Reduce Control Risk: A Practical Playbook for Compliance and Audit Readiness

Internal control failures rarely begin with a single breakdown. They emerge gradually when control ownership becomes unclear, evidence remains scattered across systems, and testing occurs inconsistently across departments. When auditors review these environments, small operational gaps often translate into expanded audit scope and additional control validation.

U.S. regulatory frameworks increasingly emphasize demonstrable control execution rather than documented policy intent. Auditors expect organizations to show structured evidence, consistent monitoring, and timely remediation of control failures. When that evidence cannot be produced quickly, the risk is assumed to be higher.

For compliance leaders, risk managers, and governance executives, the challenge is operational rather than theoretical. Reducing control risk requires disciplined processes that connect risk identification, control ownership, testing, and remediation into a repeatable system.

Key Takeaways

- Control risk directly drives audit scope, regulatory scrutiny, and compliance costs.

- Weak ownership, manual processes, and inconsistent testing are the leading causes of control failure.

- Structured risk-to-control mapping and disciplined testing reduce unexpected audit findings.

- Proactive monitoring and timely remediation lower residual risk across departments.

- Measurable control KPIs strengthen governance oversight and executive confidence.

What is Control Risk?

Control risk is the possibility that internal controls fail to prevent or detect errors, fraud, or compliance violations in a timely manner. Even well-designed policies can break down during daily operations, allowing small gaps to escalate into material misstatements or regulatory findings.

In the United States, regulators and auditors expect proof that controls operate consistently, not just that they exist on paper. If you cannot demonstrate regular testing, monitoring, and remediation, auditors assume higher control risk. That assumption increases audit scope, documentation requests, and scrutiny across the organization.

Control risk typically increases when:

- The control ownership or accountability is unclear.

- Testing is inconsistent or lacks documented evidence.

- Manual processes rely on email chains or spreadsheets.

- Policy updates are not reflected in control procedures.

Unlike inherent risk, which stems from the nature of your industry, control risk is within your influence. Strengthening execution, visibility, and oversight directly reduces the likelihood that operational failures become audit issues.

Control Risk vs. Inherent and Detection Risk

To manage risk effectively, you need to understand how control risk differs from inherent and detection risk. Together, these three components form the audit risk model used across US regulatory environments to determine the level of audit testing required.

- Inherent risk reflects the natural exposure associated with your industry, operations, or transaction complexity. For example, financial institutions face higher inherent risk due to transaction volume and regulatory oversight, while healthcare organizations face risk due to sensitive patient data and privacy requirements.

- Control risk reflects how effectively internal controls reduce that exposure. When reviews, approvals, or reconciliations operate inconsistently, control risk rises.

- Detection risk is the likelihood that auditors fail to identify existing issues. When control risk is high, auditors reduce detection risk by increasing sample sizes and testing procedures.

You cannot eliminate inherent risk, but you can strengthen controls to reduce control risk. When controls operate reliably, auditors gain confidence in your environment and often reduce the depth and disruption of testing.

Also Read: Risk Management 101, Principles, Techniques, and Key Components (2025 Edition)

Common Causes and Examples of Control Risk

Control risk rarely stems from dramatic failures. It usually grows from routine operational gaps that go unnoticed for months. When controls exist only on paper or operate inconsistently, you create exposure that auditors eventually uncover.

In US regulatory environments, documentation and consistency matter as much as intent. Even if your team performs the right activities, a lack of evidence or standardized procedures increases control risk. Regulators expect proof that controls work the same way every time.

Common causes of control risk include:

- Unclear ownership of key controls, leading to missed reviews or approvals

- Manual processes that rely on spreadsheets or email threads

- Infrequent or undocumented control testing

- Segregation of duties conflicts in finance or procurement systems

- Delayed remediation of previously identified control gaps

- Policy updates that do not translate into updated procedures

For example, if your quarterly access reviews are inconsistent or lack documented sign-off, auditors may classify that control as ineffective. If reconciliations are completed but supporting documentation is scattered across shared drives, you struggle to demonstrate reliability.

Assessing control risk requires more than confirming that policies exist. You need to evaluate whether your controls operate consistently and produce reliable, audit-ready evidence. In US regulatory environments, execution and documentation carry equal weight.

Also Read: 5 Steps to Building an Effective Risk Management Program in Your Organization

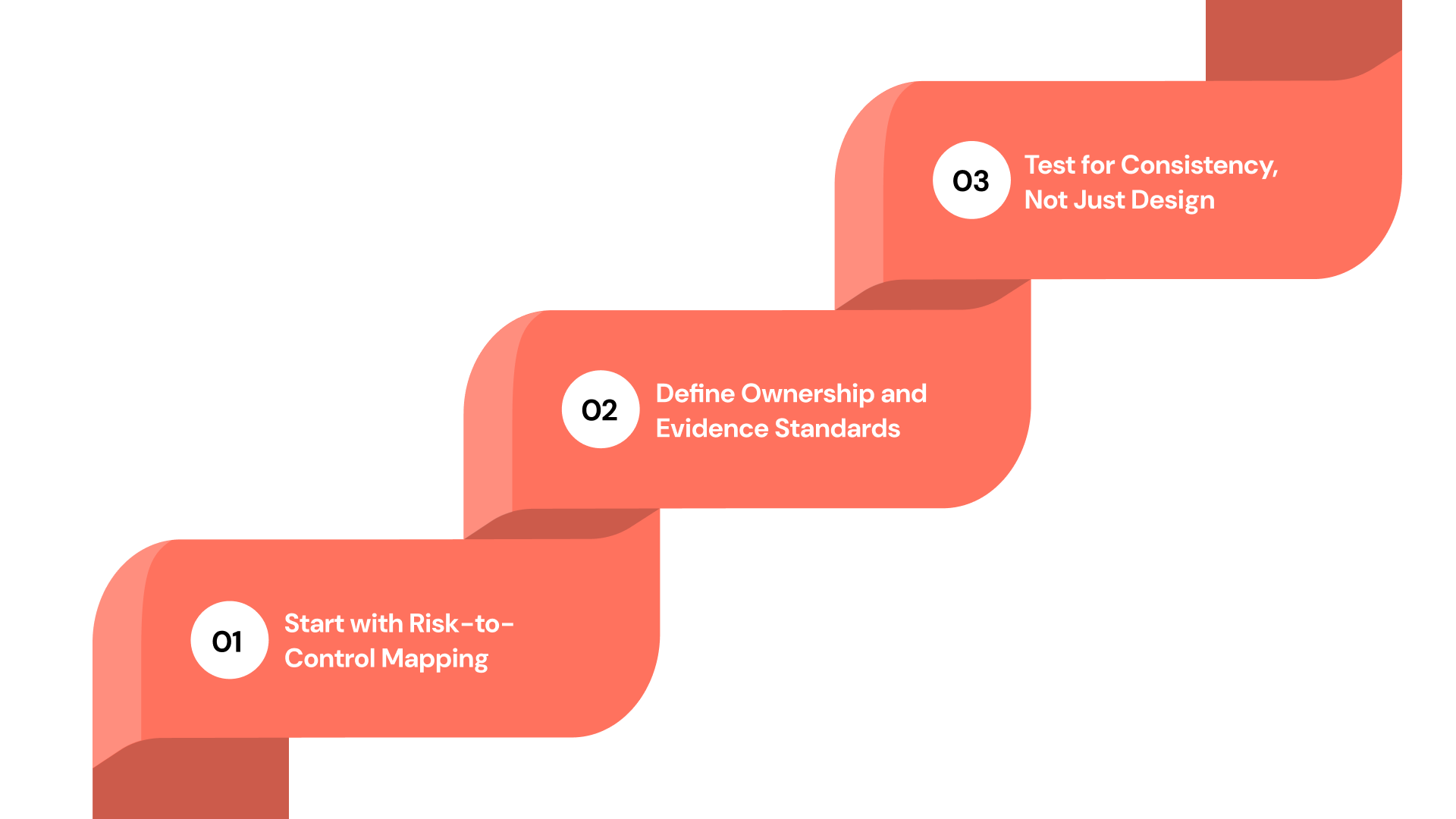

How to Assess Control Risk: 3 Essential Steps

A structured assessment gives you clarity before auditors begin testing. When you follow a repeatable approach, you reduce surprises, strengthen accountability, and identify weaknesses early.

1. Start with Risk-to-Control Mapping

Begin by identifying the risks that could affect financial reporting, regulatory compliance, or operational integrity. Then confirm that each risk has a clearly defined control designed to reduce it.

Many organizations document this relationship in a Risk and Control Matrix. This framework connects risks, controls, owners, and testing procedures in one place. It creates visibility and removes confusion during audits.

2. Define Ownership and Evidence Standards

Controls fail most often because ownership is unclear or documentation standards are inconsistent. Each control should have a named owner and a defined execution frequency.

You should also specify what qualifies as acceptable evidence. Screenshots, system logs, approvals, or reconciliations must be stored consistently and retrievable on demand.

3. Test for Consistency, Not Just Design

A control may look strong on paper but fail in practice. You need to test whether it operates as intended over time.

A practical assessment process includes:

- Verifying that controls operate at the required frequency

- Reviewing a sample of completed control activities

- Confirming evidence meets documented standards

- Tracking remediation timelines for identified gaps

Repeated failures, delayed remediation, or inconsistent documentation signal elevated control risk. When you monitor these trends proactively, you reduce audit friction and strengthen governance oversight.

A Six-Step Operating Model for Reducing Control Risk

Reducing control risk requires a structured operating model that connects risk management with daily execution. Without defined testing, monitoring, and reporting, your controls weaken over time. A disciplined framework helps you reduce audit surprises and improve oversight.

Below is a practical six-step approach you can implement across departments.

Step 1: Map objectives → risks → controls (owner, frequency, evidence type)

- Link strategic objectives to documented risks, then assign specific controls with named owners, execution frequency, and defined evidence standards. Many teams document this structure within a centralized system such as ComplianceOps to maintain visibility.

- Expected outcome: clearer accountability, fewer missed controls, and stronger audit traceability.

Step 2: Define control tests and SLAs

- Establish how each control will be tested, how often testing occurs, and service-level timelines for addressing exceptions.

- Expected outcome: consistent validation of control performance and reduced repeat findings.

Step 3: Automate evidence collection and continuous monitoring

- Use workflow-driven tracking to automate reminders, capture evidence centrally, and monitor control status in real time. For example, ComplianceOps dashboards provide visibility into overdue tasks and testing gaps.

- Expected outcome: reduced manual effort, fewer documentation gaps, and faster evidence retrieval during audits.

Step 4: Self-testing and pre-audit packaging

- Conduct internal control reviews before external audits and generate structured evidence packages for high-risk areas.

- Expected outcome: reduced audit hours, fewer last-minute requests, and improved auditor confidence.

Step 5: Remediate failures and track closure

- Log control failures as structured cases, assign corrective actions, and monitor remediation deadlines.

- Expected outcome: faster remediation cycles and lower residual risk.

Step 6: Attestations and reporting to auditors and leadership

- Require periodic control attestations from owners and generate real-time reports for auditors and executive leadership.

- Expected outcome: improved transparency, stronger governance oversight, and greater executive confidence.

KPIs That Indicate Reduced Control Risk

You cannot reduce control risk without measuring performance. Clear metrics help you identify weaknesses before they escalate into audit findings.

Track these indicators to evaluate control effectiveness:

- Percentage of controls tested on schedule

- Average time to remediate failed controls

- Percentage of automated versus manual controls

- Audit hours spent validating controls

- Rate of repeat control failures

Improvement in these metrics signals stronger execution and lower residual risk. Over time, consistent performance reduces audit disruption and strengthens executive confidence.

Industry-Specific Control Risk Considerations

Control risk does not look the same in every industry. Regulatory expectations and operational complexity shape where your greatest exposure exists.

1. Financial Services

Segregation of duties and transaction monitoring controls must operate consistently under strict regulatory scrutiny. Even minor documentation gaps can trigger audit findings or regulatory concerns.

2. Healthcare

Access controls and privacy safeguards require regular reviews and documented attestations. Regulators expect clear evidence that Protected Health Information (PHI) remains secure at all times.

3. Manufacturing and Energy

Operational safety and environmental controls must connect with incident tracking and corrective action workflows. Delays in remediation increase both compliance exposure and operational risk.

Regardless of your industry, the core requirement remains the same. You must demonstrate consistent execution, documented oversight, and timely remediation to keep control risk low.

Take Control of Control Risk with Continuous Oversight

Manual tracking leaves gaps that auditors eventually uncover. Disconnected systems make it difficult to prove that controls operate consistently across departments. As regulatory pressure increases, reactive documentation is no longer enough.

You need centralized visibility, automated workflows, and measurable accountability.

Sustaining reliable control execution requires more than periodic reviews. Organizations need systems that connect risks, controls, testing, and remediation into a single operational structure.

Platforms designed for governance operations help bring that structure into daily practice. Within the VComply GRCOps Suite, modules such as ComplianceOps, RiskOps, and CaseOps allow organizations to manage controls, testing cycles, and remediation workflows in a coordinated environment rather than across disconnected tools.

Explore how ComplianceOps structures continuous control oversight and audit readiness across the enterprise. Book a free demo today.

Conclusion

Control risk increases when execution is inconsistent, ownership is unclear, and documentation is fragmented across systems. In regulated U.S. environments, these gaps do not stay isolated, they surface during audits as expanded scope, repeated findings, higher remediation costs, and operational disruption.

What high-performing teams do differently is treat control management as an ongoing system, not a periodic exercise. Controls are clearly owned, testing is structured, evidence is continuously maintained, and remediation is tracked to closure. This creates a stable compliance posture where audit readiness is maintained, not assembled under pressure.

VComply supports this by bringing control, ownership, testing, evidence, and remediation into a single operational framework, so teams can maintain consistency, visibility, and accountability across the enterprise.

Start a 21-day free trial to see how you can operationalize control risk management and sustain audit readiness across your organization.

FAQs

Control risk is the possibility that a company’s internal controls fail to prevent or detect material errors or compliance violations. Auditors assess control risk to determine how much additional testing is needed.

Inherent risk arises from the nature of a business or industry. Control risk depends on how effectively your internal controls reduce that exposure.

Control risk cannot be eliminated entirely, but it can be reduced through consistent execution and monitoring. Strong testing and documentation lower the likelihood of control failures.

Auditors use control risk to determine the scope and depth of their testing. Higher control risk usually leads to more sample testing and documentation requests.

You measure control risk by evaluating control effectiveness, testing frequency, failure rates, and remediation timelines. Trends in repeat issues or delayed corrections indicate elevated risk.

Manual processes, unclear ownership, inconsistent testing, and poor documentation commonly increase control risk. Delayed remediation of known issues also raises exposure.