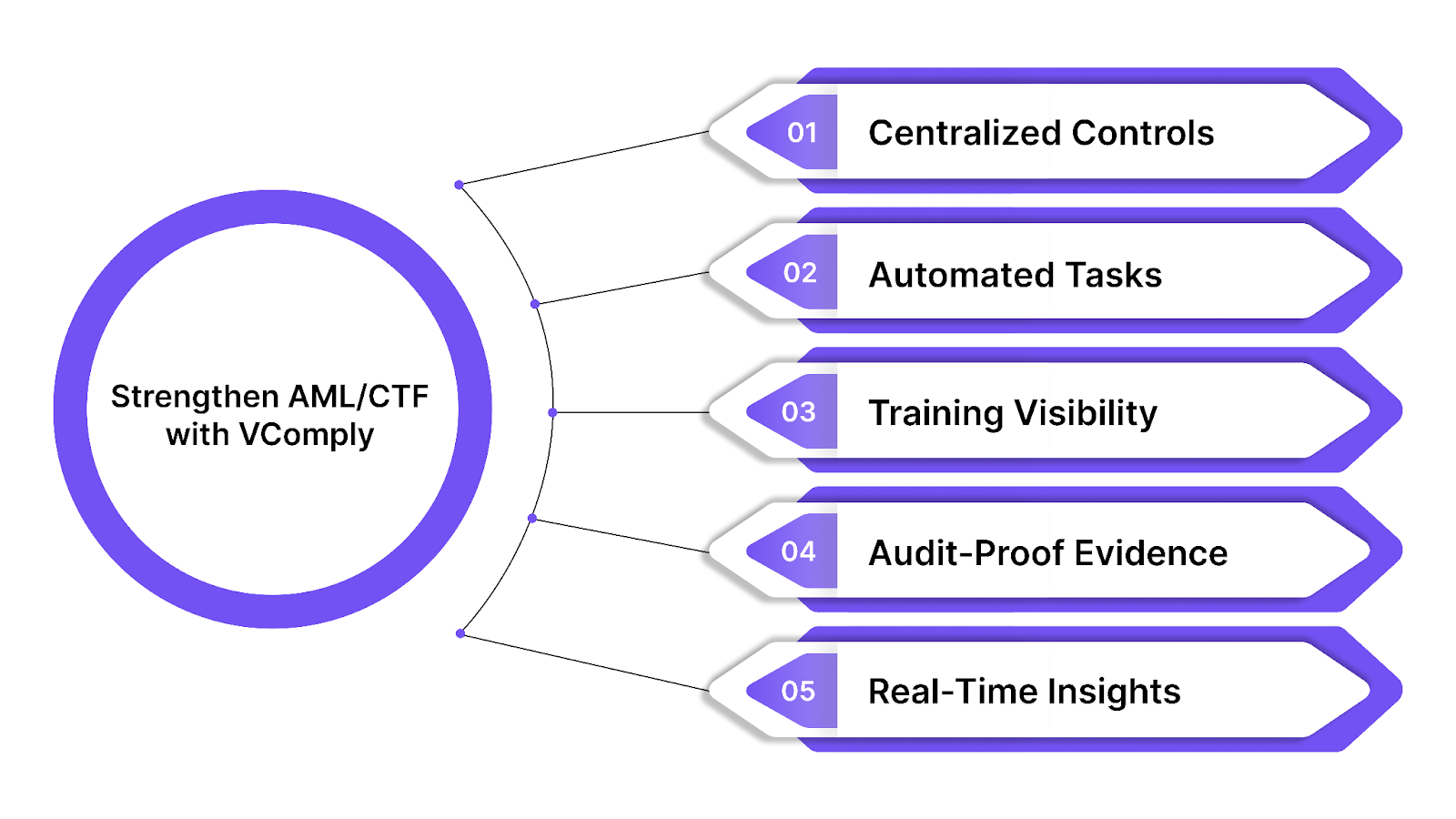

Strengthen Your AML/CTF Compliance Program with VComply

Building a compliant AML/CTF framework is just the beginning; maintaining it consistently and proving it under scrutiny requires control, visibility, and accountability. VComply helps you operationalize AML/CTF requirements with precision.

Here’s how VComply enables smarter, audit-ready compliance:

- Centralized Controls & Policy Oversight: Create, update, and distribute AML/CTF policies from one source of truth. No version confusion, no manual emails, just real-time access and accountability.

- Automated Assignments for Key Tasks: Ensure compliance officers and frontline teams never miss a deadline. VComply auto-assigns critical tasks like risk reviews, suspicious activity follow-ups, and internal audits, with reminders and status tracking.

- Training Visibility, Not Guesswork: Upload AML/CTF training content, track completion by role or region, and generate instant reports to demonstrate compliance during reviews or inspections.

- Organized, Audit-Proof Evidence: Whether it’s CDD records, SAR logs, or policy acknowledgments, store everything with timestamps and secure access, ready for regulator requests at any time.

- Real-Time Risk Insights: Identify gaps, delays, or overdue actions before they become compliance failures. VComply’s dashboards provide leadership with a live view of AML/CTF execution across teams.

Don’t just check the AML/CTF boxes; build confidence in your compliance program. Book a demo with VComply and get started.

Wrapping Up

Achieving AML/CTF compliance goes beyond fulfilling regulatory obligations. It plays a critical role in reducing the risk of financial crime and safeguarding your organization’s credibility. A compliant program requires consistent attention, starting with a clear understanding of risk, followed by well-documented procedures, ongoing staff training, real-time monitoring, and timely responses to suspicious activity.

Each phase of AML/CTF compliance, from onboarding and due diligence to reporting and audits, must be organized, transparent, and aligned with legal standards. Without the right systems in place, managing these requirements manually can quickly become inefficient and prone to error.

Start your 21-day trial of VComply today! No credit card. No delays. Just everything you need to get AML/CTF compliance under control.