What are the limitations of internal controls and how to overcome them?

Internal controls in any organization are of paramount importance as they are defined as rules and procedures established by management or those charged with governance to ensure the timely achievement of the organization’s goals, mission, and vision.

In this article, we will dive deep into what internal controls are and the limitations of internal controls so you can be aware of the associated risk factors and position your organization for success.

Key takeaways (TL;DR)

- Learn how internal controls safeguard assets, ensure compliance, and minimize organizational risks.

- Understand common limitations of internal controls and strategies to mitigate them effectively.

- Discover how automation enhances control reliability and reduces human error significantly.

- Explore risk assessment, monitoring, and training as pillars of strong controls.

- Get insights on leveraging technology like VComply to streamline control management.

What Are Internal Controls?

Internal controls refer to the processes, policies, and procedures implemented within an organization to ensure the reliability of financial reporting, safeguard assets, promote operational efficiency, and compliance with laws and regulations. Here are some common types of internal controls:

Internal controls are designed to provide organizations with reasonable assurance about achieving objectives in critical areas like the reliability of financial reporting, operational efficiency, and compliance with applicable laws and regulations. An internal control system is often implemented to prevent or minimize losses.

Internal controls, however, have their limitations. These limits can prevent the policies, procedures, or technical security measures you already have in place from effectively protecting your organization from threats.

Here are some common types of internal controls:

- Segregation of duties

- Authorization and approval

- Physical control

- Reconciliation and review

- Documentation and record keeping

- IT controls

- Risk assessment

- Training

- Code of conduct

- Monitoring and reporting

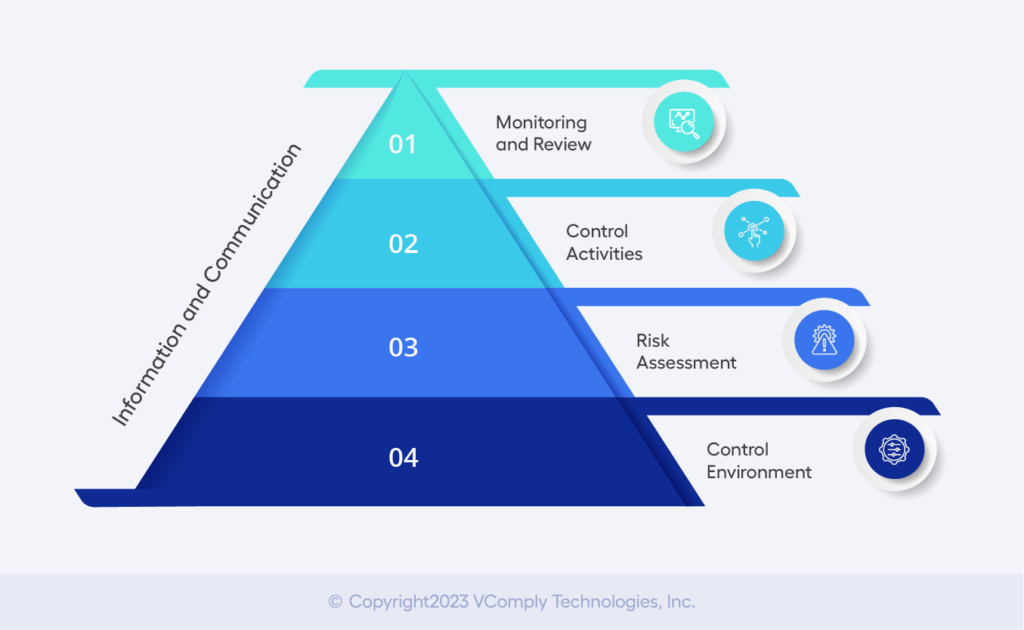

Components of Internal Controls

Internal controls encompass a set of interconnected components designed to safeguard an organization’s assets, ensure the accuracy and reliability of financial information, promote compliance with laws and regulations, and enhance operational efficiency. These components include:

Control Environment: The foundation of internal controls, it sets the tone for the entire organization, emphasizing the importance of integrity, ethical behavior, and a commitment to compliance.

Risk Assessment: The process of identifying and evaluating potential risks that may impact the organization’s objectives and assets. This involves assessing the likelihood and impact of risks.

Control Activities: Specific policies, procedures, and practices put in place to mitigate identified risks. This can include authorization processes, segregation of duties, and access controls.

Information and Communication: Effective communication channels ensure that relevant information is shared within the organization, enabling informed decision-making and the execution of control activities.

Monitoring and Review: Continuous monitoring of control activities to ensure they are functioning as intended and responding to changing circumstances. Regular reviews and audits assess the overall effectiveness of the control system.

These components work together to create a comprehensive internal control framework that helps organizations achieve their objectives while managing risks and maintaining compliance.

Limitations of internal controls and mitigation strategies to overcome them

1. Human error

Ultimately, any decisions that involve human judgment limit the effectiveness of its internal controls. Decision-makers are often under enormous pressure to produce results, which can lead to impulsive or reckless actions. And it is safe to say that people are often the weakest link in cybersecurity and internal control limitation due to human errors is no exception to this rule.

Mitigation strategy

Even the most well-thought-out internal control can fall victim to human error, and for this reason, automation is one way your organization can work to prevent human error from limiting the effectiveness of your internal controls. Rather than relying on manual processes, automated internal controls management uses workflows that automatically test, record data, and report issues. Dashboards can provide clear views of test and control status to eliminate blind spots.

2. Breakdowns

Sometimes even well-designed internal controls fail. Whether employees misinterpret instructions or just make mistakes, mistakes are bound to happen at some point. In general, the effectiveness of your internal controls depends to a large extent on the competence of your employees and those responsible for implementing the related processes. If your employees do not fully understand their roles and responsibilities, or if they do not believe that specific internal controls are necessary, they may not be following established internal control processes.

Mitigation strategy

To prevent internal control mistakes or limitations, we recommend starting a comprehensive policy training program for your employees so that they better understand the why behind internal controls and are more likely to follow the how.

3. Management override

Management override occurs when high-level personnel or privileged user accounts override prescribed policies and procedures for personal benefit, advantage, or convenience. The cancellation of the administration implies some kind of nefarious intent.

For obvious reasons, management override has the potential to completely disrupt your internal control system. If management isn’t following the correct procedures, no one else will. In some extreme cases, organizations even allow their top managers to neglect internal control risks entirely, which in turn almost entirely limits the effectiveness of internal controls.

In such a scenario, in absence of a top-down management approach, employees are more likely to see internal control processes as unnecessary and ignore them.

Mitigation strategy

Automating internal controls can help by providing automated workflows for collecting test data, enforcing test planning, and automating reporting. Using the GRC platform VComply for control management, data is pulled from business applications and stored in a centralized control and risk library with dashboards generated automatically. This dramatically reduces the possibility of voiding or falsifying controls.

4. Collusions

Segregation of duties is effective when the workers involved have properly performed their duties. However, it can be compromised if employees decide to work together to override the system.

For example, instead of reviewing the employee who creates the purchase requisition, the reviewer works with that employee to create purchase requisitions for his personal benefit. This type of fraudulent activity will be difficult to detect since control has been bypassed and subverted. These unnecessary purchases cause the company to lose money and affect its profitability of the company.

Mitigation strategy

Taking a holistic view of your control data gives you the big picture, removing hiding places for fraud or mismanagement. Automating control management involves setting standards, checks, and measuring the actual performance and exercising corrective action, instead of manual control management which is prone to errors.

5. Inadequate training or miscommunication

When the purpose of the control is not adequately communicated to staff or staff are not adequately trained to conduct the control in the first place, it becomes an internal control limitation. The employee may not understand how internal control affects the company as a whole and may neglect it for his own convenience.

A control is ineffective if employees cannot follow and perform it in accordance with internal policy. Again, this exposes your business to risks that could be significantly reduced if the control is performed correctly.

Mitigation strategy

Every employee must be aware of the internal control system in place and their respective importance and the consequence of violating those. A centralized training program must be conducted at regular intervals and management should persuade the employees to go through the training so they take it seriously.

6. Subject to misjudgment

Designing the right control for a business risk requires a great deal of judgment and relevant experience. An internal control process appropriate for another company may not always be appropriate for your organization because no two companies are alike owing to their business nature and overall culture.

Your organization should put effort into identifying risks and controls by conducting risk assessments and regularly evaluating the current internal control system.

Mitigation strategy

Regular risk assessment and objectivity towards internal controls and risk management is the key to navigating the internal control challenge of misjudgment. It can give you a real-time perspective of what’s happening across and remove any human bias.

7. System errors

Even though the internal control system is fully automated, there is a limitation in terms of the internal control system suddenly collapsing or being subject to hacker attacks.

This could result in the loss of important business information and, in more serious cases, a potential loss of customer trust. Therefore, your organization needs to ensure that its automated controls are well-protected and monitored for potential errors and attacks.

Mitigation strategy

Sharing control test results across your organization enables you to take a more proactive, informed, and coordinated approach across your organization. Automating control tests can ensure that tests relevant to a range of business processes are easily accessible and shared across the organization. In addition, ensure you are abiding by all the data protection and security frameworks to minimize the potential threats related to information security.

8. Subject to unforeseen circumstances

The myth that internal controls provide reasonable assurance is an internal control limitation. Sure, they can help your organization prevent, identify, and fix errors and fraud. But there is no surety that the controls will always work.

Mitigation strategy

Internal controls can only be proven effective with routine activities. In case of any new implementation of control procedures or deviation from the normal routine, a regular monitoring process must be put in place to detect any such circumstances and take action immediately.

9. Siloed approach

A siloed approach to internal control risks comprises inefficient or duplicate testing, wasting time and resources, and many more. If different teams manually test the same controls, you cannot streamline your internal control processes, which becomes an internal control system limitation.

Mitigation strategy

You need a holistic, cross-sectional view of risk programs to avoid silos, duplication, and wasted effort. Using a simple, workflow-based approach, your controls can be tested regularly and in a structured manner, with reports covering all elements of your operation.

10. Too many controls

Too much focus on data management or internal controls rather than focusing on the key factors can be a challenge for the organization and a major internal control limitation. Unless you know for sure, which controls would be needed, you need to deep dive and find out rather than going after every internal control available and trying to implement it which might result in severe inefficiency.

Mitigation strategy

Task your process owners with identifying important internal controls and removing non-critical ones. Identify any duplicate controls or those that prioritize low-risk or non-essential controls. Find out if there is potential to harmonize controls that affect multiple regulations.

Automation platforms can help you to gain insights into large amounts of enterprise data and bring order to a variety of actions.

11. Inconsistent controls

Many companies have complex and inconsistent approaches to controlling testing across the organization due to their internal complexities or their laggard approach to handling risk factors. Mergers and acquisitions of companies can also play a key role in the internal control limitation of inconsistent controls as this further complicates the cultural and management aspects.

Mitigation strategy

Creating a single control and risk matrix promotes consistency and allows for simpler, cleaner, and more user-friendly control data. A centralized approach to managing and monitoring internal controls using the compliance management platform VComply can avoid any inefficacy and inconsistency.

12. Technical weakness of internal controls

Technical security controls include both hardware and software. Weaknesses of technical control are due to technological and maintenance changes or configuration errors, becoming internal control limitations.

A good example is the EternalBlue vulnerability in the Windows SMB protocol, discovered in 2017, which exposed existing Windows systems to attacks.

Mitigation strategy

You need to have a state-of-the-art enterprise-grade security compliance management platform that can safeguard your organization from outside vulnerabilities.

13. Weakness in operational internal control

Operational security focuses on the operational monitoring and implementation of risk management in day-to-day business operations. Internal control system limitations in terms of weaknesses in operational controls mostly take place due to human factors. Operational controls become less effective when those responsible for operations do not follow established standards and policies.

Mitigation strategy

First and foremost, all the employees must go through rigorous training to understand the operational security aspects, their importance, and what can be the severity of the internal control processes. You need to keep an eye on the incident response time and always look for avenues to reduce the time taken for effective management using incident management software.

14. Weaknesses in administrative control

Weaknesses in administrative security controls result from persistent non-compliance with established rules and regulations.

An example of administrative control is regular backups of critical systems. In the event of a breach, you can only recover data from the time of the last backup. A backup control is rendered useless and becomes an internal control limitation useless if the organization does not regularly back up data.

Mitigation strategy

Firstly, make sure you have a proper risk assessment in place. Through such assessment, you can identify if there’s any loophole in your present internal control framework or in implementation. Make sure you put the relevant stakeholders on the job and make them accountable for their own actions leading to internal control limitations. There should also be an internal audit at regular intervals to check whether everything is according to the plan or if there’s any deviation from the track.

15. Static Controls

Internal controls must keep pace with a changing risk and regulatory landscape. Static controls which are resistant to change can soon become a liability for organizations. For example, the Sarbanes-Oxley Act of 2002 (SOX) required companies to make significant changes to the way they design and monitor internal controls.

Mitigation strategy

You first need to be aware of the new benchmarks, best practices, and regulations for effective internal controls management solutions. You should be able to modify controls in alignment with changing requirements.

Overcoming Limitations:

Leverage Technology:

Embrace the power of technology, such as automation and data analytics, to enhance the efficiency and effectiveness of internal controls. Automated controls can minimize human errors and ensure consistent compliance.

Continuous Monitoring and Review:

Regularly monitor the effectiveness of internal controls and review them to identify areas for improvement. Perform risk assessments to keep pace with changing threats.

Education and Training:

Invest in comprehensive training programs to educate employees about the importance of internal controls, how to follow procedures, and how to recognize and report suspicious activities.

Segregation of Duties:

Implement and enforce segregation of duties to prevent unauthorized or fraudulent actions. Ensure that no single individual has complete control over a critical process.

Whistleblower Programs:

Establish whistleblower programs to encourage employees to report unethical behavior without fear of retaliation. These programs can help identify and address control weaknesses.

Make VComply an integral part of your internal control system.

Developing, implementing, and maintaining organization-wide internal controls can be a daunting task, and it is common to see organizations struggle with that. Whether you need to manage cyber risks, meet business goals, or meet regulatory requirements, a compliance management platform like VComply can help simplify these tasks and streamline your efforts.

VComply takes the guesswork out of risk management. You can quickly review your internal controls to determine if they are working properly, allowing you to manage your risks by uncovering vulnerabilities before they are exploited. You can use it to:

- Automate the assignment, delegation, review, notification, and assessment of organizational control effectiveness

- Use the control workspace to collaborate with other participants, related files, evidence, or evidence

- Benefit from the library of pre-packaged compliance and control frameworks and regulations

Conclusion

Internal controls though are extremely effective in managing and containing the risk factors and threats to the organization, each control processes certain strengths and weaknesses. You need to identify the internal control limitations and have the proper mitigation strategy in place so it doesn’t blow out of proportion.