Internal Audit Checklist: Avoiding Gaps That Trigger Audit Failures

Audit season often brings a flood of follow-up requests, scattered documents, and incomplete evidence. The risk is not the audit itself, but discovering too late that a control gap was missed. For compliance leaders, internal audits are high-stakes. They must surface and explain control weaknesses before regulators or executives do.

And it turns out this anxiety is backed by research: in a study of firms’ internal control systems, more than half (54.6%) reported at least one material internal control weakness affecting operations or compliance, even before mandated audits began.

That’s why a structured internal audit checklist is essential. In this blog, we explain what an internal audit checklist should include, how to prepare and execute one, common mistakes to avoid, what auditors look for, and practical examples to help you audit with confidence.

Key Takeaways

- A structured checklist ensures controls, risk, and compliance gaps are addressed consistently.

- Proper pre-audit preparation improves efficiency and accuracy.

- Following the 5-step audit process delivers reliable, actionable results.

- Avoiding scope, compliance documentation, and follow-up mistakes strengthens audit outcomes.

- VComply streamlines audits, integrates all GRCOps, and enhances visibility.

Did you know?

In 2024, U.S. regulators found audit deficiencies in 39% of inspected audits. This means more than a third of audits had quality issues that could reflect control or process weaknesses if not addressed through strong internal audit oversight. This highlights why systematic internal audit processes, like a structured internal audit checklist, are essential for catching control weaknesses early and preventing costly deficiencies.

What Is an Internal Audit and Why Does It Matter

Internal audit is a systematic and independent evaluation of an organization’s internal controls, processes, and governance to ensure operations are effective, compliant, and aligned with strategic objectives. It offers assurance to leadership that risk management and controls operate as intended, beyond routine management oversight.

Below are the key aspects that explain its importance for your compliance, risk, and executive goals:

- Systematic Evaluation of Controls: Reviews whether policies, procedures, and controls effectively prevent errors, fraud, or regulatory non‑compliance before issues escalate.

- Strengthening Governance Frameworks: Helps ensure organizational governance aligns with strategic objectives and regulatory expectations.

- Enhanced Regulatory Compliance and Controls: Internal auditing systematically evaluates controls and compliance processes, reducing the likelihood of violations of laws (e.g., SOX, HIPAA) and identifying areas where compliance processes require strengthening.

- Improved Risk Management Assurance: By assessing risk management activities and enterprise risk management frameworks, internal auditors help confirm risks are identified, assessed, and managed in alignment with organizational strategy and risk appetite, increasing confidence in overall risk posture.

- Objective Assurance for Leadership and Governance: The audit function offers independent insight into governance and controls, enabling boards and executives to make informed strategic decisions and strengthen corporate governance frameworks.

Understanding these benefits also highlights why internal audits differ from external audits, and how both complement each other to strengthen governance and oversight.

Internal Audit vs External Audit: Key Differences

Below is a concise comparison to help you understand how internal audits differ from external audits, both vital but distinct functions in strong governance, risk, and compliance frameworks:

| Aspect | Internal Audit | External Audit |

| Primary Purpose | Evaluates and improves internal controls, risk management, compliance, and operational effectiveness. | Provides an independent opinion on the accuracy and fairness of financial statements and compliance with statutory requirements. |

| Who Conducts It | Internal auditors, either in‑house staff or contracted specialists, report to the management/audit committee. | Independent third‑party auditors or audit firms external to the organization. |

| Scope | Broad, can include finance, operations, IT, compliance, risk, and governance processes. | Narrow, typically focused on financial records and reporting standards compliance. |

| Reporting Audience | Senior management and the board (audit committee). | Shareholders, regulators, lenders, and external stakeholders. |

| Frequency | Ongoing or periodic throughout the year, based on risk priorities. | Usually, annual or as required by law. |

| Mandate | Generally voluntary and tailored to organizational needs. | Often statutory and mandatory, especially for publicly traded companies. |

Also Read: Internal Controls Process Mapping for U.S. Regulations

With a clear distinction between internal and external audits, you can now focus on building an internal audit checklist that ensures your processes are thoroughly evaluated and compliant.

How to Create an Effective Internal Audit Checklist

An internal audit checklist gives your audit team a clear framework to verify controls, assess processes, and ensure compliance systematically. It prevents ad‑hoc reviews and ensures every high‑risk area is addressed with consistency throughout the audit cycle.

Below are the core sections that should be part of an effective internal audit checklist:

- Audit Objectives and Scope Definition: Establish clear objectives and scope for the audit, specifying what areas (e.g., finance, IT, operations) and standards (e.g., SOC 2, ISO/IEC 27001) the audit will cover. This focus ensures that your checklist targets the areas that matter most to your risk and compliance priorities.

- Governance and Policy Alignment: Review governance frameworks, board reporting lines, and policy approvals to confirm that corporate governance structures align with strategic goals and regulatory expectations. Strong governance evaluation ensures leadership oversight effectiveness.

- Risk Assessment and Prioritization: Include items that assess whether risks are identified, quantified, and prioritized appropriately, and whether high‑impact risks are reflected in the audit scope to ensure your audit addresses critical control gaps.

- Control and Process Evaluation: Check the existence and operational effectiveness of internal controls, process procedures, and workflow standards across departments to validate whether processes are both designed and functioning as intended.

- Evidence and Documentation Verification: Ensure the checklist includes prompts for evidence gathering and compliance documentation review, including policy manuals, process records, test results, and audit trails, so your audit records are comprehensive and defensible.

VComply’s Compliance Ops centralizes policies, automates audit checklists, and tracks compliance adherence in real time. This helps your team avoid missed controls and gaps before they become risks. Streamline policy management and ensure every department aligns with your compliance standards.

Once the structure of your checklist is defined, it helps to include practical sample items that auditors can use to verify controls, compliance, and operational integrity.

Sample Checklist Items

Below are practical and actionable internal audit checklist questions that experienced auditors use to verify control effectiveness, compliance, and operational integrity.

These items help ensure your internal audit evaluation is thorough, structured, and defensible:

- Policy and Procedure Currency: Confirm that all relevant policies and procedures have been reviewed, updated, and formally approved within the last 12 months to reflect current regulatory requirements and internal standards.

- Access Rights and Permissions Validation: Verify that access permissions across key systems (e.g., financial systems, sensitive data repositories) are aligned with documented IT security policies and that revoked access has been removed in a timely manner.

- Incident and Exception Log Review: Ensure all incident logs, exceptions, and corrective action records have been reviewed, closed, and that documented follow‑up actions with responsible owners have been identified.

- Control Operation and Effectiveness Testing: Test whether internal controls (e.g., segregation of duties, transaction authorizations) function as designed and whether exceptions are documented with risk impact.

- Documentation and Evidence Completeness: Check that evidence supporting compliance assertions (e.g., signed control test sheets, audit trails) is complete, legible, and stored securely for future audit review or regulatory inspection.

Now, let’s have a look at the 5-step internal audit process that ensures your checklist delivers actionable, reliable results.

5‑Step Internal Audit Process

A structured internal audit process ensures your audit activities are disciplined, repeatable, and aligned with business risk priorities. The following five steps reflect common professional practice used by audit functions to systematically plan, execute, and conclude audit work.

Below are the core steps and what each entails:

- Step 1 – Audit Planning and Scope Definition: Establish the audit’s objectives, scope, and standards to guide your efforts, including which processes, control areas, and risk factors will be reviewed. Clear planning is essential for targeted evaluation and resource alignment.

- Step 2 – Evidence Collection and Review: Gather relevant policies, records, logs, and documentation that support your audit focus areas. Auditors analyze documents and examine workflows to understand current practices and prepare for control testing.

- Step 3 – Control Testing and Evaluation: Evaluate whether internal controls are designed correctly and operating effectively by testing selected controls and transactions. This step may involve review, sampling, or observation techniques to validate control performance.

- Step 4 – Reporting Findings and Gaps: Document the observations, issues, and exceptions identified during testing. Create an audit report that includes findings, their impact, and actionable recommendations for a remediation plan.

- Step 5 – Follow‑Up and Remediation Tracking: After the report is issued, ensure that corrective actions are assigned, implemented, and tracked. Periodic follow‑up confirms that identified gaps are closed and that control improvements are sustained.

VComply’s Risk Ops enables audit teams to assess and prioritize organizational risks systematically, linking audit findings directly to enterprise risk frameworks. Identify high-impact control gaps faster and make risk-informed decisions with confidence.

Even with a structured process, common mistakes can undermine audit effectiveness. Knowing them helps you avoid pitfalls and strengthen outcomes.

Common Internal Audit Mistakes and How to Avoid Them

Even seasoned audit teams encounter common pitfalls that undermine audit effectiveness and delay meaningful insights. Recognizing these missteps early helps you structure your internal audit process to be more resilient, efficient, and compliant.

Below are frequent errors audit professionals encounter, along with how to mitigate them:

- Unclear Audit Scope and Objectives: Failing to define the audit’s scope and goals clearly can lead to missed key areas and unfocused testing, reducing the audit’s value. Precise scope and SMART objectives help ensure your audit covers all pertinent risk and compliance domains.

- Incomplete or Inconsistent Documentation: Inadequate documentation, whether evidence, procedures, or findings, leads to inefficiencies, misunderstandings, and reporting delays. Ensure documentation is complete, standardized, and recorded promptly.

- Overlooking Risk‑Based Prioritization: Auditing without a risk‑based focus often wastes resources on low‑impact areas while ignoring emerging or high‑impact threats. Adopt a risk‑based audit approach to align efforts with organizational risk appetite and priorities.

- Insufficient Follow‑Up and Remediation Tracking: Identifying gaps without tracking their resolution can lead to recurring control weaknesses and compliance failures. Implement a structured follow‑up process, linking audit findings to corrective and preventive actions.

Also Read: Manufacturing Compliance Checklist: Complete 2026 Guide

Preventing these mistakes also relies on understanding the key roles and responsibilities auditors play throughout the internal audit lifecycle.

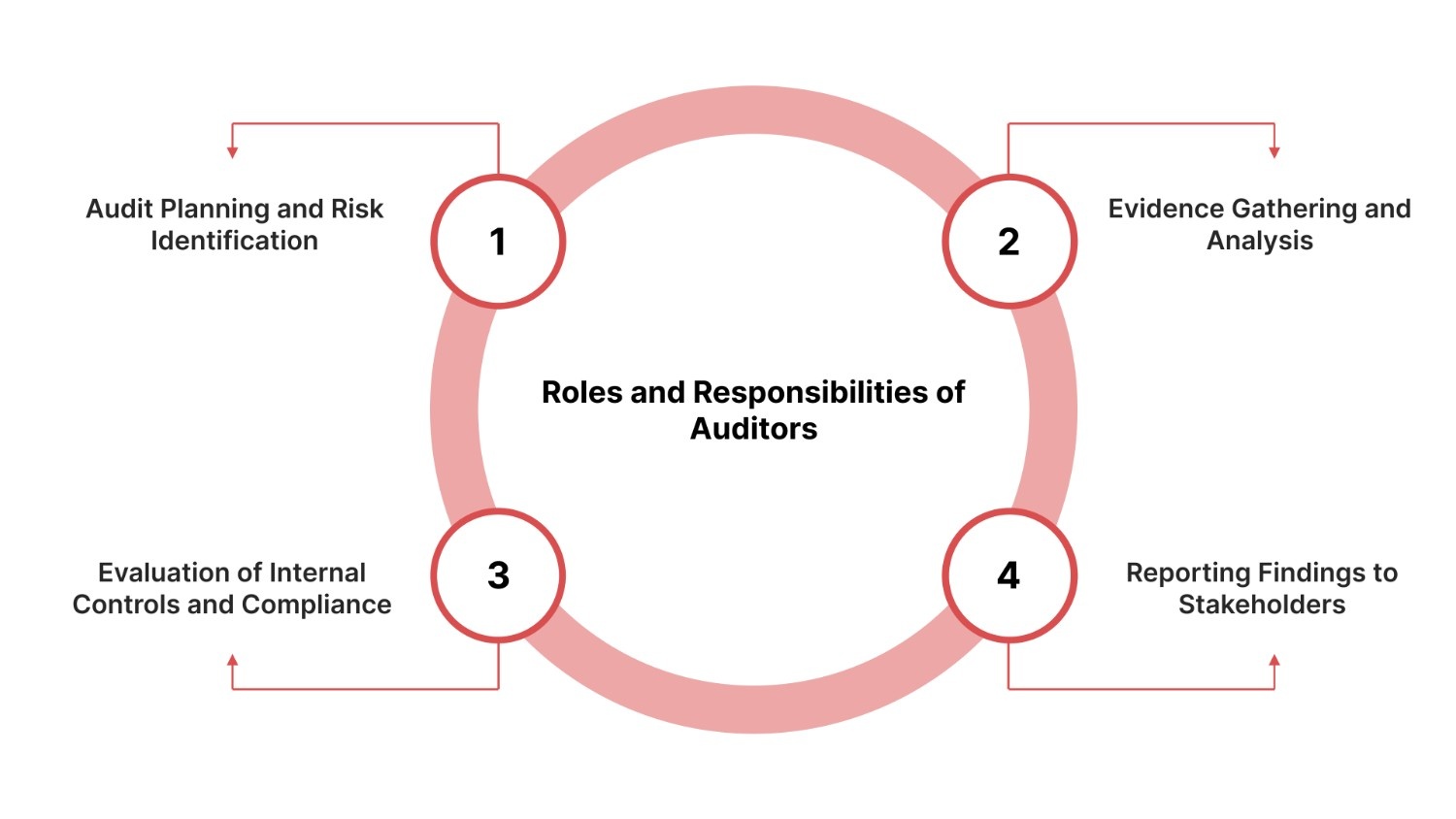

Roles and Responsibilities of Auditors

Internal auditors play a central role in strengthening governance, compliance, and operational integrity across an organization. Their responsibilities extend beyond simple checklist reviews; they combine analytical insight with structured evaluation to help leadership identify risks, validate controls, and drive continuous improvement.

Below are the key roles auditors typically perform in the internal audit process:

- Audit Planning and Risk Identification: Auditors establish the audit plan by defining objectives, prioritizing risk areas, and determining the audit scope based on regulatory requirements and strategic risk assessments.

- Evidence Gathering and Analysis: They systematically collect and examine documentation, transaction records, logs, and workflows to gain a clear understanding of current practices and identify deviations from standards.

- Evaluation of Internal Controls and Compliance: Auditors test whether controls are designed correctly and operating effectively, and they assess organizational adherence to internal policies and external regulations.

- Reporting Findings to Stakeholders: After fieldwork, auditors prepare detailed reports that communicate audit results, highlight deficiencies, and outline the impact of control gaps for management and the audit committee.

VComply’s GRCOps Suite connects ComplianceOps, RiskOps, PolicyOps, and CaseOps in a single platform, giving you a unified view of all audit, risk, and compliance activities. Reduce siloed processes, improve visibility, and ensure audit readiness across your organization effortlessly.

Also Read: How to Map U.S. Regulations to Internal Controls, A Comprehensive Guide and Checklist for 2026

These responsibilities make internal auditors indispensable partners in risk management and governance, helping organizations stay resilient and compliant in a complex regulatory environment.

How VComply Can Simplify Your Internal Audit

When you face the intricacies of internal audits, from planning scopes and gathering evidence to tracking findings and reporting, you need more than spreadsheets and manual checklists.

VComply is an all‑in‑one Governance, Risk, and Compliance (GRC) platform that unifies compliance, audit, risk, policy, and incident management in a single system, giving you clarity, accountability, and audit readiness without siloed tools.

Below is how VComply can help make your internal audit process more efficient, accurate, and reliable:

- Automated Checklist Templates and AuditOps: VComply offers customizable internal audit checklist templates and task workflows that mirror your audit process, allowing you to automate audit planning, scheduling, evidence gathering, and fieldwork execution, eliminating repetitive manual setup and reducing error risk.

- Real‑Time Dashboards and Centralized Reporting: With centralized dashboards, you can view audit statuses, key findings, compliance performance metrics, and risk heatmaps in real time, enabling data‑driven decisions and faster response to control gaps without toggling between systems.

- Task Assignment and Collaboration Features: Assign audit responsibilities, set due dates, send automated reminders, and track task completion across teams with intuitive task management, helping compliance officers and audit teams stay aligned and accountable.

- Unified GRCOps Capabilities: Through integration of ComplianceOps, RiskOps, PolicyOps, and CaseOps, VComply lets you connect audit findings with risk assessments, policy controls, and incident resolution in one platform, enhancing visibility and reducing control gaps across your entire compliance and risk ecosystem.

- Centralized Evidence and Documentation Management: Store audit evidence, workpapers, policies, and risk records in a secure, centralized repository, so you can demonstrate compliance with regulators and internal stakeholders confidently and without misplaced documents.

Ready to streamline your internal audits with an integrated GRC platform? Book a demo with VComply to see how the platform can transform your audit process.

Final Thoughts

Internal audits are strategic assurance tools that help you safeguard assets, improve processes, and strengthen corporate governance. By systematically evaluating controls, risk management, and operational effectiveness, your internal audit function becomes a foundation for proactive decision‑making and sustained organizational resilience.

That’s where VComply transforms your audit process. With its integrated GRC platform, VComply centralizes checklist templates, task assignments, evidence management, and real‑time dashboards, so you can manage internal audits with clarity and confidence.

If you’re ready to enhance control quality, streamline audit execution, and reduce operational burdens, start your 21‑day free trial on VComply today, and experience how structured GRC automation elevates internal audit success.

FAQs

Internal auditors follow the International Professional Practices Framework (IPPF) and professional standards to ensure consistent, high-quality audit practices. These standards define ethical principles, risk-based approaches, and reporting expectations, helping auditors maintain objectivity and credibility.

Departments are selected based on risk assessments, considering operational complexity, regulatory requirements, and past audit findings. High-risk functions like finance, IT, or compliance-heavy operations are prioritized. This ensures resources are focused on areas where control gaps could impact business continuity or regulatory adherence.

Internal audits can focus on financial, operational, IT, compliance, or integrated areas. Financial audits review transaction accuracy, operational audits assess process efficiency, IT audits check system controls, and compliance audits ensure regulatory adherence. Integrated audits combine multiple areas for a holistic organizational risk perspective.

Frequency depends on risk exposure and regulatory requirements. High-risk processes may require quarterly or semi-annual reviews, while stable low-risk areas may be audited annually. A risk-based schedule ensures critical controls are continuously monitored, and audit resources are allocated efficiently.

Clarify which departments, processes, or systems are included, the timeframe of review, applicable regulations, and standards. Asking about scope prevents misaligned expectations, ensures relevant evidence is collected, and confirms the audit addresses both high-risk areas and organizational compliance objectives effectively.