Risk Based Compliance Management – Making It Work for Banks

Banking compliance in 2026 is no longer limited to meeting regulatory requirements after they are issued. Banks and financial institutions now need a proactive, risk-based compliance model that can keep pace with regulatory change, cyber threats, fraud risk, AI adoption, third-party dependencies, data privacy expectations, and rising board-level scrutiny.

As banking operations become more digital and interconnected, compliance teams are expected to do more than interpret regulations. They must translate regulatory obligations into controls, policies, workflows, monitoring activities, reporting, and evidence across business units. This requires a stronger connection between compliance, risk management, internal audit, cybersecurity, operations, and leadership.

Risk-based compliance management gives banks a practical way to prioritize resources based on the level of exposure across products, processes, customers, vendors, geographies, and regulatory obligations. Instead of treating every requirement the same, banks can focus attention on the areas that carry the greatest financial, operational, legal, and reputational risk.

Key Takeaways (TL;DR)

-

Learn how risk-based compliance management helps banks tackle regulatory complexity while optimizing operational efficiency.

-

Understand why integrating governance, risk, and compliance (GRC) frameworks is vital for modern banking success.

-

Explore how technology, AI, and automation are transforming compliance reporting, risk monitoring, and fraud prevention.

-

See how adopting a proactive, data-driven compliance culture strengthens transparency, collaboration, and risk accountability.

-

Discover how VComply’s no-code GRC platform empowers banks to centralize, automate, and streamline compliance effortlessly.

Since 2009, regulatory fees have increased dramatically relative to banks’ earnings. In addition, the scope of the regulatory approach and scrutiny are continuously expanding. Non-compliance can result in heavy penalties.

In 2025, global banks and financial institutions were fined approximately $3.8 billion for AML, KYC, sanctions, and customer due diligence failures. Although this was lower than the $4.6 billion recorded in 2024, enforcement did not ease evenly. Penalties declined in North America but rose sharply across EMEA and APAC, signaling that regulators are continuing to test whether financial institutions have effective controls, monitoring, escalation, and evidence in place.

While most regional and small-scale entities and major banking enterprises have some form of compliance framework in place, there are still a number of questions related to banking compliance that go unanswered.

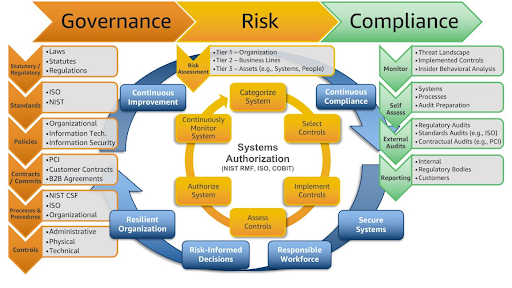

The traditional banking compliance model was developed at a different time and for a different purpose, primarily as a compliance arm for the legal department. Compliance organizations used to publish internal bank guidelines and regulations largely in an advisory capacity with a narrow focus. It was mostly attributed to the identification and management of real risks. However, the traditional approach provided a limited understanding of the underlying business operations and risks, as well as very little insight into the regulatory requirements from the business perspective. Back in the day, banks played safe and tried to constrain risk management within the parameters of the 20th-century playbook. Being so accustomed to the siloed approach and archaic processes, many banks, even now, are still struggling with fundamental front-line control environment issues as compliance activities are typically isolated. Also, there is no clear connection to the broader framework of risk management, governance, and processes.

With new regulations knocking on the doors of banking institutions at regular intervals, it is crucial to ensure continuous compliance to keep things under control. Many regulatory compliance practices in banking are new and evolving, with stringent implementation deadlines putting further pressure on banks. Banking institutions face the challenge of keeping up with the proliferation of regulations regarding risk and compliance management. Banks must have a strong infrastructure and highly skilled staff for compliance management to ensure the new standards. The existing risk management framework will help to manage risks of different types and levels. A streamlined risk management process would enable the bank to identify, monitor, and control compliance risks proactively. Routine risk management solutions and ad hoc practices need to be replaced with a robust risk management system. The merging of different risk factors, the reference to different compliance standards, and the integration of different audit processes are only possible through an integrated company-wide architecture. In addition to facilitating regulatory compliance, it tracks potential violations to avoid legal penalties and business opportunity restrictions. Connected banking includes end-to-end process automation to mitigate risk. Efficient digital integration with partners, customers, regulators, and government agencies facilitates proactive risk and compliance management. Gartner cautions that performing typical compliance activities individually is an unsustainable approach. Compliance programs must function as integrated steps in banking operations rather than being a separate and siloed process.

As more organizations in the banking and financial services industry rely on technology to complete transactions, GRC is more important than ever. GRC in banking and financial services is about:

- Managing risks to sensitive stakeholder data and maintaining the confidentiality and privacy of financial transactions.

- Compliance with industry regulations on fair practices, safe banking, and financial services activities.

- Implement governance at all levels of a banking or financial institution to meet the organization’s specific needs.

Although in the banking industry, GRC is designed to mitigate risk to stakeholder data, the GRC requirements may vary based on geographic location and banking and financial ecosystem. GRC is also vital to keep banks and financial services organizations fully operational to support the day-to-day needs of businesses and individuals. For example, the United States government classifies financial systems as critical infrastructure. If left unaddressed, the risks to the banking industry could disrupt the operations of many institutions and affect the livelihoods of US citizens. The importance of a GRC platform for the banking industry:

- Protect privacy for sensitive digital transactions.

- Identify cybersecurity threats before they can affect entire organizations and ecosystems of banking and financial services.

- Fix banking and financial services management gaps that could lead to fraudulent transactions.

- Monitor data processing of sensitive cardholder data to mitigate data risks from cybercriminals.

When it comes to sensitive banking and financial services transactions, earning customer trust is crucial to sustaining your business. A GRC platform like VComply can help you demonstrate your commitment to keeping transactions fair and secure to meet the needs of your customers.

How Banks Can Make Risk-Based Compliance Management Work in 2026

Risk-based compliance management is no longer a theoretical framework for banks. It has become a practical necessity. Banks are operating in an environment shaped by regulatory pressure, fraud risk, cyber threats, third-party dependency, AI adoption, payments innovation, customer due diligence expectations, and growing board-level scrutiny.

In the U.S., regulators continue to treat compliance risk as a key supervisory area. The OCC’s FY 2025 Bank Supervision Operating Plan identified BSA/AML, countering the financing of terrorism, OFAC, consumer compliance, CRA, and fair lending as compliance focus areas, while also emphasizing cybersecurity, third-party risk, payments, enterprise change management, and operational resilience. The OCC’s Spring 2025 risk perspective also stated that compliance risk remains elevated due in part to BSA/AML and consumer compliance risks associated with elevated fraud levels, account access concerns, and evolving business models.

This means banks need compliance programs that do more than document requirements. They need programs that identify risk, prioritize action, assign ownership, monitor controls, track remediation, and produce evidence. The goal is not to treat every regulation, customer segment, product, or process the same. The goal is to focus effort where the bank’s exposure is highest and where weak controls could create financial, legal, operational, or reputational consequences.

1. Expand the Compliance Function From Advisory to Active Risk Ownership

In many banks, compliance teams historically played an advisory role. They interpreted laws, reviewed policies, provided guidance, and responded to regulatory questions. That role is still important, but it is no longer enough.

In 2026, the compliance function must be more actively involved in the bank’s risk and control system. Compliance officers need to help translate regulatory requirements into practical operating standards, controls, workflows, training, escalation rules, and monitoring activities. They should not only advise business units on what a regulation says. They should help determine how that requirement is implemented and evidenced across customer onboarding, payments, lending, deposits, fraud monitoring, vendor management, complaints, and reporting.

A modern compliance function should be able to:

- Interpret laws, rules, and regulatory guidance in business terms

- Define compliance risk materiality standards

- Develop risk assessment methods for products, processes, customers, and geographies

- Set training expectations based on role and risk exposure

- Review whether frontline teams are applying compliance procedures correctly

- Approve higher-risk customers, transactions, products, or exceptions based on risk rules

- Monitor the overall health of the compliance program

- Report control gaps, emerging risks, and remediation status to leadership

This shift does not mean compliance owns every risk alone. The first line still owns day-to-day risk execution, and risk, audit, legal, cybersecurity, and operations all play critical roles. But compliance must have enough visibility and authority to challenge weak practices, escalate issues, and confirm that controls are operating as expected.

A bank’s compliance team should not be seen as a department that says “yes” or “no” at the end of a process. It should be part of the operating system that helps the bank make risk-aware decisions from the beginning.

2. Build a Risk Culture That Supports Escalation and Challenge

Risk-based compliance works only when the bank’s culture supports transparency. If employees are afraid to escalate issues, if business teams treat compliance as a blocker, or if leadership rewards growth without control discipline, the compliance program will eventually fail.

A strong risk culture in banking depends on three behaviors:

- Timely information sharing

- Rapid escalation of emerging risks

- Willingness to challenge unsafe or non-compliant practices

These behaviors are easy to describe but difficult to measure. That is why banks should use structured methods to assess risk culture across business units, branches, teams, and functions. Risk culture surveys, employee feedback, issue trends, audit findings, hotline reports, training results, and control exceptions can all reveal whether risk awareness is actually embedded into daily operations.

Banks should examine questions such as:

- Do employees know how to raise compliance concerns?

- Are issues escalated early or only after they become serious?

- Do managers respond constructively when risks are raised?

- Are employees comfortable challenging questionable practices?

- Do frontline teams understand the bank’s risk appetite?

- Are policy exceptions tracked and reviewed?

- Do repeated issues appear in the same departments or processes?

Risk culture must also be visible at the leadership level. Executives and board committees should review not only compliance metrics, but also patterns that show whether the organization is learning from incidents. A low number of reported issues may not always mean low risk. It may mean employees do not trust the reporting process.

In 2026, banks should treat culture as a control environment issue. The quality of escalation, accountability, and challenge often determines whether a compliance weakness is identified early or becomes an enforcement problem later.

3. Take a Holistic View of GRC Across the Bank

Governance, risk, and compliance in banking cannot be managed through disconnected processes. Yet many financial institutions still rely on separate systems for regulatory obligations, risk assessments, audits, incidents, complaints, policies, vendor reviews, and control testing. Teams often use spreadsheets, shared drives, email threads, and local trackers to manage work that should be connected.

This creates blind spots. A vendor risk issue may not be connected to a control failure. A customer complaint may not be tied to a policy gap. A failed audit test may not trigger a corrective action. A regulatory change may not be mapped to the affected business process. These gaps make it difficult for leadership to understand the bank’s real risk position.

A holistic GRC model helps banks connect:

- Regulations and obligations

- Policies and procedures

- Risks and controls

- Business processes and products

- Vendors and third parties

- Audit findings and issues

- Incidents and corrective actions

- Training and attestations

- Board and management reporting

The Federal Reserve has also emphasized tailoring supervision to each bank’s size, complexity, business model, and risk profile, and its 2025 supervision report notes that supervisors are focusing on material risks to safety and soundness. Banks should apply the same principle internally. The compliance program should be tailored to the institution’s business model and actual risk exposure, not copied from a generic template.

A centralized GRC approach gives banks one operating view of compliance risk. It helps teams understand not only whether a requirement exists, but who owns it, which controls support it, whether evidence exists, and what remediation is pending.

4. Improve Transparency on Residual Risk and Control Effectiveness

A common weakness in traditional compliance programs is that they focus heavily on listing high-risk processes and related controls, but do not always show whether those controls actually reduce risk. This can create a false sense of security.

For example, a bank may have a documented control for customer due diligence, but if the control is not tested, exceptions are not escalated, or evidence is incomplete, the residual risk may still be high. Similarly, a policy may exist for sanctions screening, but if alert handling is delayed or ownership is unclear, the control environment remains weak.

In 2026, banks need better visibility into residual risk. This means understanding the risk that remains after controls are applied. It also means measuring whether controls are designed well, operating consistently, and producing reliable evidence.

Banks should ask:

- Which controls are mapped to each regulatory obligation?

- Are controls preventive, detective, or corrective?

- How often are controls tested?

- What exceptions or failures have been identified?

- Are control owners clearly assigned?

- What evidence proves the control operated?

- What residual risk remains after the control is applied?

- Are remediation actions completed on time?

This is especially important in areas such as AML, KYC, OFAC sanctions, fair lending, consumer complaints, vendor risk, cybersecurity, fraud controls, and payment operations.

A risk-based compliance program should not only say, “We have controls.” It should show which controls are working, which controls are weak, and which risks still need leadership attention.

5. Use Data More Effectively for Compliance Decisions

Banks generate enormous amounts of data across transactions, customer onboarding, monitoring alerts, complaints, audits, policies, investigations, training, vendors, and control testing. But data only supports compliance when it is usable, connected, and trusted.

If compliance data is spread across documents, emails, business systems, spreadsheets, and standalone tools, teams lose time reconciling information instead of interpreting it. This makes it harder to detect patterns, measure effectiveness, and report risk accurately.

A modern banking compliance program should use data to answer practical questions:

- Which compliance tasks are overdue?

- Which business units have repeated control failures?

- Which customers or products create higher compliance exposure?

- Which vendors have unresolved issues?

- Which policies are overdue for review?

- Which training programs have low completion?

- Which audits produce repeat findings?

- Which incidents point to a deeper process gap?

- Which remediation items are past due?

The DOJ and banking regulators have increasingly emphasized the need for compliance programs to have access to relevant data and use it to assess effectiveness. For banks, this means compliance teams need dashboards, alerts, trend reporting, and evidence trails.

Data should support better decisions, not just reporting. The strongest banks use compliance data to prioritize testing, refine training, improve controls, and escalate emerging risks before they become regulatory findings.

6. Integrate Compliance With Risk Management, Audit, Regulatory Affairs, and Issue Management

Risk-based compliance is strongest when compliance is integrated with the broader risk management framework. A bank cannot manage compliance effectively if regulatory obligations, risk assessments, internal controls, audits, issues, and remediation plans are handled separately.

Integration helps banks:

- Maintain a complete view of operational and compliance risks

- Identify systemic issues across business units

- Reduce duplicated work across control functions

- Allocate resources based on risk

- Improve management reporting

- Avoid gaps between compliance, risk, audit, and operations

- Track remediation from finding to closure

A practical integrated model should include:

- One inventory of operational and compliance risks

- Standardized taxonomies for risks, controls, products, processes, and obligations

- Aligned timelines for risk assessment, control testing, remediation, and reporting

- Clear roles between the first line, compliance, risk, legal, audit, and business owners

- Integrated training and communication plans

- Governance forums with defined mandates

- Formal escalation paths for high-risk issues

- Clear ownership for corrective actions and target dates

This matters because many modern compliance risks fall into gray areas. Third-party risk involves procurement, legal, IT, compliance, security, and business owners. Privacy risk involves compliance, legal, data teams, cybersecurity, and operations. AML risk involves customer onboarding, transaction monitoring, investigations, technology, and governance. Without integration, these risks can fall between functions.

7. Strengthen Cross-Functional Collaboration

Bank compliance is no longer the responsibility of one function. A single policy update may affect legal, IT, HR, training, operations, customer service, risk, and audit. A vendor issue may involve procurement, cybersecurity, privacy, compliance, and business owners. A fraud trend may involve frontline teams, investigations, technology, legal, and risk management.

That is why collaboration is not a soft benefit. It is a control requirement.

Greater internal collaboration improves:

- Risk assessments

- Incident response

- Fraud prevention

- Policy review

- Vendor oversight

- Control testing

- Audit response

- Corrective action follow-up

Banks should create workflows that make collaboration structured. For example, when a new policy is created, the platform or process should automatically route it to legal, compliance, risk, business owners, HR, and training teams as needed. Feedback should be captured in one place. Versions should be tracked. Approvals should be documented. Employees should receive the final version and acknowledge it.

Without this structure, collaboration becomes email-based and difficult to audit. That creates version confusion, delayed approvals, and weak evidence.

8. Properly Map Risks to Controls

Risk-to-control mapping is one of the most important parts of risk-based compliance management. Banks often know their risks, but they struggle to map each risk to the right control, owner, evidence, and testing process.

For example:

Risk: Employees handling account details, social security numbers, loan files, or transaction data may access sensitive information beyond what is required for their role.

Relevant controls may include:

- Role-based access controls

- Background checks for sensitive roles

- Segregation of duties

- Dual approval for high-risk transactions

- Access reviews

- Data loss prevention controls

- Security training

- Monitoring of unusual access patterns

- Restrictions on personal devices in sensitive areas

- Incident reporting procedures

The value of mapping is that it shows whether the bank has a sufficient control environment for each material risk. It also helps auditors, regulators, and leadership understand how risk is being managed.

A strong risk-to-control map should include:

- Risk description

- Related regulation or obligation

- Control objective

- Control owner

- Control frequency

- Evidence required

- Testing method

- Last test result

- Open issues

- Residual risk rating

- Corrective action status

This makes compliance measurable and defensible.

9. Use Technology to Support Continuous Compliance

Technology is now essential to banking compliance because the volume and complexity of compliance work cannot be managed effectively through manual processes. Banks must track regulations, controls, policies, audits, issues, third parties, evidence, and reporting across multiple teams and systems.

A GRC platform can help banks:

- Centralize obligations, risks, controls, and policies

- Assign ownership and due dates

- Automate recurring compliance tasks

- Send reminders and escalations

- Track evidence and approvals

- Monitor control testing

- Manage corrective actions

- Support vendor due diligence

- Generate dashboards for leadership

- Maintain audit trails for regulatory reviews

Technology is also important for third-party risk management. Banks need evidence that vendors and service providers are being reviewed, monitored, and held accountable. A platform can help collect SOC reports, contracts, risk assessments, issue logs, renewal dates, due diligence documents, and remediation evidence.

The best technology does not replace compliance judgment. It gives compliance teams better visibility, consistency, and control over execution.

10. Use AI and Machine Learning Carefully

AI and machine learning can improve banking compliance, but they must be governed carefully. Banks are using AI and analytics for fraud detection, transaction monitoring, sanctions screening, regulatory change management, customer risk scoring, alert triage, and document review.

AI can help banks:

- Analyze regulatory updates faster

- Reduce false positives in monitoring systems

- Identify unusual transaction behavior

- Improve fraud detection

- Support customer due diligence reviews

- Find patterns in complaints or incidents

- Automate repetitive reporting tasks

- Reduce manual errors

However, AI creates its own risks. Banks need clear governance for model risk, data quality, explainability, bias, privacy, security, human review, and documentation. In April 2026, the OCC, Federal Reserve, and FDIC issued updated model risk management guidance that emphasizes risk-based, tailored practices based on a bank’s size, complexity, and extent of model use.

Banks should ask:

- Where is AI being used in compliance or risk decisions?

- What data does the model use?

- How are outputs validated?

- Is there human review for high-impact decisions?

- Are models tested for bias and accuracy?

- Are changes documented?

- Are third-party AI tools reviewed?

- Can decisions be explained to auditors or regulators?

AI can strengthen compliance management, but it cannot replace accountability. Banks need strong governance before they scale AI-enabled compliance workflows.

Banks enter 2026 under continued pressure from regulators, auditors, customers, boards, and the wider financial ecosystem. Compliance expectations are no longer limited to having policies in place or responding to findings after an examination. Banks now need to show that risks are identified early, controls are operating effectively, corrective actions are completed on time, and evidence is available when regulators ask for it.

A systematic, risk-based, and technology-enabled approach is now essential. With rising scrutiny around AML, KYC, sanctions, fraud, cybersecurity, AI governance, third-party risk, consumer protection, and operational resilience, banks can no longer rely on spreadsheets, email follow-ups, and disconnected systems to manage compliance. These manual methods create blind spots, slow down response times, and make it harder to prove accountability.

A modern GRC platform helps banks bring compliance, risk management, internal controls, policies, audits, issues, and evidence into one connected system. It allows teams to assign ownership, monitor obligations, track control performance, manage remediation, and provide leadership with real-time visibility into compliance status and residual risk.

For banks looking to strengthen compliance and governance in 2026, VComply provides a structured way to reduce silos, improve accountability, and maintain audit-ready evidence across teams and business units.

Discover VComply, the preferred solution for leading banks! Book your live demo now.

Frequently Asked Questions

1. What is risk-based compliance management in banking?

Risk-based compliance management focuses on identifying, assessing, and prioritizing compliance risks based on their potential impact. It allows banks to allocate resources efficiently and address high-risk areas proactively.

2. Why is risk-based compliance important for banks?

It helps banks manage increasing regulatory complexity, reduce compliance costs, and enhance operational efficiency. By focusing on risk severity, banks can better prevent violations and maintain strong governance.

3. How does GRC integration support banking compliance?

Integrating governance, risk, and compliance (GRC) frameworks provides a unified view of risk exposure, enables consistent reporting, and promotes better decision-making across departments and business units.

4. What role does technology play in modern compliance management?

AI, automation, and analytics streamline compliance workflows, improve data accuracy, and detect anomalies in real time—helping banks reduce manual effort and improve regulatory reporting efficiency.

5. How can banks build a proactive compliance culture?

Encouraging transparency, continuous employee training, and data-driven monitoring helps establish a culture of accountability. Regular audits and open communication further strengthen compliance resilience.

6. How does VComply enhance banking compliance management?

VComply’s no-code GRC platform centralizes compliance operations, automates risk tracking, and provides real-time insights—enabling banks to simplify workflows and achieve stronger regulatory alignment with ease