PCI DSS Compliance Made Simple: Key Requirements and Core Standards

PCI DSS compliance often feels heavier than it should, especially when teams are juggling scattered card-data processes, rising audit pressure, and limited internal bandwidth.

Breaches of cardholder data keep executives awake at night because audit teams flag gaps, regulators impose fines, and acquirers raise rates. In the U.S. alone, 43% of investigated breaches in 2025 involved phishing or stolen credentials. By understanding the Payment Card Industry Data Security Standard (PCI DSS) requirements and core standards, you’ll be able to map your vulnerabilities and embed controls that reduce risk while simplifying oversight and audit readiness.

Quick Overview

- PCI DSS is a security rule set that protects payment card data by controlling how systems store it, move it, and guard it from attackers across U.S. environments.

- The 12 PCI requirements act as practical guardrails that shape everything from firewalls and encryption to access controls, logging, testing, and daily security habits.

- A PCI roadmap shows how an organization figures out where card data exists, identifies weak spots, fixes gaps, proves compliance, and keeps controls reliable throughout the year.

- The content lays out how PCI safeguards reduce breach impact, where teams commonly struggle, and which practices help maintain strong payment-security hygiene over time.

What is PCI DSS?

The Payment Card Industry Data Security Standard defines how card data must be handled across storage, processing, and transmission points so your environment stays secure. Most U.S. organizations discover compliance matters the moment acquirers start requesting SAQs, ROC reports, or audit evidence. Attacks often rise faster than internal controls can mature, leaving teams overwhelmed by what to fix first. Strong familiarity with PCI DSS gives you clarity on risks and a practical starting point for tightening payment-security governance.

A clear definition sets the stage, and understanding its purpose provides more clarity about why the framework demands strict attention.

Purpose of PCI DSS

PCI DSS exists to reduce payment-card fraud and help organizations manage risk in a predictable, structured way.

Here are the core goals this standard solves for businesses:

- Establishes a unified approach to protecting cardholder data so fragmented security practices don’t leave exploitable gaps.

- Ensures acquirers, merchants, and processors operate with consistent safeguards that reduce fraud across the U.S. payment ecosystem.

- Lowers the financial impact of breaches by embedding preventive controls that demonstrate due diligence.

- Gives organizations a clear language to use with banks, QSAs, and processors during assessments and audits.

Also read: Understanding Key Updates in PCI DSS v4.0

These goals form the foundation of the standard, and next, you’ll see the guiding principles that influence how PCI DSS operates in real-world environments.

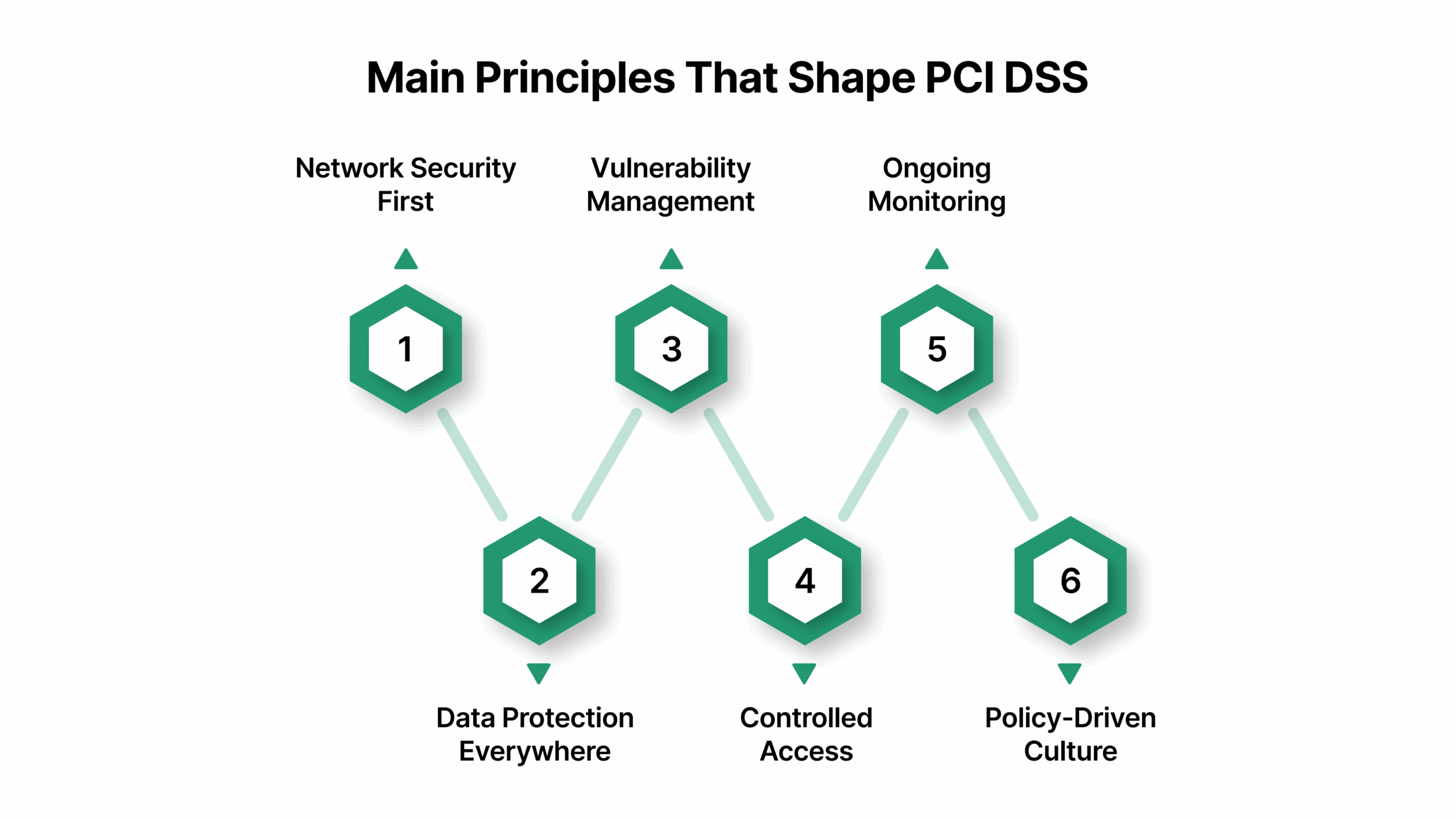

Main Principles That Shape PCI DSS

The entire standard is built on core security principles that guide how payment data must be protected throughout its lifecycle. Below is a breakdown of those principles in practical terms:

- Network Security First: A secure environment begins with limiting where card data can travel, segmenting critical systems, and controlling traffic pathways.

- Data Protection Everywhere: Encryption, key management, and tokenization help prevent attackers from misusing cardholder information even if systems are breached.

- Proactive Vulnerability Management: Continuous patching, scanning, and secure development reduce exploit windows that cybercriminals often target.

- Controlled Access: Least-privilege, MFA, and verified identities ensure only authorized people touch sensitive payment systems.

- Ongoing Monitoring: Alerts, logs, and integrity checks keep daily activity visible so threats are caught before spreading.

- Policy-Driven Culture: Documented rules help employees follow secure practices consistently across shifts, departments, and remote workflows.

These principles give the standard its structure, and the following section shows how they translate into the core PCI DSS expectations organizations follow.

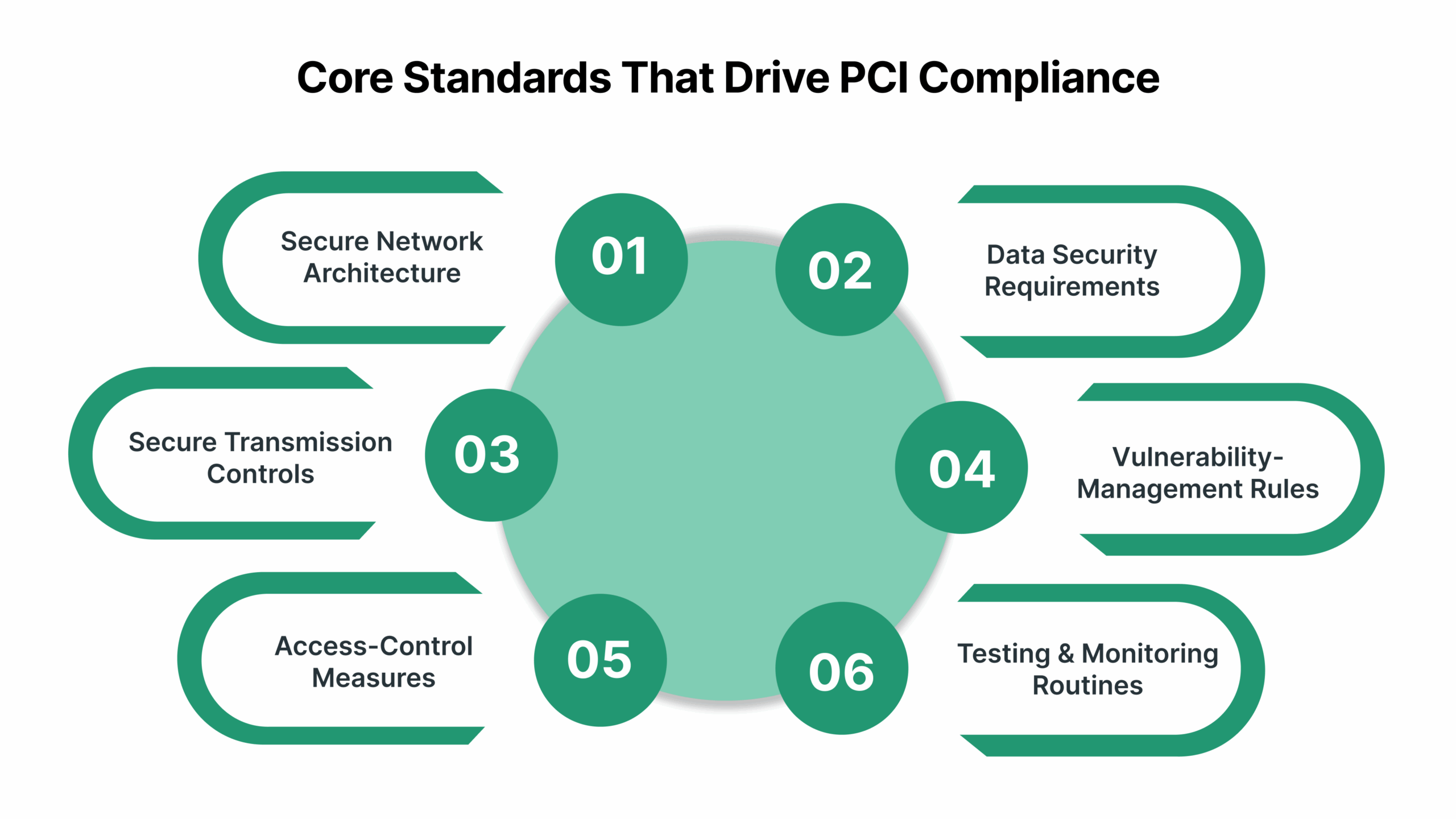

Core Standards That Drive PCI Compliance

PCI DSS defines core standards that shape how systems, people, and processes interact with card data across your environment. Here are those standards explained in business-friendly terms:

- Secure Network Architecture: Firewalls, segmentation, and hardened configurations form the backbone of a controlled payment environment.

- Data Security Requirements: Encryption, retention limitations, and storage controls keep cardholder information protected end-to-end.

- Secure Transmission Controls: Strong cryptographic protocols shield data moving across public and internal networks.

- Vulnerability-Management Rules: Patch cycles, scanning, and secure coding policies decrease exposure to known threats.

- Access-Control Measures: Identity verification, user-level permissions, and multi-factor authentication restrict unnecessary access.

- Testing & Monitoring Routines: Continuous monitoring, penetration testing, and log analysis ensure controls stay reliable year-round.

Also read: Understanding the Cost of PCI Compliance

Once these standards are understood, it becomes easier to break down the 12 actionable requirements that determine PCI DSS compliance.

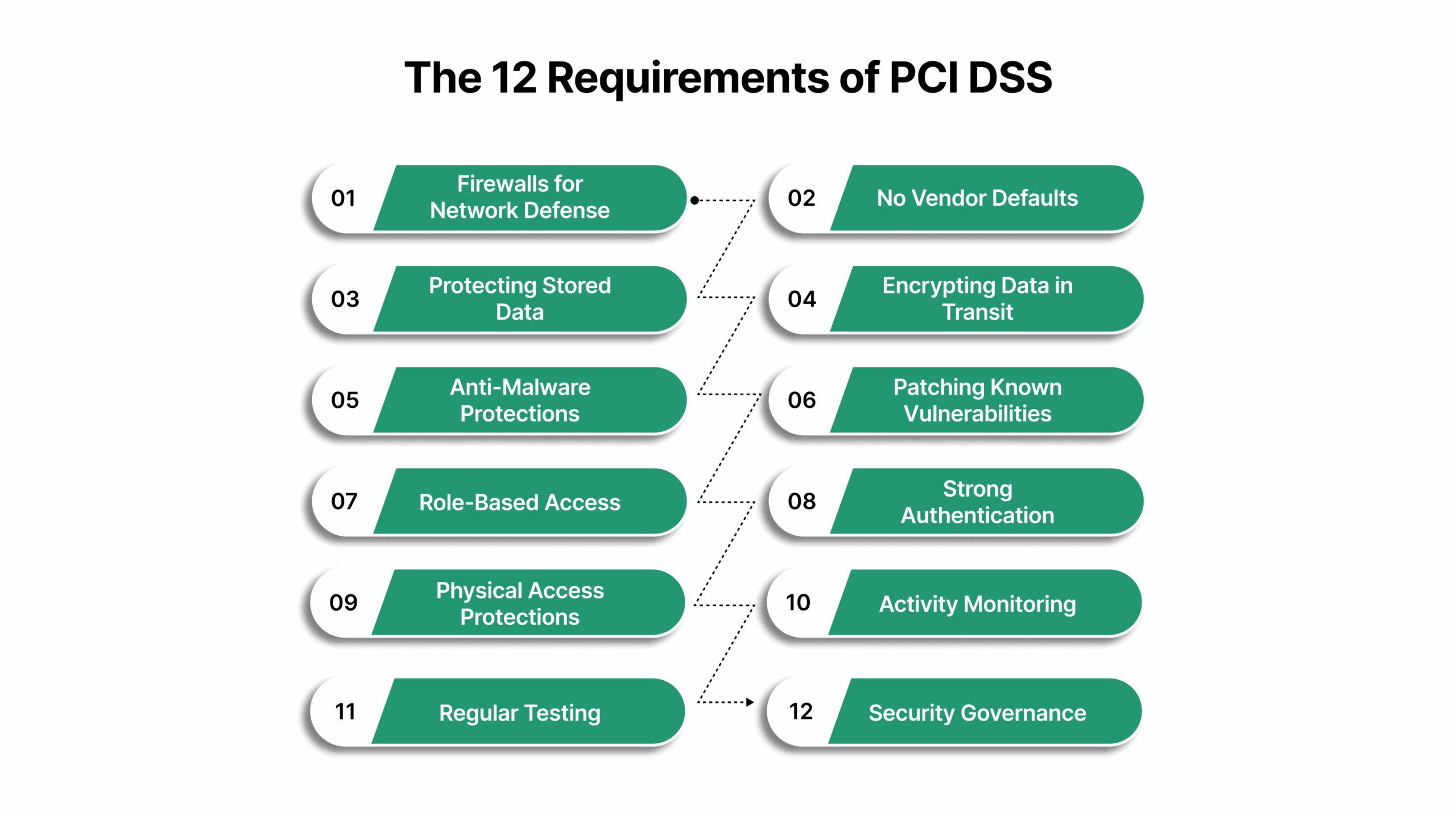

The 12 Requirements of PCI DSS

The 12 requirements act as detailed control statements explaining what you must implement to achieve Payment Card Industry Data Security Standard PCI DSS compliance.

Below is a practical breakdown of each one:

- Firewalls for Network Defense: Firewalls block untrusted traffic, reduce attack paths, and define clear security boundaries.

- No Vendor Defaults: Default settings expose systems, making configuration hardening a critical first step.

- Protecting Stored Data: Encryption and restricted storage help eliminate unnecessary card-data exposure.

- Encrypting Data in Transit: Secure protocols prevent attackers from intercepting payment information.

- Anti-Malware Protections: Modern anti-malware tools and behavioral analysis reduce the chance of compromise.

- Patching Known Vulnerabilities: Timely patches minimize threat windows and reinforce system integrity.

- Role-Based Access: Access tied to job roles ensures card data is available only where operationally required.

- Strong Authentication: MFA supports secure identity verification and blocks unauthorized logins.

- Physical Access Protections: Badges, locked rooms, and surveillance help guard on-premise systems.

- Activity Monitoring: Centralized logs ensure visibility into actions that affect payment security.

- Regular Testing: Scans and penetration tests validate that security controls truly work.

- Security Governance: Policies guide teams on what to do, how to respond, and how to maintain consistency.

With the requirements in place, the next logical step is understanding how organizations actually work through PCI DSS from start to finish.

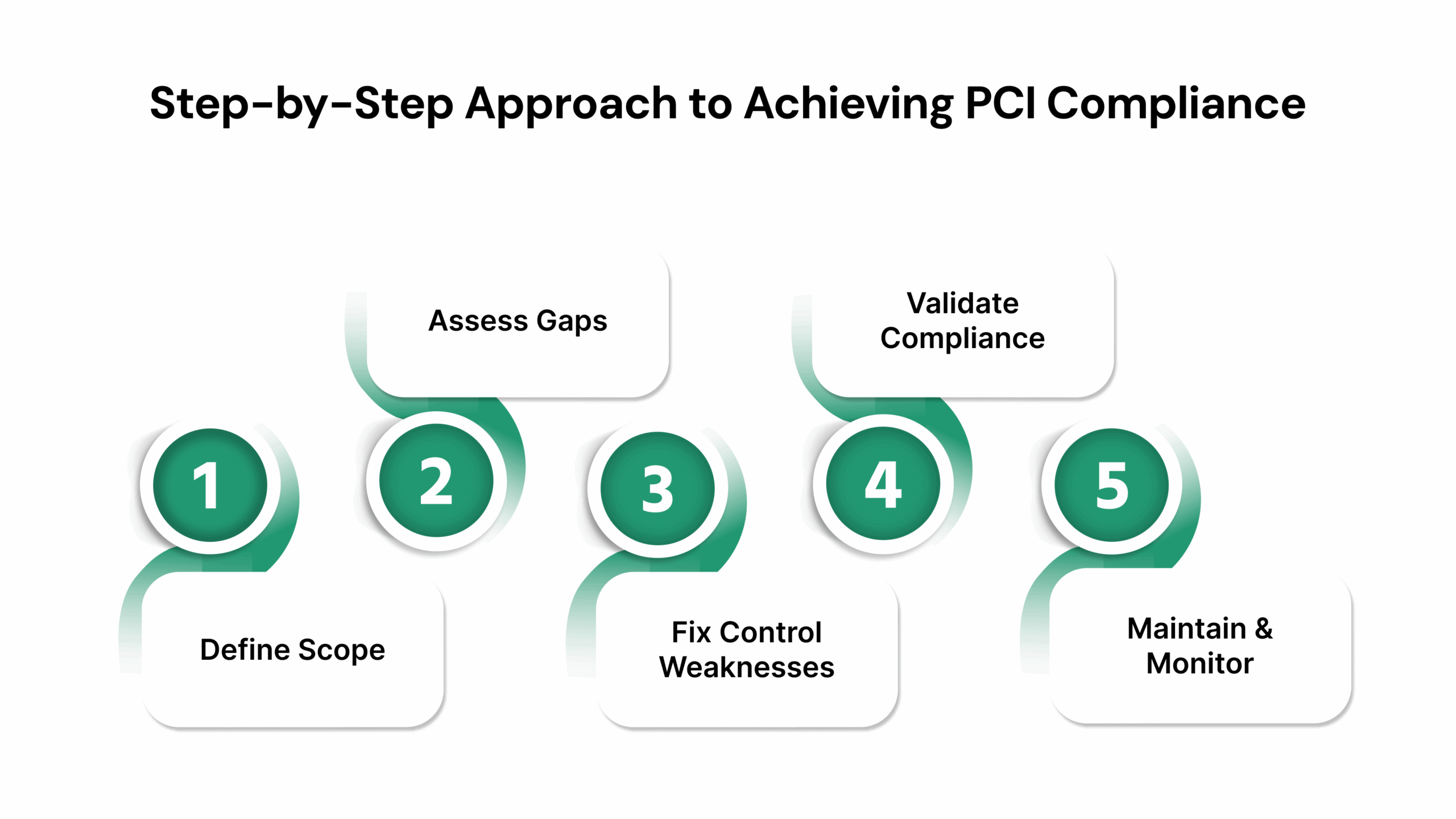

Step-by-Step Approach to Achieving PCI Compliance

This roadmap helps your team move from uncertainty to a structured PCI DSS industry-aligned compliance program.

Here is the complete sequence organizations follow:

1. Define Scope

A precise scope identifies every system, asset, vendor, and integration touching card data. Teams usually uncover unexpected storage points once logs and workflows are examined thoroughly. Proper scoping prevents bloated PCI environments that drain time and budget.

2. Assess Gaps

A structured gap assessment reveals what controls exist, what’s missing, and what auditors will examine closely. Findings help you prioritize risks and allocate resources toward the most critical weaknesses. Clear documentation also sets the stage for smooth remediation planning.

3. Fix Control Weaknesses

Focused remediation ensures encryption, MFA, segmentation, patching, and logging reach the required maturity. Control owners need clear deadlines and responsibilities to complete updates effectively. Strong remediation dramatically increases audit confidence and reduces rework.

4. Validate Compliance

Validation depends on merchant level and may involve SAQs or full QSA audits. Evidence, interviews, and system reviews form the foundation of this step. Well-organized documentation accelerates the process and limits follow-up requests.

5. Maintain & Monitor

Ongoing monitoring helps controls stay effective long after the audit window closes. Alerts, log reviews, and policy updates keep security aligned with evolving threats. Strong maintenance prevents sudden gaps that could jeopardize your next assessment.

Completing these steps offers a clear path to compliance, and it helps to look at the business value that comes from staying aligned with PCI DSS.

Business Value of PCI DSS

PCI DSS gives organizations practical governance and technical advantages that directly strengthen operational resilience. Here are the core benefits that matter for U.S. businesses today:

- Lower Breach Exposure: Embedded controls reduce the likelihood of attackers exploiting weak payment workflows.

- Lower Financial Risk: Documented controls help limit fines, penalties, and forensic-investigation fees.

- Stronger Brand Trust: Customers perceive your brand as safe when payment security is transparent and well-managed.

- Cleaner Internal Processes: Standardized workflows reduce confusion between security, IT, operations, and finance.

- Improved Audit Readiness: Predictable control structures make PCI-related and non-PCI audits more efficient.

Also read: In-depth guide to Compliance Management System

Even with these benefits, teams still face common hurdles, and the next section outlines the challenges that often get in the way.

Common Obstacles in PCI DSS

Teams commonly run into issues that slow down PCI progress or increase audit complexity. Here are the typical roadblocks that create friction:

- Scoping Blind Spots: Hidden data flows, integrations, and vendor systems often inflate or distort the actual PCI footprint.

- Evidence Management Burden: Manual documentation turns audits into exhausting, multi-week exercises.

- Technical Skill Gaps: Encryption, segmentation, logging, and MFA require specialized configuration knowledge.

- Version Changes: PCI DSS v4.0 introduces new flexibility and maturity expectations that stretch small teams.

- Cross-Team Misalignment: Security requirements often clash with operational priorities, delaying implementation.

Knowing the roadblocks gives you a sharper view of what to avoid, and the following best practices help create a smoother compliance journey.

Best Practices for PCI Implementation

Successful PCI programs follow tested practices that make compliance smoother and more sustainable. Below are the best practices that increase your success rate:

- Document Every Data Flow: Detailed mapping reveals hidden databases, flat files, SFTP streams, and shadow services.

- Segment the Environment: Proper segmentation reduces PCI audit scope and cuts remediation workload dramatically.

- Enforce Privileged-Access Controls: MFA, JIT access, and strict provisioning prevent misuse of sensitive systems.

- Automate Monitoring & Evidence: Automation prevents missing logs, stale proof, or incomplete control checks.

- Provide Regular Employee Training: Trained staff reduces human errors, phishing exposure, and policy violations.

- Run Pre-Audit Assessments: Early assessments catch small issues before auditors elevate them to findings.

Strong habits make PCI work more manageable, and the next part explains how a compliance platform supports these efforts day to day.

How Compliance Platforms Support PCI?

Compliance platforms help operationalize PCI Payment Card Industry data security standard requirements by turning manual, chaotic work into structured workflows.

Below are the ways platforms add measurable value:

- Control Automation: Automated reminders, workflows, and evidence requests prevent tasks from falling through the gaps.

- Centralized Documentation: All PCI artifacts sit in one repository, so audits don’t require last-minute scavenger hunts.

- Visibility Into Gaps: Dashboards highlight risks and overdue tasks before they escalate into auditor findings.

- Cross-Team Coordination: Teams coordinate tasks and approvals without relying on email chains or spreadsheets.

- Policy & Version Control: Policy updates stay consistent and traceable across teams and yearly cycles.

- Support From Tools Like V-Comply: Platforms such as V-Comply provide PCI templates, audit logs, role assignments, and control-tracking built for US-based organizations.

Understanding their role provides context for how specialized tools fit into PCI operations, which leads directly into how V-Comply supports this work in practice.

Strengthen PCI DSS Compliance with V-Comply

Managing PCI DSS becomes far easier when every requirement, task, and piece of evidence sits inside one structured system instead of scattered tools. V-Comply gives your team a clear, repeatable way to satisfy payment-security obligations across all 12 PCI DSS requirements without drowning in manual work.

Here’s how Compliance Ops in V-Comply directly supports PCI DSS execution:

- Pre-Loaded Framework Library (PCI-ready controls): A built-in PCI DSS control set helps map requirements instantly, eliminating guesswork when assigning responsibilities or defining evidence.

- Automated Workflow & Task Management: Automated tasks ensure firewall reviews, log checks, access-control certifications, patch cycles, and encryption validations happen on schedule, as core activities auditors expect.

- Evidence & Document Management: Centralized evidence storage keeps screenshots, policy versions, access logs, and test results audit-ready, reducing the scramble typically seen during QSA assessments.

- Real-Time Dashboards & Alerts: Dashboards highlight overdue PCI tasks, missing artifacts, and failing controls so gaps don’t linger until audit season.

- Integrations & Collaboration Tools: Seamless connections with tools like Slack, Teams, Gmail, and Dropbox allow control owners to submit PCI evidence and complete tasks within their daily workflow.

Start building a faster, cleaner, and more predictable PCI DSS program. Try V-Comply’s free trial today.

Wrapping Up

A strong PCI DSS program gives your business a safer payment environment, clearer operational structure, and fewer surprises during audits or regulatory reviews. A well-built approach also reduces financial exposure from breaches while bringing consistency to every part of your card-data lifecycle. With a platform like VComply, your team gains the structure, automation, and visibility needed to manage PCI tasks without the usual manual burden. Centralized workflows, dashboards, and evidence collection help you stay prepared long before a QSA audit begins.

Take the next step toward streamlined PCI DSS readiness. Book a V-Comply demo today.

FAQ

Any organization that stores, processes, or transmits payment card data must comply with PCI DSS. This includes merchants, service providers, processors, gateways, and SaaS platforms connected to card transactions. Compliance applies regardless of business size or transaction volume.

Compliance timelines depend on system complexity, documentation readiness, and the number of gaps found during assessment. Smaller environments may complete the process in weeks, while larger enterprises may require several months. Consistent monitoring shortens future renewal cycles.

Non-compliance can lead to fines, increased transaction fees, mandatory forensic investigations, and potential loss of card-processing privileges. Breach-related expenses also rise significantly when required controls are missing. Reputation damage often becomes harder to recover from than financial penalties.

Small merchants must still validate compliance even if payments flow through hosted or third-party processors. Outsourcing reduces scope but does not remove responsibility for securing local systems, endpoints, and policies. SAQs (Self-Assessment Questionnaires) often apply in these cases.

PCI DSS validation is typically required annually, with additional quarterly scans for many merchants and service providers. Certain payment partners may request more frequent checks based on risk. Ongoing monitoring ensures the environment stays compliant between assessments.