Digital Banking Compliance in 2025: What to Know & How to Choose the Right Compliance Toolkit

With the rise of digital banking, compliance requirements are becoming more intricate. Digital banks have to follow a variety of regulations to ensure customer safety, protect data privacy, and maintain financial integrity. For those overseeing compliance—whether it’s a risk manager, compliance officer, or executive—staying updated on the latest rules and best practices is a must. This blog will walk you through the key compliance requirements digital banks need to meet in order to build trust and avoid any legal issues.

Digital banking has rapidly transformed how people manage their finances, with 69% of the U.S. population using digital banking services as of 2023. This figure is projected to rise to over 79% by 2029, highlighting the growing shift towards online banking.

As digital banking continues to expand, the complexity of compliance requirements also increases. Digital banks must adhere to various regulations designed to ensure customer safety, data privacy, and financial integrity.

For those responsible for compliance, whether risk managers, compliance officers, or executives, staying informed about the latest regulations and best practices is essential. This blog will cover the key compliance requirements digital banks must meet to maintain trust and avoid legal pitfalls.

Key Takeaways (TL;DR)

-

Understand why compliance must be embedded into digital banking operations—not treated as optional.

-

Discover how evolving AML, KYC, and data privacy laws shape digital bank obligations.

-

Learn how automation streamlines regulatory tasks, minimizes risk, and enhances audit readiness.

-

See how strong internal controls and risk management protect data, trust, and transparency.

-

Explore how VComply helps digital banks stay compliant, scalable, and future-ready with ease.

Why Compliance Can’t Be an Afterthought

Regulators aren’t just setting expectations, they’re enforcing them. Recent U.S. enforcement actions show that gaps in AML and compliance processes come at a high cost:

- TD Bank was fined $3 billion for AML failures and placed under the oversight of a court-appointed compliance monitor.

- LPL Financial paid $18 million after the SEC found repeated lapses in its AML procedures.

- Block, Inc. (formerly Square) was fined $40 million for major shortcomings in its BSA/AML compliance program.

These penalties highlight a simple truth: digital banks can’t afford to treat compliance as a checkbox. It needs to be built into the core of operations, proactively, not reactively.

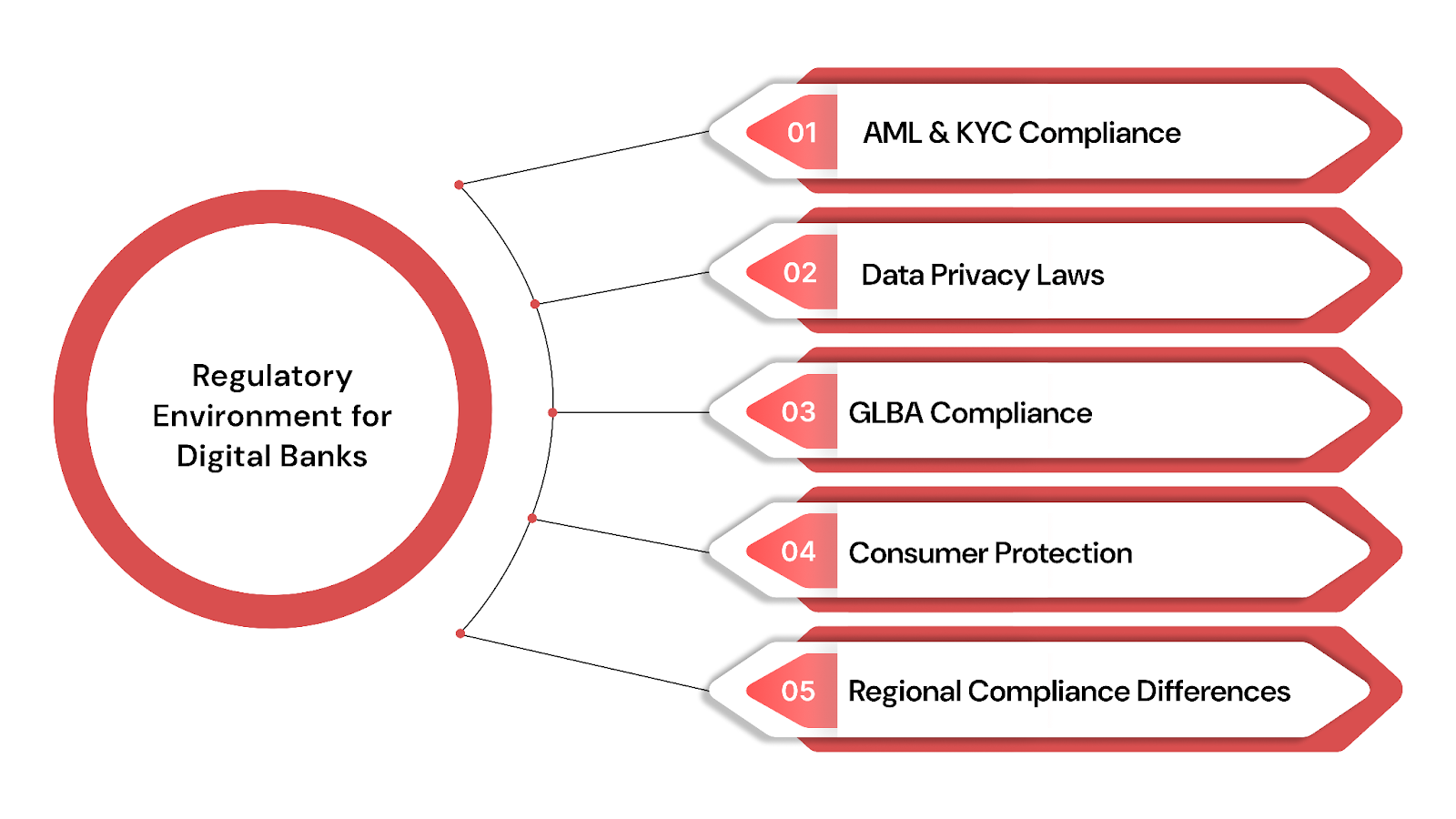

Understanding the Regulatory Environment for Digital Banks

As digital banking continues to grow, so does the regulatory environment governing it. Digital banks are subject to various local and global regulations designed to ensure consumer transparency, fairness, and security. Let’s break down the most significant compliance regulations that digital banks must manage:

1. AML (Anti-Money Laundering) & KYC (Know Your Customer) Regulations

AML and KYC regulations ensure that financial institutions do not become conduits for money laundering, terrorist financing, or other illicit activities. These regulations require digital banks to verify the identities of their customers before they can open accounts or engage in financial transactions.

- AML monitors and reports suspicious activities that could indicate illegal financial activities, including fraud or money laundering.

- KYC involves verifying the identity of clients, ensuring that banks only serve legitimate customers, and maintaining robust records for regulatory scrutiny.

For digital banks, staying compliant with AML and KYC regulations involves integrating identity verification processes into every transaction. The challenge lies in balancing regulatory requirements with customer convenience, ensuring that these processes don’t hinder the user experience while meeting strict legal standards.

2. GDPR and Data Privacy Laws

For digital banks, protecting customer data is central to both compliance and trust. In the U.S., the primary regulation governing data privacy is the California Consumer Privacy Act (CCPA). It grants users rights over their data, including access, deletion, and control over data sharing, and applies to businesses handling data of California residents, regardless of where the company is based.

Meanwhile, EU-based digital banks operating in the U.S. (or serving EU customers from the U.S.) are still required to comply with the General Data Protection Regulation (GDPR). GDPR applies to any organization, regardless of location, that processes the personal data of individuals in the EU.

That means:

- GDPR governs how EU customer data is collected, stored, and shared, even by U.S. branches of EU firms

- CCPA governs how the data of California residents is handled, even by foreign companies operating in the state

For multinational digital banks, this creates a layered compliance obligation. They must implement frameworks that respect both GDPR and local U.S. regulations like CCPA, ensuring robust privacy practices across jurisdictions.

3. GLBA (Gramm-Leach-bliley Act)

The Gramm-Leach-bliley Act (GLBA) is a foundational data privacy law for U.S. financial institutions, including digital banks. It mandates that financial organizations not only disclose how they collect, share, and protect customer data, but also implement technical and procedural safeguards to do so securely.

GLBA is built around three core provisions:

- The Financial Privacy Rule: Requires institutions to provide clear, written privacy notices to customers that explain data collection practices and opt-out rights. Digital banks must deliver this notice at account opening and annually thereafter, covering everything from how customer data is used to which third parties may receive it.

- The Safeguards Rule: Demands that institutions develop, implement, and maintain a written information security program. This must include risk assessments, continuous monitoring, employee training, and protocols to manage third-party service provider risks.

- The Pretexting Provision: Protects consumers from social engineering tactics—like phishing or impersonation—that may be used to obtain personal information fraudulently. Banks must have controls in place to detect and prevent unauthorized access attempts.

For digital banks, GLBA compliance goes beyond just having a privacy policy. It requires ongoing oversight of data flows, third-party relationships, and internal access controls. This often involves cross-functional coordination between product, legal, security, and compliance teams, as well as regular testing of controls to ensure audit readiness.

Click here to download VComply’s free downloadable policy template

4. Consumer Protection Regulations

Consumer protection regulations are in place to safeguard customers’ interests and ensure that digital banks do not engage in unfair practices. These regulations include rules around transparency in pricing, clear communication of terms, and fair dispute resolution processes.

Digital banks must ensure that:

- Their marketing materials and product offerings are transparent and honest.

- They clearly outline fees, interest rates, and other charges to avoid deceptive practices.

- Customers have access to effective channels for resolving complaints and disputes.

The implementation of consumer protection regulations varies depending on the jurisdiction. In the U.S., the Consumer Financial Protection Bureau (CFPB) oversees these protections, enforcing rules around fair lending, transparent disclosures, and dispute resolution in banking services.

5. Differences in Compliance Requirements Across Regions

Compliance requirements for digital banks can vary widely depending on the region in which they operate. While many of the regulations mentioned above are global, digital banks must adapt to local rules and frameworks, which can differ significantly.

Digital banks in the U.S. are subject to various federal and state regulations, such as the Bank Secrecy Act (BSA) for anti-money laundering, the Dodd-Frank Act for consumer protection, and CFPB guidelines for fair lending practices. Regulations focus heavily on transparency, data protection, and consumer rights.

For digital banks that operate in multiple regions, maintaining compliance becomes even more challenging due to the need to monitor and adapt to different regulatory environments. With a clear understanding of the regulatory environment, the next crucial step for digital banks is effective risk management.

Also Read: Financial and Regulatory Compliance Management Software

Risk Management and Internal Controls

The growing complexity of digital banking brings a broad spectrum of risks that must be carefully managed. Whether securing customer data or maintaining financial stability, implementing robust internal controls and auditing practices is essential for safeguarding operations and ensuring compliance.

Types of Risks Digital Banks Face

Digital banks are exposed to various types of risks, each with distinct challenges and potential consequences:

Cybersecurity Risks

As digital banks rely heavily on technology, they are prime targets for cyberattacks. These can include data breaches, phishing attacks, and denial-of-service threats. Cybersecurity risks not only endanger customer data but also have the potential to damage a bank’s reputation. Ensuring robust defenses, such as end-to-end encryption, two-factor authentication, and regular security audits, is essential to mitigating these risks.

Operational Risks

These risks arise from the failure of internal processes, systems, or external events. For digital banks, operational risks can occur due to technology failures, human error, or external factors such as natural disasters. Preventing such risks involves creating a culture of continuous improvement, regular testing of systems, and ensuring that all teams are well-trained to handle emergencies.

Financial Risks

Digital banks must also manage financial risks, including credit, liquidity, and market risks. This involves evaluating and monitoring the creditworthiness of borrowers, ensuring that there is enough liquidity to meet customer demands, and protecting the bank from market fluctuations. Proper financial risk management ensures that the bank remains solvent and capable of withstanding financial stress.

While understanding the types of risks is crucial, it’s equally important to have robust measures in place to manage and mitigate these risks. This is where strong internal controls and regular audits come into play.

Get your copy of VComply’s e-book on future-ready risk management program for financial services.

Importance of Internal Controls and Auditing

Internal controls are at the bottom of any organization’s risk management strategy. For digital banks, internal controls provide a framework for preventing fraud, ensuring regulatory compliance, and maintaining operational efficiency. A strong internal control system helps:

- Prevent errors and fraud through established checks and balances.

- Ensure accurate financial reporting, which is critical for regulatory compliance and transparency.

- Promote accountability, ensuring that roles and responsibilities are clearly defined and adhered to.

Auditing plays a vital role in verifying the effectiveness of these internal controls. Regular internal and external audits help understand potential vulnerabilities in systems and processes, while also ensuring that all operations align with regulatory requirements. By conducting audits, digital banks can demonstrate their commitment to transparency and accountability.

Now that we’ve covered the importance of internal controls and auditing, let’s look at the key tools and processes digital banks can implement to enhance their risk management framework further and stay on top of compliance.

Key Tools and Processes for Managing Risks and Maintaining Compliance

To effectively manage risks, digital banks must leverage the right tools and processes:

- Risk Management Software

Digital banks can use advanced risk management software to monitor and assess potential risks. These tools can automate risk assessment processes, track changes in regulations, and offer real-time reporting. Automated risk dashboards and alerts help banks stay on top of emerging risks and respond swiftly to mitigate them. - Compliance Management Systems (CMS)

CMS tools are essential for helping digital banks track and manage their compliance obligations. These systems provide a centralized platform to manage all aspects of compliance, from regulatory reporting to audit trails, ensuring that the bank remains up to date with the latest requirements. - Case Management Systems for Fraud and Risk Monitoring

Modern case management systems are central to how digital banks detect, investigate, and respond to fraud. Rather than just flagging suspicious transactions, these systems consolidate alerts, assign risk scores, and route cases to the right teams for review. Powered by AI and machine learning, they analyze behavioral patterns across accounts, identifying anomalies in real time.

The advantage? Digital banks can move from isolated alerts to structured investigations, tracking every action taken, documenting findings, and escalating risks with full audit trails. This reduces manual effort, speeds up resolution times, and strengthens compliance posture across the board.

- Training and Awareness Programs

Regular training sessions for employees are key to fostering a risk-aware culture. Employees should be educated on the bank’s internal controls, cybersecurity best practices, and how to recognize and report suspicious activity. Ongoing education ensures that all staff members are equipped to handle the risks they may encounter in their day-to-day roles.

By combining these tools and processes, digital banks can manage risks more effectively and ensure compliance with the ever-evolving regulatory landscape. While effective risk management and internal controls are essential for maintaining compliance, the growing complexity of regulatory requirements and the volume of data involved make it increasingly difficult to manage manually.

This is where compliance automation comes into play, offering a streamlined approach to ensure digital banks remain compliant while minimizing the risk of human error.

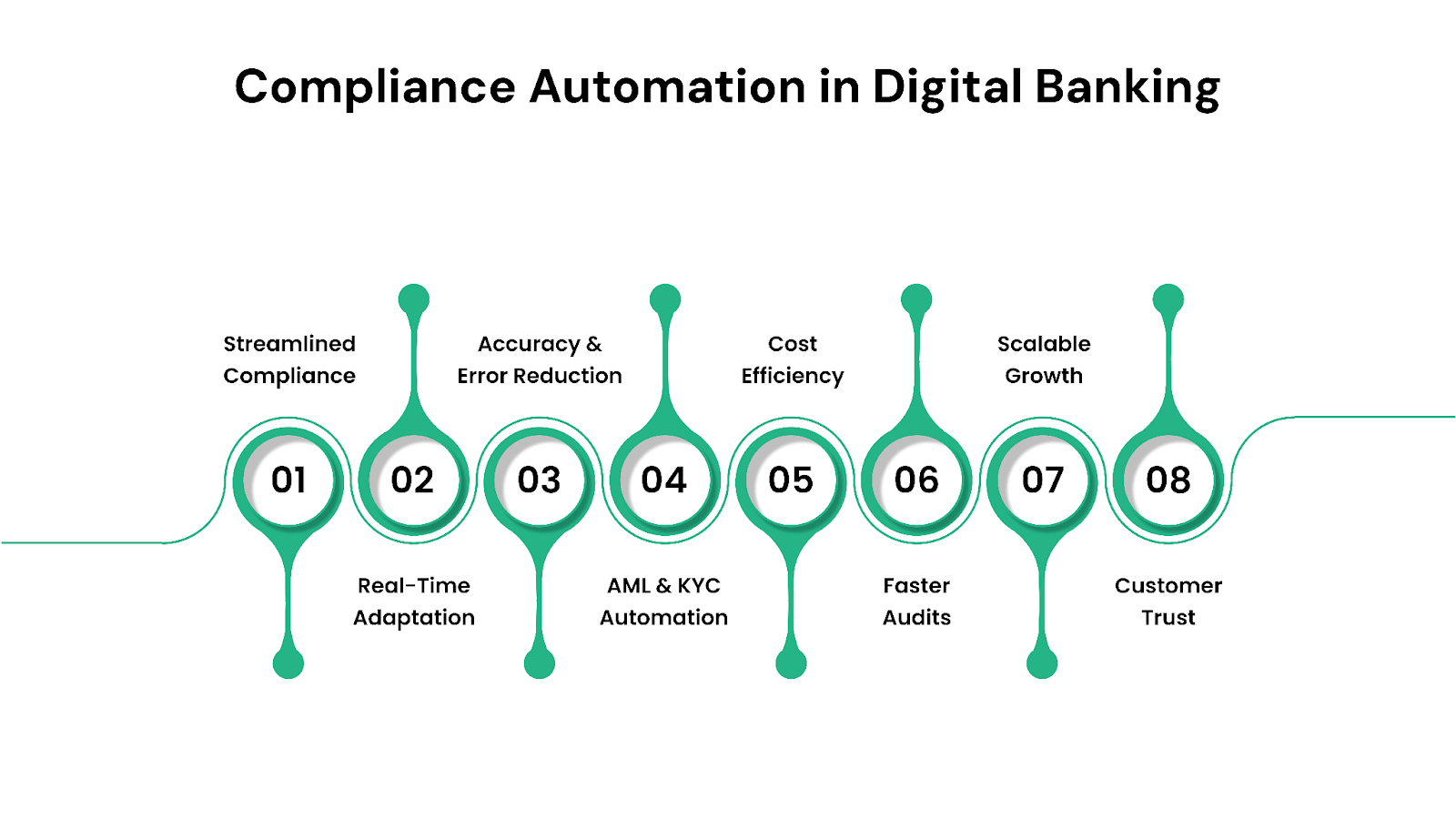

Compliance Automation in Digital Banking

As digital banking becomes more widespread, staying compliant with a growing list of regulatory requirements can be complex and resource-intensive. Compliance automation has emerged as a critical solution, allowing digital banks to manage these challenges effectively and efficiently. Here’s why automating compliance is invaluable for digital banks:

1. Smooth Compliance Tasks

Automation reduces the manual effort involved in routine compliance tasks like monitoring transactions, conducting KYC verifications, and preparing regulatory reports. This frees up valuable resources, allowing the bank to focus on core activities such as customer experience, business growth, and innovation, without sacrificing compliance standards.

2. Real-Time Adaptation to Regulatory Changes

Regulatory frameworks evolve constantly, and keeping up with these changes manually is a daunting task. Automated systems ensure that digital banks can automatically adjust compliance processes whenever there are updates or new regulations. This proactive approach reduces the risk of non-compliance due to outdated procedures, keeping the bank agile and in line with the latest legal requirements.

3. Enhanced Accuracy and Reduced Risk of Human Error

Compliance processes that rely on human intervention are prone to errors. Automating routine compliance checks minimizes human involvement, ensuring that tasks are completed with greater consistency and accuracy. This dramatically reduces the risk of errors, which could otherwise lead to costly fines, damage to the bank’s reputation, or even legal action.

4. Efficient AML and KYC Monitoring

Anti-Money Laundering (AML) and Know Your Customer (KYC) are two of the most critical compliance areas for digital banks. Automated tools continuously monitor customer activity for suspicious behavior, conduct real-time background checks, and update records, ensuring banks are not only compliant but also vigilant in preventing financial crimes. Automation makes it easier to meet AML regulations and ensures that KYC procedures are always up to date.

5. Cost Savings and Resource Efficiency

Maintaining compliance manually requires significant time, resources, and manpower, all of which can drain the bank’s operational budget. By automating compliance processes, digital banks save on operational costs and reduce the need for extensive compliance teams. These savings can be reinvested into more critical business areas like customer acquisition, technology upgrades, or product development.

6. Faster Audits and Reporting

Automated compliance systems document and log every action taken within the bank’s compliance framework, making audit trails clearer and more accessible. This reduces the time and effort required to prepare for audits and ensures that regulatory reporting is accurate and timely. Banks can quickly generate reports that meet regulatory deadlines without scrambling at the last minute, ensuring transparency and accountability.

7. Scalability to Support Growth

Maintaining manual compliance across different regions, services, and customer bases becomes increasingly challenging. Compliance automation systems grow with the bank, easily adapting to new regulations, markets, and customer segments. This scalability allows banks to stay compliant as they scale operations globally or diversify their services without adding excessive manual oversight.

8. Enhanced Customer Trust and Experience

Compliance automation safeguards the bank’s operations and enhances customer trust. By maintaining a strong and visible commitment to security, privacy, and fair practices, digital banks can build stronger relationships with their customers. Customers are more likely to trust a bank that adheres to regulatory requirements and can demonstrate its compliance practices transparently.

While automating compliance processes is essential for managing regulatory requirements, digital banks must also address a critical aspect of their operations: data protection and privacy. As customer data becomes a prime asset, ensuring its security and privacy is a regulatory obligation and a matter of trust.

Also Read: Building a Strong Privacy Program Framework: A Practical Guide for Compliance Success

Data Protection and Privacy Considerations

Data protection and privacy are paramount in an age where digital banks manage vast amounts of sensitive data. Adherence to data protection regulations not only prevents legal consequences but also ensures that customers’ personal and financial information remains secure. Let’s explore the key data protection considerations that digital banks need to prioritize:

1. Key Data Protection Laws

To safeguard customer information, digital banks must comply with various data protection laws. These regulations require banks to:

- Obtain explicit customer consent for data collection and processing.

- Provide customers with the right to access, correct, or delete their data.

- Ensure transparency in how data is used, processed, and shared.

Failing to comply with these laws can lead to severe penalties and damage to the bank’s reputation, making strict adherence essential for both legal compliance and customer trust.

2. Data Encryption and Secure Storage Practices

As cyber threats continue to grow, data encryption plays a crucial role in protecting customer information. Encryption transforms sensitive data into an unreadable format that can only be accessed with a decryption key. This is especially important for financial data, such as account details and transaction histories, which are prime targets for cybercriminals.

In addition to encryption, secure storage practices ensure that data is kept in safe environments, whether on-premises or in the cloud. Banks must ensure that data is stored in encrypted formats and that access control mechanisms are in place to limit unauthorized access. These practices help mitigate the risk of data breaches and maintain compliance with privacy laws.

3. Retention Policies and Legal Compliance for Data Usage

Digital banks must implement clear data retention policies to manage how long customer data is stored and ensure that it is not kept longer than necessary. These policies should align with regulatory requirements that mandate data deletion once it is no longer needed for legal or operational purposes. Compliance with data retention laws ensures that data is not exposed unnecessarily and protects the bank from legal liabilities.

Additionally, digital banks must have mechanisms to ensure that data usage complies with the principles outlined in data protection laws. This includes ensuring that data is used for its intended purpose, is processed with customer consent, and is not shared with unauthorized third parties.

With data protection and privacy firmly in place, digital banks now face a broader set of challenges in meeting their compliance requirements.

Also Read: People, Process, and Technology: The Three Pillars of Effective Compliance Management

Compliance in Digital Banking: Challenges and How to Respond

For digital banks, compliance isn’t just about keeping regulators happy; it’s about protecting customer trust while moving fast in a landscape that’s anything but static. But staying compliant is rarely straightforward. Below are some of the more persistent (and costly) challenges digital-first banks are navigating today.

Adapting to a Shifting Regulatory Landscape

From evolving anti-money laundering (AML) policies to new consumer data rights frameworks, regulatory updates rarely slow down. For digital banks operating across multiple states or partnering with vendors handling sensitive data, the ability to track and adapt to these changes isn’t just a nice-to-have. It’s essential. Yet many still rely on static documentation, siloed teams, or outdated processes that delay critical updates.

The Operational Burden of Manual Compliance

Compliance tasks, monitoring transactions, preparing reports, and reviewing audit logs can quickly turn into operational bottlenecks. When these processes are handled manually, they eat into team time and increase the likelihood of human error. For smaller digital banks and fintechs, this creates an unsustainable drag on both efficiency and cost.

Privacy Risks Hidden in Plain Sight

Encryption and access controls are table stakes, but true data privacy involves much more, especially when it comes to understanding who has access to what, how long data is retained, and how quickly the organization can respond to breaches or audit requests. These gaps often go unnoticed until they’re exposed by an incident.

Reporting That Doesn’t Scale

As digital banks grow, so does the complexity of their reporting obligations. Systems that worked at launch often struggle to keep up with regulatory submissions, especially when data lives across multiple tools. The result? Inconsistencies, version control issues, and fire drills during audits.

While no single strategy eliminates these pressures entirely, banks that prioritize visibility, automation, and internal alignment are in a far better position to keep pace. The next section explores how this can be implemented in practice, highlighting proven strategies that reduce risk without hindering growth.

What Smart Compliance Looks Like in Practice

Staying compliant doesn’t always mean growing your headcount or drowning in documentation. For digital banks looking to scale sustainably, the real opportunity lies in building systems and habits that make compliance part of how you operate, not something bolted on after the fact.

Here are a few principles that leading digital banks are leaning on:

Automate with Intention

Automation shouldn’t replace judgment, but it should reduce manual overhead where consistency matters. Banks that automate recurring tasks like KYC verification, suspicious activity alerts, or regulatory reporting don’t just save time, they build more reliable systems. The key is to choose tools that integrate cleanly into your existing workflows and leave a clear audit trail behind every action.

Make Compliance Everyone’s Business

It’s easy to isolate compliance in a single team. But the best-run banks treat it as a shared responsibility. That means product teams understand the regulatory implications of a new feature, ops teams flag risks early, and leadership gets a clear, ongoing view of exposure. Regular training helps, but what really makes the difference is weaving compliance into daily decision-making.

Build for Audit-Readiness, Not Just Audit-Response

Most audit issues don’t come from bad intentions; they come from messy data, unclear ownership, or poor documentation. The banks that stay ahead don’t wait for audit season. They log, tag, and document as they go, making audit-readiness a byproduct of good operations, not a last-minute scramble.

Choose Tools That Scale with Regulation

It’s not just about handling today’s rules. It’s about being ready for what’s coming. Whether it’s evolving AML thresholds, new reporting formats, or state-by-state variations in data privacy law, compliance software needs to adapt fast, without requiring months of rework. Prioritize platforms that are built with flexibility in mind.

Staying compliant doesn’t have to slow you down. Designed for digital-first banks, VComply brings together everything you need to manage compliance in one platform, from automating KYC and AML workflows to streamlining regulatory reporting and audit preparation.

With real-time updates, secure data handling, and built-in flexibility, VComply helps banks reduce operational costs while staying ahead of evolving requirements. It’s not just about meeting today’s standards; it’s about building a framework that supports long-term growth and resilience.

How VComply Supports Digital Banking Compliance

Digital banks face unique compliance challenges, from ensuring data protection to evolving regulations. VComply offers a comprehensive set of services customized to help digital banks streamline their compliance processes. Here’s how VComply can support your digital banking operations:

- Automated Compliance Reporting: VComply automates compliance reporting, ensuring timely submissions and meeting all regulatory requirements. This eliminates manual work and reduces the risk of human error.

- Real-Time KYC & AML Monitoring: With VComply, automate your Know Your Customer (KYC) and Anti-Money Laundering (AML) checks, ensuring smooth verification and continuous monitoring for suspicious activity, all while meeting regulatory standards.

- Data Privacy and Security Compliance: Compliance with privacy regulations like GDPR and CCPA is made easier with VComply, helping digital banks securely store and manage customer data while maintaining transparency for audits.

- Risk Management and Audit Readiness: VComply equips banks with real-time risk management tools, enabling effective risk tracking and mitigation. Additionally, its audit-ready system ensures you’re always prepared for compliance checks.

- Regulatory Updates and Adaptation: Keep up with changing regulations using VComply’s automatic updates that adapt workflows to maintain compliance with evolving legal standards.

Want to simplify your compliance processes and stay ahead of the curve? Request a demo today and discover how VComply can help you streamline compliance management, reduce risks, and enhance operational efficiency.

Wrapping Up

Compliance isn’t just about staying out of trouble; it’s about building operational clarity, safeguarding customer trust, and staying agile as regulations shift. For digital banks, the challenge isn’t knowing what to comply with, but how to manage it all without slowing down the business.

That’s why many forward-looking teams are moving away from manual processes and point solutions, and instead adopting centralized systems that bring visibility, automation, and audit-readiness into one place.

If you’re looking to reduce overhead, improve reporting accuracy, and stay current with changing laws, a dedicated compliance platform can help you get there faster and with fewer risks.

Start your 21-day free trial with VComply and explore how streamlined compliance can support your next stage of growth.