Is PCI Compliance Required by Law? What Businesses Must Know in 2026

Every day, businesses process card payments without realizing that gaps in their security practices can expose customer data. These failures rarely come from negligence. They usually happen because PCI requirements are misunderstood or inconsistently applied.

When that happens, the impact is real: lost trust, financial penalties, and even the inability to accept card payments.

Many compliance teams are still unclear on a basic question: Is PCI compliance a legal requirement in the U.S., or a contractual obligation tied to payment processors? This uncertainty makes it harder to protect cardholder data and manage risk with confidence.

In this blog, we break down what PCI compliance includes, when PCI compliance required by law applies, who must comply, and how to approach compliance step by step.

Key Takeaways

- PCI compliance applies to all businesses handling cardholder data, no matter the size.

- Not federally mandated, but non-compliance can lead to fines, lawsuits, and lost payment privileges.

- Compliance requires technical controls, policies, monitoring, and audit-ready evidence.

- Merchant levels (1–4) dictate validation type: SAQs, RoCs, AOCs, and scans.

- VComply centralizes compliance, risk, policy, and incident management for easier audits and continuous monitoring.

Did you know?

According to recent reporting, a major U.S. cyberattack compromised sensitive personal data for at least 25 million Americans, including those in Texas. This illustrates how pervasive and impactful data breaches can be when security protections fail. Such incidents highlight why strong card-data security (under PCI DSS) matters to every business that touches payment card information.

PCI Compliance Explained: What It Really Means

PCI DSS sets a global baseline of security expectations for any business that stores, processes, or transmits payment card data, ensuring controls to safeguard customers and reduce fraud. It represents actionable steps to protect cardholder information through structured requirements rather than vague recommendations.

Below are key components that define what PCI compliance really means in operational terms:

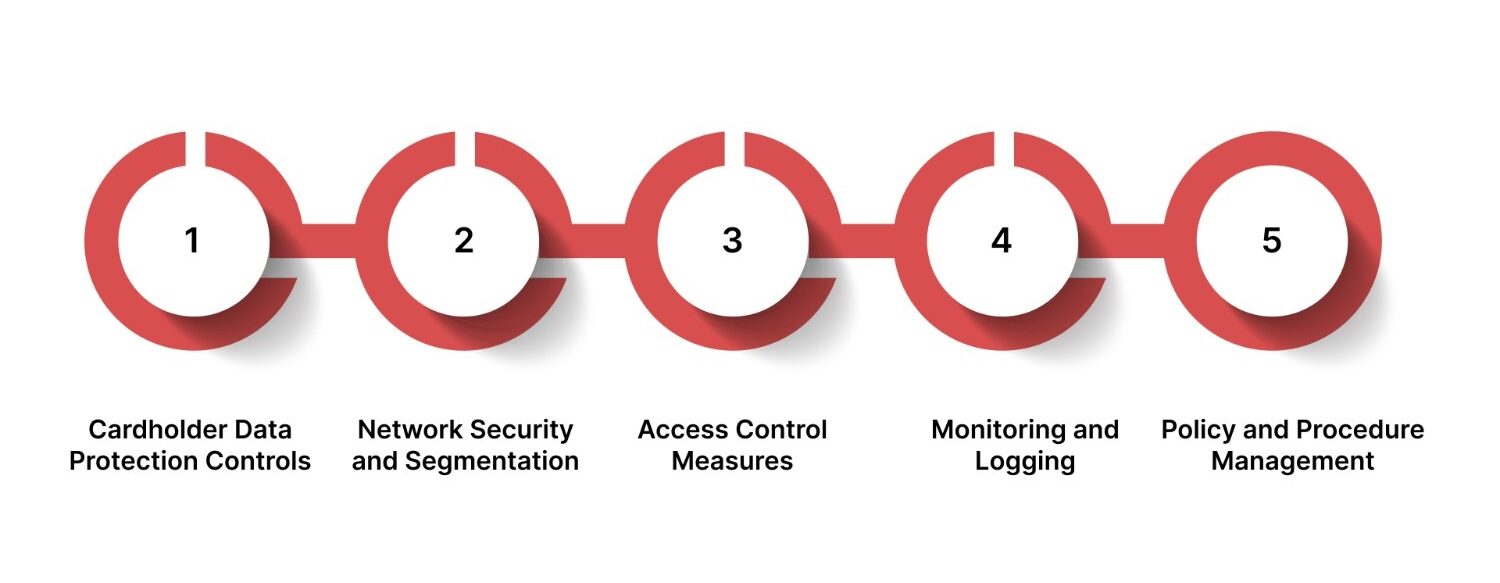

- Cardholder Data Protection Controls: Standards require strong encryption and secure storage of cardholder data so that unauthorized parties cannot read or misuse sensitive information.

- Network Security and Segmentation: PCI DSS mandates firewalls and secure configurations to isolate systems handling card data from other network segments, reducing exposure to attacks.

- Access Control Measures: Only authorized personnel should access cardholder systems, using unique user IDs and multifactor authentication to prevent unauthorized usage.

- Continuous Monitoring and Logging: Organizations must track, centralize, and review access logs regularly to detect anomalies and respond quickly to threats.

- Ongoing Policy and Procedure Management: PCI compliance requires documented security policies and regular updates to operational processes to maintain alignment with changing threats.

Also Read: Understanding the Cost of PCI Compliance

While PCI DSS sets clear security standards for protecting cardholder data, many businesses still wonder if PCI compliance is required by law, and understanding the legal context is key to shaping a defensible compliance strategy.

Is PCI Compliance Required by Law? The Answer for U.S. Businesses

In the United States, PCI compliance is not codified as a federal law that forces every business to comply simply by statute. This means no federal agency will prosecute you for lacking PCI DSS on its own. However, PCI is far from optional in practice.

PCI DSS is enforced through contracts with payment brands and banks, and in some states, parts of it are backed by law, making compliance effectively mandatory.

Below are the key aspects of PCI DSS’s legal and contractual standing in the U.S.

Legal Status of PCI DSS in the U.S.:

- Not a Federal Law: PCI DSS is a security standard developed by the PCI Security Standards Council (a consortium of major card brands), not a statute enacted by Congress. It has no direct enforcement by federal regulators.

- Contractual Enforcement: Your acquiring bank or payment processor requires PCI compliance as part of the merchant agreement. Failure to comply can lead to contractual penalties, loss of card processing privileges, or increased fees, all of which carry real business and legal risk.

- State Legal References: Some states explicitly reference PCI DSS in statute. For example, Nevada is the first state to require PCI DSS compliance and provides liability protection for compliant businesses after a data breach.

Consequences Tied to Legal Exposure:

- Fines Passed Through Contracts: Acquiring banks and card brands can impose significant fines on non‑compliant merchants, often ranging from $5,000 to $100,000 per month until compliance is achieved.

- Civil Liability in Breach Events: If a data breach occurs and your business is not PCI compliant, you may face lawsuits from customers, financial institutions, or partners, strengthened by the fact that you failed to follow recognized data security practices.

- Operational and Regulatory Impact: Beyond PCI contracts, state privacy laws like the California Consumer Privacy Act (CCPA) can increase legal exposure for breaches of personal data, which often include cardholder details.

Now that you understand when PCI compliance required by law applies, let’s look at who needs to be PCI compliant and why.

Who Needs to Be PCI Compliant and Why?

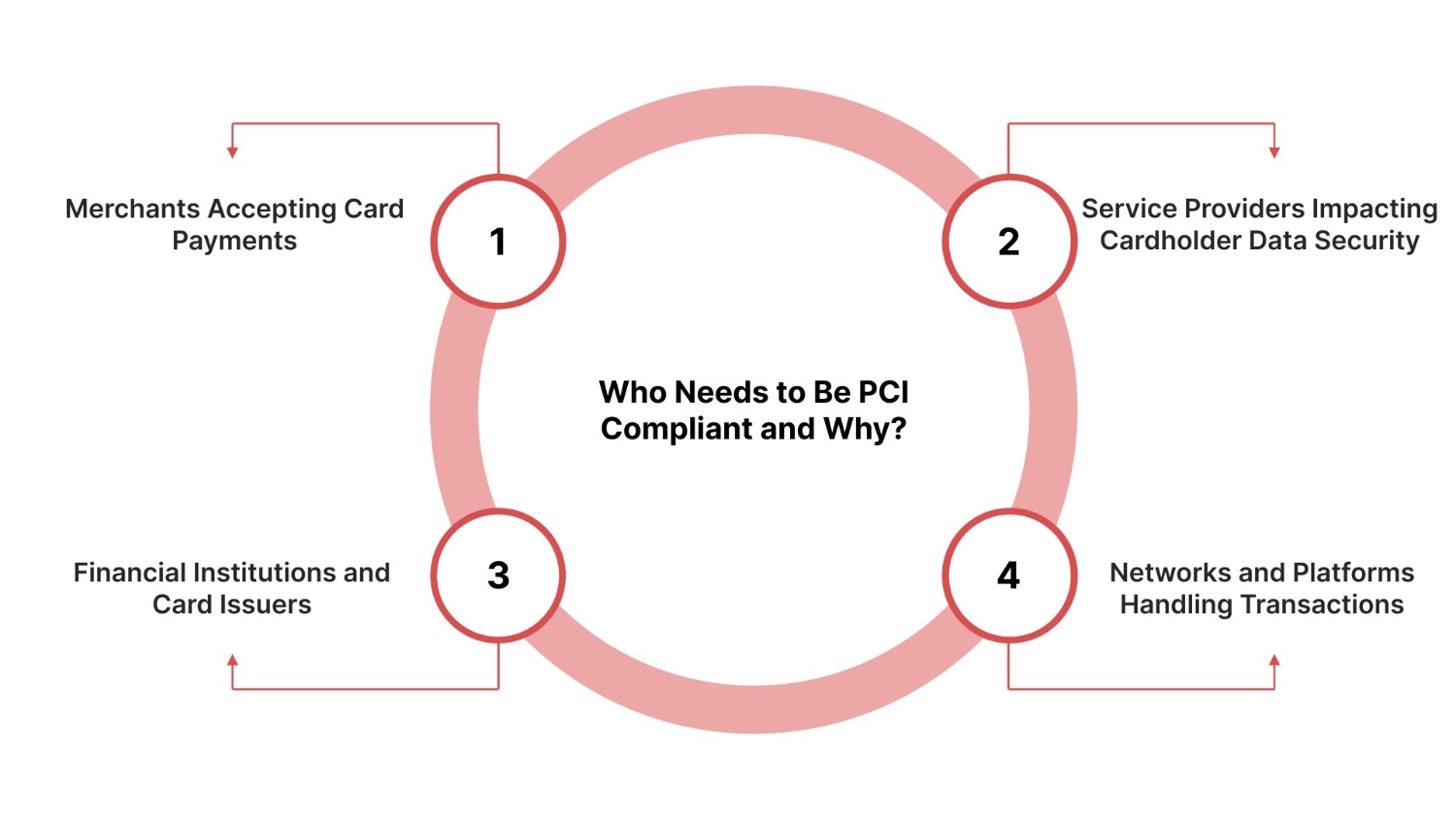

PCI DSS applies to any organization that stores, processes, or transmits payment card data, regardless of size or transaction volume, and extends to service providers that could impact the security of that data.

Below are the principal categories that fall under PCI compliance obligations:

- Merchants Accepting Card Payments: All businesses that accept credit or debit card payments, whether in‑store, online, or via mobile channels, must meet PCI DSS requirements because they handle cardholder data as part of their revenue operations.

- Service Providers Impacting Cardholder Data Security: Third‑party services such as payment gateways, processors, hosting providers, and related infrastructure vendors are in scope because their systems directly influence how card data is protected.

- Financial Institutions and Card Issuers: Banks, credit unions, and card issuers that manage account and transaction data are subject to PCI DSS controls due to their role in processing and safeguarding sensitive payment information.

- Networks and Platforms Handling Transactions: Subscription systems, SaaS platforms, and e‑commerce applications that transmit or store cardholder data must comply, even if the data passes through APIs or third‑party services.

Also Read: PCI DSS Compliance Made Simple: Key Requirements and Core Standards

Once you know who must comply, the next step is understanding what compliance entails, covering both policies and technical controls, so you can fully address the requirements and obligations tied to PCI compliance required by law.

What Compliance Involves: From Policies to Technical Controls

PCI compliance requires both documented governance and strong technical safeguards to protect cardholder data and reduce the likelihood of breaches across your organization.

Below are the key aspects that compliance entails and how they work together to secure your systems:

- Network Security Controls: Implement and maintain firewalls and secure configurations to control traffic into and out of systems that process or store cardholder data. These controls prevent unauthorized access to your payment environment.

- Data Encryption and Protection: Encrypt stored cardholder data and secure its transmission across networks to ensure sensitive information is unreadable without proper authorization, limiting exposure if systems are compromised.

- Access Control Measures: Restrict access to cardholder data to only those personnel with a legitimate business need, using unique IDs, multi‑factor authentication, and role‑based permissions.

- Vulnerability Management and Patch Processes: Maintain up‑to‑date systems by applying security patches promptly, conducting regular vulnerability scans, and establishing a program to address identified weaknesses.

- Security Policies and Procedures: Develop and maintain documented policies outlining how your organization protects cardholder data in accordance with PCI DSS, including roles, responsibilities, and employee training requirements.

VComply’s Compliance Ops helps centralize all your technical controls, policies, and monitoring activities in one place, reducing the risk of missed requirements and easing audit preparation. Streamline your PCI DSS compliance workflows and ensure your team always has the right evidence at hand.

With policies and controls in place, the next step is showing evidence of compliance, a key part of understanding PCI compliance required by law.

How Do Validation Levels and Required Evidence Demonstrate Compliance?

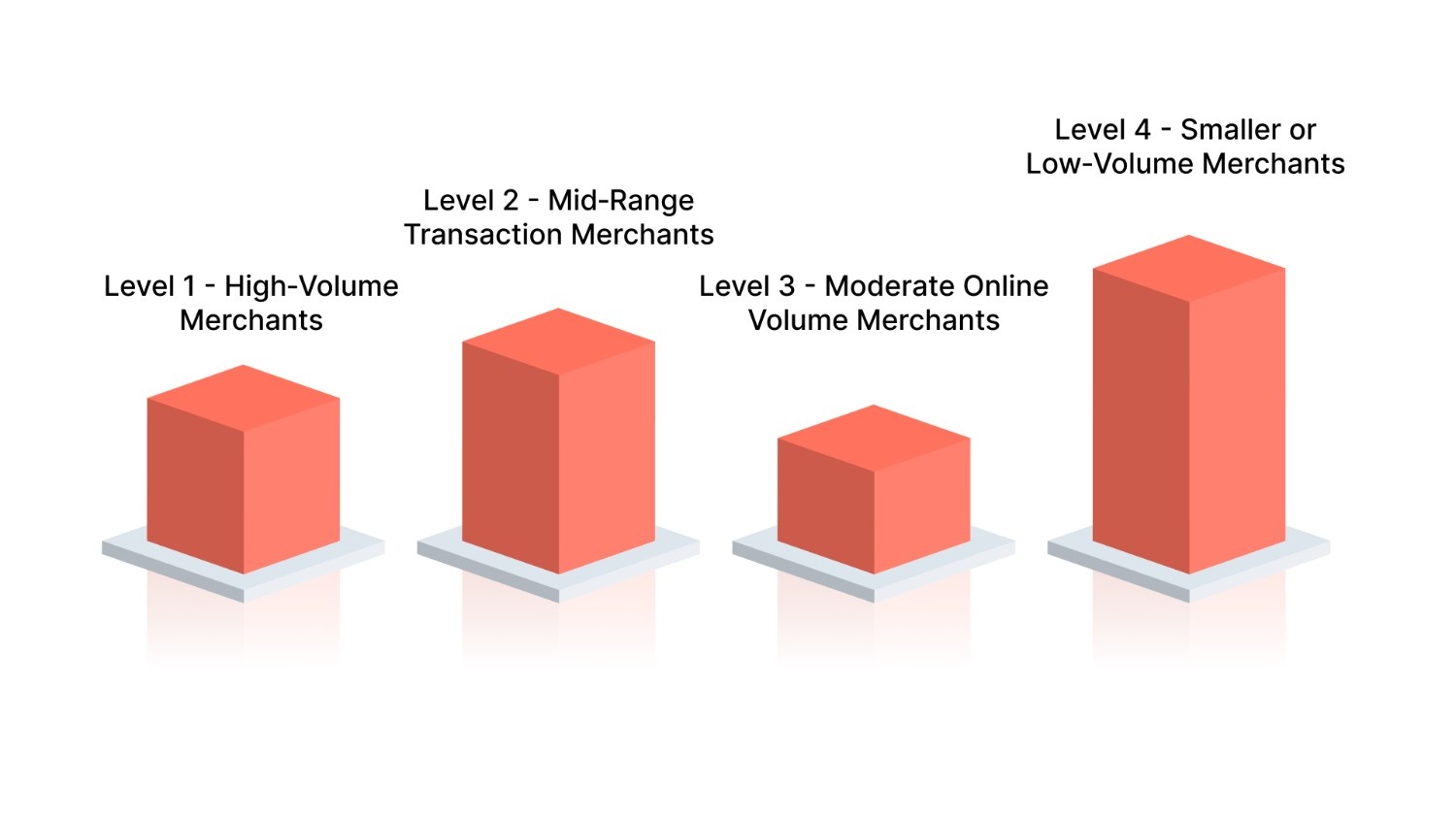

To demonstrate PCI compliance, your business must provide specific validation evidence based on its merchant level, which is determined by annual card transaction volume.

Below are the four merchant levels and the types of evidence typically required to satisfy PCI DSS validation:

- Level 1 – High‑Volume Merchants: Merchants processing more than 6 million transactions annually fall into Level 1. This level requires the most stringent validation:

- An annual Report on Compliance (RoC) conducted by a Qualified Security Assessor (QSA) or an Internal Security Assessor (ISA).

- Annual Attestation of Compliance (AOC) signed by the assessor.

- Quarterly external vulnerability scans by an Approved Scanning Vendor (ASV). Level 1 examples include large e‑commerce platforms and national retail chains.

- Level 2 – Mid‑Range Transaction Merchants: Merchants with 1 million to 6 million transactions per year typically use:

- An annual Self‑Assessment Questionnaire (SAQ) is appropriate to their environment.

- Quarterly network scans by an ASV.

- Attestation of Compliance (AOC) to verify self‑evaluation results.

Many regional retailers fall into this category.

- Level 3 – Moderate Online Volume Merchants: Merchants processing between 20,000 and 1 million e‑commerce transactions per year:

- Annual SAQ submission.

- Quarterly scans by an ASV are generally required.

- An AOC to confirm self‑reported results. Many online stores with moderate annual sales are Level 3.

- Level 4 – Smaller or Low‑Volume Merchants: Merchants processing fewer than 20,000 e‑commerce transactions or up to 1 million overall may:

- Complete an annual SAQ.

- Perform quarterly ASV scans if required by the acquirer. The exact requirements for Level 4 are often set by your acquiring bank or payment brand.

Types of Required Evidence:

- Self‑Assessment Questionnaire (SAQ): A series of structured yes/no questions where you attest your controls meet PCI DSS requirements.

- Report on Compliance (RoC): A formal, on‑site audit by a QSA; used primarily by Level 1 merchants.

- Attestation of Compliance (AOC): A signed declaration of your compliance status accompanying SAQ or RoC submissions.

- Quarterly Vulnerability Scans: External scans by an ASV to validate network security and identify vulnerabilities.

Also Read: Key Differences Between PCI DSS and HIPAA Compliance

Understanding the validation levels and required evidence helps clarify compliance expectations and addresses common questions about whether PCI compliance is required by law.

Common PCI Compliance Myths Debunked

Even experienced teams often misunderstand PCI DSS, leading to weak controls, audit issues, or unnecessary costs. Below are three common myths and the realities behind them.

- Myth 1: Only Large Businesses Must Comply: PCI DSS applies to any organization that processes, stores, or transmits cardholder data, regardless of size. Small businesses are often at higher risk due to weaker security controls.

- Myth 2: Compliance is a One-Time Effort: PCI compliance is ongoing. It requires continuous monitoring, regular assessments, and updates as systems and threats change.

- Myth 3: Compliance Eliminates Legal Liability: PCI compliance reduces risk and shows due diligence, but it does not prevent fines, contractual penalties, or legal action after a breach.

With VComply’s GRCOps Suite, you gain end-to-end visibility over compliance, risk, policy, and incidents. This integration allows leadership to track progress, ensure accountability across teams, and maintain continuous monitoring, making PCI compliance a sustainable, organization-wide practice rather than a one-off effort.

Now, let’s have a look at the PCI compliance checklist for your business.

Step‑by‑Step PCI Compliance Checklist for Your Business

To achieve and demonstrate PCI compliance, you must follow a structured set of steps that help you identify, secure, monitor, and document all aspects of your cardholder data environment.

Below is a practical checklist tailored for U.S. businesses that process payment cards:

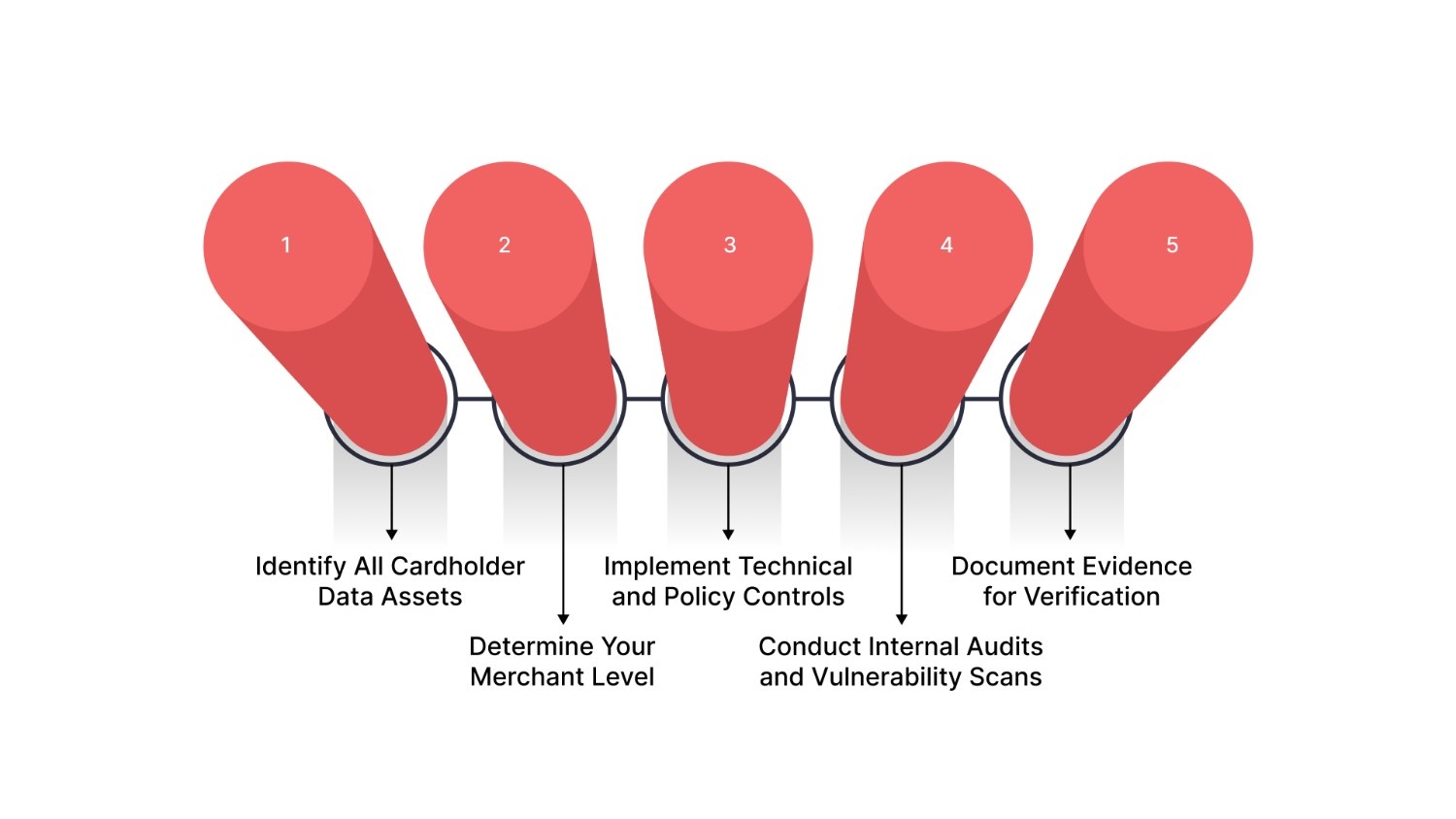

- Identify All Cardholder Data Assets: Map every system, database, application, or process that stores, processes, or transmits cardholder data to define the scope of your compliance activities. This should include internal systems and any third‑party services that touch payment data.

- Determine Your Merchant Level: Review your annual card transaction volume to confirm whether you are a Level 1, Level 2, Level 3, or Level 4 merchant, as this influences your validation method (e.g., SAQ or ROC) and reporting requirements.

- Implement Technical and Policy Controls: Based on PCI DSS requirements, deploy network security controls (firewalls, segmentation), configure systems securely, protect stored and transmitted cardholder data, and restrict access based on business need‑to‑know.

- Conduct Internal Audits and Vulnerability Scans: Perform regular risk assessments, internal audits, and external vulnerability scans (at least quarterly by an Approved Scanning Vendor) to identify gaps and remediate them promptly.

- Document Evidence for Verification: Retain required documentation such as SAQ or ROC reports, Attestations of Compliance, risk assessments, network diagrams, access logs, and scan results. This evidence supports your compliance status during validation or audit reviews.

Also Read: PCI DSS Compliance and Assistance in Financial Services

By following these structured steps, you’re building a resilient compliance program that enhances security and supports audit readiness.

How VComply Simplifies PCI Compliance for Businesses

When ensuring PCI compliance, with its technical controls, audits, policy obligations, and risk monitoring, you need a centralized solution that reduces complexity, eliminates manual processes, and gives you real‑time visibility into your compliance status.

VComply is a cloud‑based Governance, Risk, and Compliance (GRC) platform that brings all compliance, risk, policy, and incident management workflows into one unified environment, helping businesses like yours simplify PCI compliance and stay audit‑ready without juggling spreadsheets or disconnected tools.

Below is how VComply can help you streamline and operationalize PCI compliance effectively:

- ComplianceOps – Centralized Compliance Management: ComplianceOps enables you to define PCI DSS controls, track compliance activities, assign tasks, and centralize evidence in a single platform. This reduces manual oversight and ensures your team can stay audit‑ready at all times with automated workflows and status tracking.

- RiskOps – Integrated Risk Identification and Monitoring: RiskOps gives real‑time transparency into risk data associated with your payment card environment. It helps you identify, assess, and prioritize risks that could impact PCI controls, with dashboards and heatmaps that make it easy to understand exposure and drive proactive mitigation.

- PolicyOps – Streamlined Policy Lifecycle Management: With PolicyOps, you can create, approve, distribute, and track PCI‑related policies and procedures within a centralized repository. Automated workflows ensure policies remain current, employees acknowledge them, and audit evidence is easily accessible.

- CaseOps – Incident and Remediation Tracking: CaseOps helps you log, investigate, and resolve PCI‑related incidents or control failures. By centralizing incident records and corrective actions, you gain accountability, reduce resolution time, and maintain compliance evidence for auditors.

- Unified GRCOps Suite for End‑to‑End Visibility: VComply’s GRCOps suite connects all four operational pillars, compliance, risk, policy, and case management, offering leadership a comprehensive, real‑time view of your GRC posture. It enables collaboration across teams, drives accountability, and supports continuous monitoring rather than one‑off assessments.

Book a demo with VComply to see how ComplianceOps, RiskOps, PolicyOps, and CaseOps can streamline your PCI compliance workflows and keep your organization audit‑ready with confidence.

Final Thoughts

PCI DSS compliance is a foundational component of securing payment ecosystems for businesses of all sizes that accept, process, or transmit cardholder data. The standards you implement today help protect sensitive financial information, reduce fraud risk, and avoid costly financial and reputational fallout from breaches or non‑compliance.

VComply helps you transform PCI compliance from manual spreadsheets and scattered evidence into a strategic, automated, and scalable program. With VComply’s integrated GRC suite, you can define PCI DSS controls, coordinate risk assessments, enforce policy adherence, and track remediation activities, all from a single platform.

Ready to turn PCI compliance into a competitive advantage rather than a burden? Start your 21‑day free trial with VComply today and experience how ComplianceOps can streamline your compliance operations and keep your business audit‑ready with confidence.

FAQs

Yes. PCI DSS covers all environments where cardholder data is processed, transmitted, or stored, including phone and mail orders. Businesses must implement appropriate security controls, such as encrypted storage, restricted access, and monitoring, even if physical or remote channels are the only methods used for payments.

Yes. Clients, partners, or payment processors can contractually demand stricter compliance than your merchant level indicates. Even if your transaction volume qualifies for a lower validation level, you must meet the additional requirements, which may include more extensive SAQs, audits, or quarterly scans.

Not always. If multiple locations share the same Cardholder Data Environment (CDE) under one legal entity, a single validation usually suffices. However, acquiring banks or card brands may still require individual location scans or reporting to ensure consistent compliance across all sites.

Yes. PCI DSS applies to any organization that processes, transmits, or accepts cardholder data, not just those storing it. Even if data is temporarily processed or transmitted via systems you control, controls like encryption, access restrictions, and monitoring are required to maintain compliance.

You should provide evidence such as your Self-Assessment Questionnaire (SAQ), Attestation of Compliance (AOC), quarterly vulnerability scan reports, and internal audit records. These documents demonstrate that PCI DSS controls are in place and functioning, satisfying client, bank, or payment processor validation requirements.