The Ultimate Guide To Implementing Internal Controls

Implementing effective internal controls is not just a good business practice; it’s often a requirement to achieve legal and regulatory obligations and organizational objectives. This ultimate guide aims to demystify the world of internal controls, providing a comprehensive overview and actionable insights for organizations of all sizes and industries.

Key Takeaways (TL;DR)

-

Learn how internal controls safeguard organizational assets, enhance transparency, and ensure regulatory compliance across industries.

-

Understand the importance of preventive, detective, and corrective controls in minimizing business risks and fraud.

-

Discover how effective internal control frameworks like COSO strengthen governance, accountability, and operational efficiency.

-

Explore the challenges of manual control management and how automation eliminates inefficiencies and human errors.

-

See how VComply’s automated GRC platform simplifies internal control implementation, monitoring, and compliance management.

Internal Control refers to a system implemented and upheld by a company’s management to provide assurance in meeting business objectives, upholding policies and regulations, securing assets, ensuring operational efficiency, and maintaining the reliability of financial statements.

They are the policies, procedures, and activities that protect organizations from financial, operational, and strategic risks. They ensure that an organization operates efficiently, effectively, and ethically. The primary objective of internal control is to minimize risks and prevent fraud, errors, and mismanagement. These controls are designed to safeguard a company’s assets, ensure the accuracy of financial information, and help it achieve its objectives. Internal controls are important for various stakeholders within an organization and the broader business environment.

The controls of each company differ from those of others and are designed taking into account the size of the company and its structure. Efficient and effective internal controls help to achieve corporate goals.

Internal accounting controls ensure that a company’s financial reports comply with accounting principles generally accepted in the United States. Internal controls help prevent fraud by ensuring the integrity of financial records and promoting accountability. In addition, other rules also apply internally for specific industries, e.g., Healthcare, nonprofits, manufacturing, and retail, among many others. Manually managing internal controls: The loss by numbers, we’ve found that more than 50% of organizations manage their internal control procedures on spreadsheets. This results in a number of inefficiencies that include multiple version controls, errors due to copy-pasting of data, cross-departmental collaboration, and outdated data. Imagine the time your compliance teams spend on data curation and validation instead of analyzing this data and driving value-added activities.

As business activities and volumes expand and reliance on manual intervention increases, human error, omissions, and fraudulent manipulation can also increase significantly. Internal controls help minimize the risk of unexpected losses, fraud, and possible damage to the organization’s reputation. It helps protect the interests of the public and all other stakeholders in the organization. In addition, it also ensures that the organization correctly follows legal, regulatory, and other governance requirements, internal policies, procedures, and guidelines. Ultimately, an effective internal control environment helps the organization eliminate inefficiencies and strengthen business functions and processes towards business growth, better customer centricity, and profitability. The most prominent benefits of a robust internal controls procedure include:

- Helps mitigate risks – Internal controls are also powerful tools for risk management. They identify potential risks and vulnerabilities, allowing organizations to develop strategies for mitigation and contingency. This proactive approach minimizes the impact of unforeseen events and helps organizations adapt to changing circumstances.

- Stringent regulatory compliances – Many laws and regulations require organizations to use internal controls to achieve specific outcomes. These laws specifically require companies to use specific frameworks, as using a recognized framework brings discipline and transparency to your compliance efforts. This, in turn, reduces the likelihood of compliance violations that could lead to costly enforcement actions.

- Improves operational efficiency – Operational efficiency can be improved through the application of internal controls as this helps eliminate unnecessary and duplicate steps in a process or procedure. Improving operational efficiency allows management to obtain timely information about the organization that helps to review current operations and verify whether or not business goals are being met.

- Increased security – The first and foremost benefit of internal controls is the enterprise-wide protection they provide. Your business is significantly less vulnerable with a defense plan in place. Every business is at risk from business disruption, cyberattacks, market shifts, and more. By preparing ahead of time for these inevitable situations, you can sail through them successfully and move your business ahead.

- Helps reduce audit fees – Properly established internal controls reduce the need for external audit fees. When an organization provides a clear framework for the implementation of internal controls and their findings, it reduces the need for reviews or the need to rebuild all internal controls after external audit and verification.

- Timely preparation of financial statements – Timely preparation of financial statements helps management make future decisions for the company beforehand and also protects stakeholders and the company’s reputation. Regular financial statements help identify and correct small mistakes that help build trust and demonstrate company transparency.

- Recognition of the SOX Act – The main purpose of establishing SOX was to maintain accountability in an organization. Internal controls via efficient and effective financial reporting do the same. The SOX Act is a federal law enacted to protect investors and ensure that the organization provides reliable and accurate financial information. By complying with the SOX law, companies gain confidence in investors and in the company’s financial data management. Know more about SOX compliance with VComply

- Enhances accountability – Well-designed internal controls created with specific roles for key members help reduce errors and improve process performance. This leads to improved accountability when clear data transfer, data recording, and data sharing protocols are followed. Enhanced accountability means the company meets legal and regulatory reporting requirements.

- Helps keep duties segregated – Internal controls ensure that tasks are separated for different people as this prevents conflicts of interest and reduces the likelihood of financial mismanagement. Segregation of duties also ensures that a system of checks and balances is put in place so that not every person has access to all the data.

- Organized information – Properly organized data from any organization helps prepare for events such as litigation and external audits. Internal controls protect customers’ interests by creating systems that archive customer data or documents or by imposing restrictions. Organizing information also helps improve efficiency by ensuring the security of financial data that are accessed.

- Saves money – External financial reports are more reliable when good internal controls are in place. Additionally, the ability to see what is being done to avoid losses will help you improve those efforts and better allocate your funds. The controls also minimize lost profits caused by business disruption and avoid litigation and other forms of compensation that are often necessary for your customers after a risk event has occurred.

In addition, internal control compliance is designed to ensure the achievement of operational objectives, including the effectiveness of operations, accurate, reliable, and timely financial reports, and compliance with the country’s laws and regulations. Simply put, internal control compliance plays an important role in ensuring that the organization’s operational, strategic, compliance, and reporting goals are met.

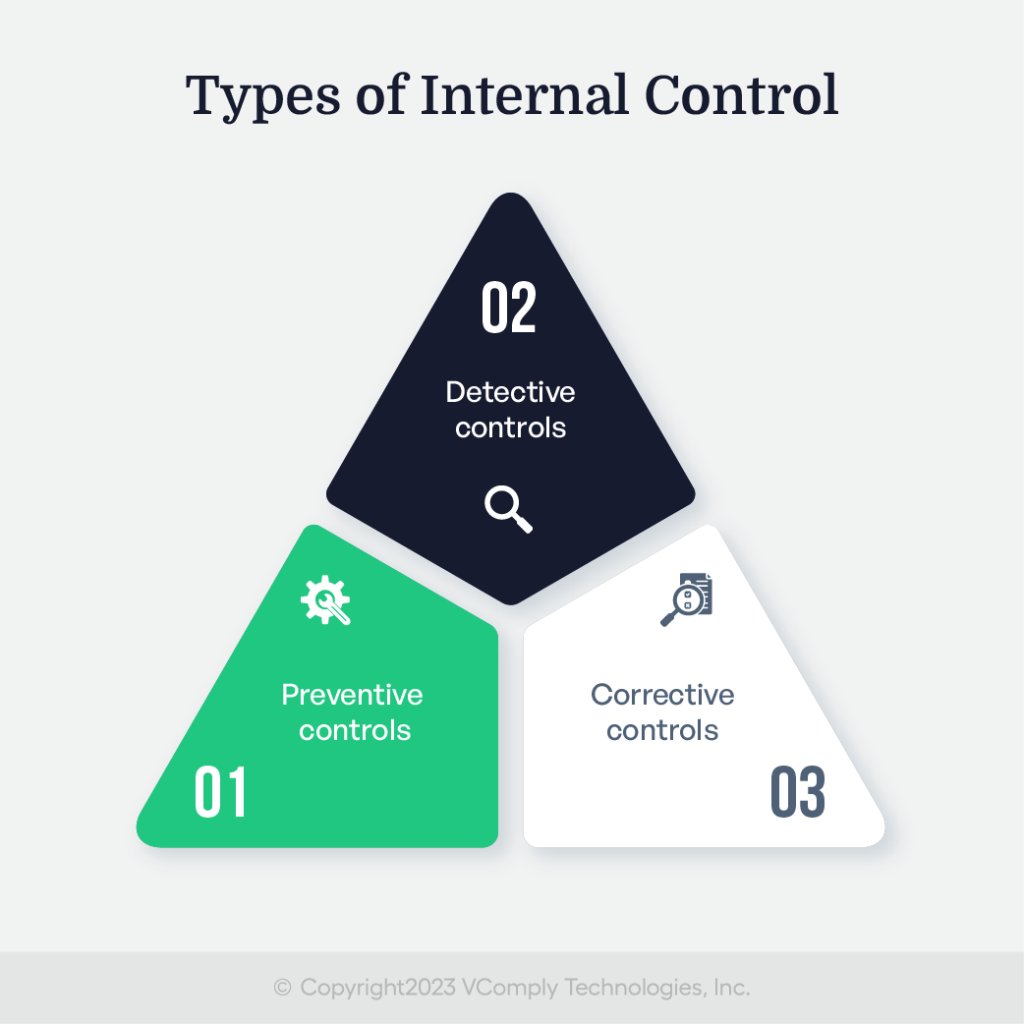

There are three main categories of internal controls: preventive, detective, and corrective.

Preventive controls

Preventive controls are measures taken to prevent an undesirable event from occurring in the first place. This broad category includes everything from key card access controls to segregation of duties and complex password requirements. Preventive controls are implemented after a risk assessment has determined which risks could affect different areas of your organization. Examples of preventive internal control include video surveillance or strategic placement of security personnel at points of entry, verification of identification data, and restricted access. Furthermore, firewalls, computer and server backups, training programs, and even routine drug testing are all types of preventive internal controls that are put in place to prevent the loss of assets and the occurrence of harmful events. The main preventive control measures are:

Access controls: They regulate who or what has access to corporate assets, including IT systems. These controls are a critical security concept that reduces risk to the business. Physical access control limits access to IT campuses, buildings, rooms, and physical assets. Security personnel are required to verify identification credentials or access key cards to enforce physical access control. Logical access control restricts connections to computer networks, system files, and data.

Pre-employment screening: Pre-employment screening is a process in which employers conduct background checks, drug tests, reference checks, and assessments. It is used in the recruitment process to screen out many unwanted candidates before investing in the onboarding process.

Having GRC software in place: GRC software helps an organization proactively identify and address compliance risks. It can safeguard an organization from the aftermath of regulatory actions through automated GRC tasks. A single HIPAA breach has a potential consequence of $4.24 million, along with a very long-lasting reputational dent on the organizations. Implementation of GRC software can save an organization from multiple issues in advance.

Detective controls

Detective controls are used to examine transactions and determine if errors have occurred. This allows executives to fix a problem before it causes more problems. Ideally, detective internal controls will discover an issue before it becomes a significant problem.

Examples

Some examples of detective controls are internal audits, reconciliations, financial reports, financial statements, and physical inventories.

Internal audits: An internal audit aims to assess compliance with company procedures, applicable laws, and international standards. Data and reports are checked for consistency and compliance. This internal control provides management and board value by identifying and correcting weaknesses in a process before external audits discover them. This can protect the organization from loss of certification and fines.

Financial reporting and reconciliations: Reconciliations are conducted to verify financial reporting between different sources. For example, comparing a bank statement to a company’s internal records is one form of reconciliation. Financial reports document the company’s income, expenses, cash flow, and financial health. It enables executives and investors to make more informed judgments about performance and opportunities for improvement. Unusual or unexpected numbers in financial reports and financial statements help identify unintentional errors and inappropriate actions.

Physical inventory counts: Physical inventory counts are performed regularly to ensure that actual inventories correspond to the records in business systems and financial statements. Physical inventory values directly affect the balance, so it is imperative that they are accurately reflected. Inventory discrepancy investigations can uncover system problems, accidental errors, and theft.

Corrective controls

The third type of internal control is corrective internal control. These are the controls performed after internal detective controls have identified a problem. Sometimes, even if all existing preventive controls are working as planned, they fall short. If an error or deficiency is discovered within the current security regime, corrective internal controls are implemented with identifiable internal controls to address previous deficiencies.

Corrective controls could include:

- Implement a more rigorous training process

- Update the policies

- Invest in new technology to protect against new threats

Corrective internal controls are inherently specific to failures and typical risks of your organization, previously assessed through comprehensive risk assessments or detection controls such as audits.

Examples

A few examples of corrective controls include:

Patch management

Patch management is the process of deploying and installing software updates. These patches are needed to fix software vulnerabilities.

Patches are often needed for operating systems, applications, and embedded devices. If a vulnerability is discovered after the software has been released, it can be fixed by a patch. Proper patch management protects the security of information by preventing data leakage and privacy breaches.

New/updated policies and procedures

Policies and procedures may be updated if an audit or other detective control identifies a loophole in the processes. For example, root cause analysis of an inventory discrepancy may reveal that employees are not trained enough to reduce areas that fail quality checks. Corrective controls include updated work instructions and training.

Disciplinary actions

Disciplinary actions are corrective actions taken in response to employee misconduct, rule violations, or poor performance. Discipline can take various forms, including a verbal warning, a formal warning, an unfavorable performance review, or even termination, depending on the severity of the situation.

Internal controls consist of five main components, established by the Committee of Sponsoring Organizations (COSO) and providing guidance to companies around the world. Known as the COSO framework, these five components are:

Control activities

Control activities provide a reasonable level of assurance that the entity’s objectives will be met. Although absolute assurance is not possible due to cost, collusion, human error, and management’s ability to override controls, having an internal control process can reduce the risk proponent to a significant level.

The key control activities in an internal control process include:

- Authorization to initiate or approve transactions should be limited to designated personnel. Permissions can be restricted by the type of transactions or the number of transactions.

- Segregation of duties means that a single employee is not responsible for all phases of a transaction.

- In general, an employee with physical access to an asset should not also be responsible for the accounting records related to that asset.

- Assets should be physically protected. Access to assets should be restricted. Reconciliations of assets to accounting records must be made regularly and reconciliation of items must be done in a timely manner.

- Physical assets must be counted regularly, and the results of the counts must be compared with accounting records.

- Inconsistencies should be reported to the appropriate administrators and investigated.

- Transactions must be properly documented, and records must be kept in an organized manner.

Control environment

Before dealing with any of the other components, the second most important step is to create the control environment. The control environment examines the behavior of top management and their ability to implement the necessary controls. It examines everything from the ethics of an organization’s top management to their integrity in dealing with any issues that may arise. The top management sets the tone for the rest of the organization, including human resource policies and procedures, management philosophy, and organizational structure. The control environment also includes the involvement of management and the board of directors to ensure that internal controls are being followed, as well as how employee responsibilities are assigned and managed.

Risk assessment

Once the control environment has been established, the next component to consider is risk assessment. Assessing a company’s risks is essential, as the risks must be identified before a control procedure is implemented.

Risks greatly vary from company to company, depending on the organization itself, its current control environment, or even a particular industry. Both internal and external risks must be identified so that an appropriate process can be put in place to mitigate the identified risk.

Risks may include:

- Public scandal

- Revenues not received or, if received, not accurately documented

- Improperly recorded assets are not used efficiently

- Assets that cannot be used to achieve the unit’s goals and objectives for personal use

- Information used for decision-making is not reliable, current, or available

Develop assessment criteria: This step ensures that team members assessing and prioritizing risks are using the same metrics to do so. High, medium, and low risk is the most common qualitative scale for measuring risk. Without these defined criteria, it will be difficult to interpret risk assessments in your company.

Assess risks: In this step, your team actually scores each risk against the scoring criteria. An important thing to remember is that this step should be iterative. Risk assessments can be conducted in a variety of ways, including online surveys, face-to-face interviews, group workshops, or benchmarking. Ultimately, the result should be a risk score for each risk based on likelihood and average impact on the organization.

Prioritize risks: While prioritizing risks based on your risk score from the risk assessment mechanism, risk prioritization is actually a downstream process that helps your organization broaden the view of risk beyond probability and financial impact. Prioritization should also include subjective criteria such as damage to reputation, health and safety, vulnerability, and other qualitative factors.

Information and communication system

The purpose of the information and communication system is to ensure that employees are aware of the objectives and goals of the unit, how they are to be achieved, and who is responsible for the specific tasks assigned to them. The information and communication system should also provide managers with reports containing operational, financial, and compliance information to monitor progress toward set goals and objectives. Using this, managers and stakeholders can make data-backed decisions.

Information and communication systems include:

- Written corporate policies and procedures

- The goals and objectives of the unit

- Documented unit policies and procedures

- Evaluation of performance

- Organization chart information and communication system that ensures employees know what they are supposed to achieve and how to do it

Monitoring

Monitoring ensures that the internal control system is working as designed. It must be conducted by supervisors and be focused on high-risk areas. Monitoring identifies changes in circumstances that may require modification to the internal control system.

Oversight and monitoring of internal control activities include:

- Timely review of transactions to ensure compliance with policies and procedures related to departmental accounting records

- Reviews of high-risk accounts or records, including employee payrolls and vacation records, trend assessments, review of supporting documentation, and unexpected counts of cash and other assets

- Documentation of software for employee licenses

- Reviews of tangible personal property and related records

- The follow-up to grievances, rumors, and allegations requires supervisory or management oversight

A test of control describes a systematic and methodical testing procedure used to evaluate internal controls. The objective of auditing the controls is to determine whether these internal controls are sufficient to detect or prevent the risk of asset mismanagement or unforeseen threats. A strong internal control system is essential for organizations to maintain accurate financial records.

There are several reasons for performing control testing in auditing. When an organization’s internal controls are working effectively, it reduces the need for additional substantive auditing procedures that can be time-consuming and expensive. Another purpose of these tests is to obtain more audit evidence to support the auditor’s statements.

The steps to test the internal controls are:

Inventory creation

Before establishing a reliable testing process, you should consider all important controls and document their activity in detail. When you have a complete and consistent control library, you can identify the basic details of each control and its impact on different departments or business units in the organization. It is not necessary to fully document all controls prior to testing, but an inventory of key controls can make the test easier and more effective.

Prioritization of required testing

Typical organizations have hundreds or even thousands of controls documented. Testing all of these controls is not viable, but the list needs to be streamlined and simplified for each individual test. For each control under consideration, determine its impact on the organization. Use this information to determine the type and frequency of testing.

Ask yourself whether the control required to demonstrate compliance with the main guidelines is crucial for regulatory purposes. Also, try to determine whether you have significant control over financial reporting and whether you believe that control is effective. Answer these questions to prioritize controls and help auditors focus on their work.

Often, specific regulations or compliance standards to which the organization is subject, such as SOX, GDPR, HIPAA, or PCI, guide the testing process and determine which controls are critical.

Designing the right test approach for control

The test approach is often dictated by the type of control. If the organization relies on a control to mitigate significant risks, it should assess it more frequently. You can also perform a design evaluation of the control before testing its functionality.

If you identify potential problems with the controller’s operation, you can suspend operational testing until the controller design is corrected.

Documentation and tracking

Although it may seem like a simple concept, an important aspect of test control is prioritizing and correcting problems found during testing. These fixes should be tracked until they are complete. The best practice is to verify fixes by running the test program again after giving time to fix to verify that all issues have been fixed.

Although internal check and internal control imply similar functions and are often used synonymously, they differ largely in their scope of work.

Internal check refers to the separation and delegation of tasks to the subordinate management of a company. Internal controls, on the other hand, are implemented to prevent, identify, or correct gaps, particularly in financial reporting.

Internal checks only address the functions of individual seniors after the activities and processes, while controls are managed and reviewed by everyone with equal responsibility. Because the latter directly affects the efficiency and productivity of organizations. For example, if a car has been manufactured as per the requirement, the respective employee might give the thumbs up to go for direct launch in the market and see the reaction of the newly launched car, but if the supervisor senses some fault in the mechanism and the internal control process that might jeopardize safety, he might ask to halt or postpone the launch until all the security parameters are cleared. The first is identified as an internal check, but the latter is associated with internal control implementation.

Though internal controls provide a plethora of benefits to organizations, they do have limitations as well if improperly implemented.

Notable limitations of internal controls are:

Collusion

Segregation of duties is one of the most commonly used internal controls in organizations. It is highly recommended that tasks be separated so that no employee has the power to commit fraud. However, employees can overcome this by working together through an elaborate process to cover up their fraud.

Human error

Human error can be another disadvantage of internal controls, especially when it comes to the reliability of manual processes and discretionary decisions. For example, errors can be made with manual inventory counts, and poor judgment can affect internal audit results.

Wherever possible, automated systems should be used to promote consistency and reduce human error. For example, scales in warehouses can be used to verify inventory counts. Automated systems can help reconcile accounting and financial records. Robust audit processes, along with management oversight, will support strong internal audit standards.

Management override

The risk here is that certain individuals with management authority can approve an exception to internal control. For example, the Chief Information Security Officer may have the authority to authorize elevated access privileges for individuals, but doing so inappropriately could undermine your access management controls.

System errors

The risk of automated system controls crashing without warning can prove to be a nightmare. An increasing number of companies are relying on automated system controls to maintain the security, availability, and integrity of their systems. However, if the setting to enforce encryption is overridden in a system update, you may lose an important privacy control if no one is made aware of the change.

Misjudgment

The risk denotes that you have misidentified controls to adequately mitigate the risk of your business or operating environment. Identifying appropriate internal controls is more of an art than a science, and you may find that the industry-leading vulnerability scanner isn’t right for your organization after you’ve identified the overlooked vulnerabilities.

For starters, developing an internal control framework for the organization can be an overwhelming and time-consuming activity. Most organizations don’t know where to start and wander off to find the right controls to begin with, which wastes valuable time and effort.

To simplify this process, the answer is a compliance management platform with a pre-built internal control framework. Whether your organization is struggling to manage cyber risk and meet cybersecurity goals, improve performance management, meet business goals, or meet regulatory requirements, VComply can simplify all of these tasks and streamline your efforts.

Compliance risk is regarded as one of the major risk factors for any organization. VComply specializes in tackling compliance risk using the GRC platform, which helps set up internal controls for managing regulatory compliance and maintaining industry standards.

VComply is a powerful compliance management platform with a pre-built internal control framework. It has features to create controls, assign them to concerned personnel, measure and review performance, and provide oversight to hold responsible individuals accountable. You can leverage the linked controls feature to instantly assign controls when the risk assessment identifies gaps in the system. VComply manages the coordination between the different parties interested in compliance with the obligation to comply and sends notifications and reminders. With its performance dashboard and compliance reports, C-level executives have a better overview and understanding of how the organization operates.

Some advantages of implementing VComply are:

- Automated control assignment, delegation, review, reporting, and evaluation of the effectiveness of organizational control.

- You can leverage the library of predefined regulations and compliance and control frameworks.

- Collaborate with teams and stakeholders using VComply’s control workspace.

- Automate your risk assessments and identify gaps.

- Link controls to risk and implement risk mitigation methods.

- Assign policies and content frames to generate automatic reports.

Conclusion

As the levels of uncertainty and chaos are rising exponentially day by day, organizations must be ready to tackle unforeseen challenges from all aspects. A thorough and well-designed internal control framework is the best weapon in the arsenal of organizations to defend themselves.

A successful approach to implementing internal control management must include defining the right outcomes for the organization, ensuring proper governance, and including internal control considerations in all new activities. Understanding this approach is critical to the success of an organization’s transformation efforts, along with operational efficiency.

Elevate your internal control management with VComply—book a live demo today!

Frequently Asked Questions

1. What are internal controls and why are they important?

Internal controls are processes and procedures designed to safeguard organizational assets, ensure accurate financial reporting, and promote compliance with laws and regulations. They help maintain transparency, accountability, and operational integrity across all departments.

2. What are the main types of internal controls?

Internal controls are typically categorized into preventive, detective, and corrective controls. Preventive controls reduce the likelihood of errors or fraud, detective controls identify issues that occur, and corrective controls address and resolve those issues effectively.

3. How do internal control frameworks like COSO help organizations?

The COSO framework provides a structured approach to designing, implementing, and evaluating internal controls. It strengthens governance, improves risk assessment, and enhances overall business performance by aligning controls with strategic objectives.

4. What challenges do organizations face with manual internal control management?

Manual control processes often lead to inconsistent documentation, human error, and delayed reporting. These inefficiencies make it harder to maintain compliance, respond to audits, and track risk exposures in real time.

5. How can automation improve internal control effectiveness?

Automation streamlines control testing, monitoring, and reporting, ensuring timely updates and greater accuracy. It reduces manual workload and provides continuous oversight of key compliance activities.

6. How does VComply simplify internal control management?

VComply’s automated GRC platform centralizes internal control documentation, assigns responsibilities, and monitors compliance performance in real time—helping organizations achieve transparency, efficiency, and stronger regulatory compliance.