Insurance Brokers & Agencies Compliance Requirements Guide

Compliance in insurance brokerage isn’t governed by a single rulebook; it’s a complex web of obligations that differ by state, product, and client type. At its core, it ensures brokers act fairly, protect consumers, and adhere to legal and ethical standards. Brokers face requirements from multiple authorities, including state insurance departments for licensing and advertising, the NAIC for model laws, and federal regulations like AML and data privacy laws, particularly for financial data. Compliance touches both front-office and back-office functions, from client communications and data storage to commission disclosures and agent training. Essentially, it’s an ongoing process that’s woven into the daily operations of the business.

In 2025, the U.S. insurance brokers and agencies industry is valued at $234.8 billion, having grown at a steady CAGR of 1.5% since 2020. As the market expands, so does regulatory oversight. State regulators and the NAIC are intensifying enforcement across critical areas like licensing, consumer disclosures, data privacy, and anti-money laundering (AML) compliance. Updated model laws, more frequent audits, and stricter documentation expectations are becoming the norm.

Failing to meet these standards doesn’t just risk penalties. It can lead to license suspensions, reputational damage, or even legal consequences. Whether you’re a solo broker or part of a national agency, compliance isn’t a checkbox. It is critical to protecting your business and earning client trust.

Key Takeaways (TL;DR)

In this article, we’ll break down the key compliance requirements brokers and agencies need to stay on top of in 2025 and how to manage them effectively.

- Compliance in insurance brokerages is a continuous, multi-layered responsibility shaped by state, federal, and carrier-specific regulations.

- Licensing management, data privacy, suitability reviews, and complaint handling are high-risk areas that require active oversight and clear documentation.

- Failure to standardize disclosures, track continuing education, or control marketing materials can lead to regulatory violations and legal exposure.

- Technology plays a critical role in reducing manual errors, enforcing compliance workflows, and maintaining audit-ready records across distributed teams.

- Building a culture of compliance is essential for maintaining trust, avoiding enforcement action, and operating sustainably at scale.

Understanding Compliance for Insurance Brokers and Agencies

Compliance in the insurance brokerage space is not defined by a single regulation or rulebook. It is a layered system of obligations that vary by state, product, and client type. At its core, compliance ensures that brokers operate fairly, protect consumer interests, and meet the legal and ethical standards required to sell insurance.

Unlike insurers, brokers and agencies must navigate requirements from multiple authorities:

- State insurance departments regulate licensing, renewals, and advertising practices.

- The NAIC (National Association of Insurance Commissioners) sets model laws and guidelines many states adopt or adapt.

- Federal regulations such as AML rules and data privacy laws add additional layers of responsibility, especially when dealing with financial data or multi-state operations.

What makes compliance complex for brokers is that it affects both front-office and back-office functions. This includes how you communicate with prospects, store client data, manage commission disclosures, and ensure your agents are properly trained and supervised.

In short, compliance is not a one-time task. It is a continuous process built into everyday operations.

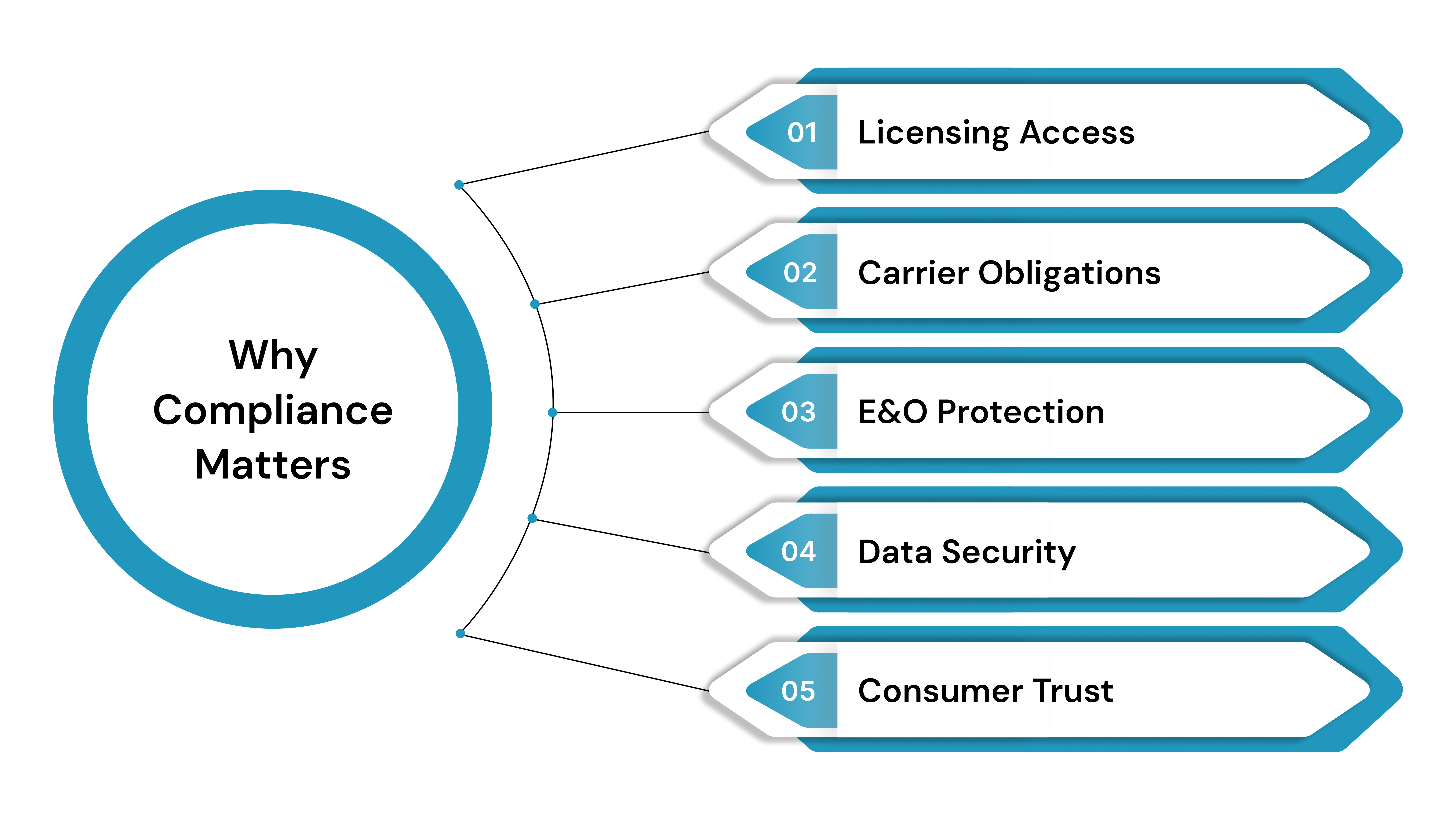

Why Compliance Matters for Insurance Brokers and Agencies

Compliance directly affects your ability to operate, grow, and retain client trust. For insurance brokers and agencies, the stakes are especially high because they sit at the intersection of financial services, personal data handling, and regulated sales practices.

1. Licensing and Market Access

Each U.S. state has its own licensing authority, renewal schedules, and continuing education requirements. Noncompliance, even in one jurisdiction, can result in revoked authority to sell policies, fines, or disciplinary actions. For agencies operating across multiple states, managing this patchwork requires meticulous tracking.

2. Carrier Contractual Obligations

Brokers must often comply not only with regulatory expectations but also with the contractual compliance standards set by insurance carriers. These include production thresholds, disclosure rules, and adherence to underwriting guidelines. Falling short can lead to termination of carrier appointments or commission clawbacks.

3. Protection Against E&O Claims

Errors and omissions (E&O) insurance claims often arise from failure to disclose terms, lapses in communication, or unsuitable policy recommendations. A robust compliance framework, including documented disclosures, policy comparisons, and customer acknowledgments, serves as critical defense evidence in the event of litigation.

4. Data Privacy and Cybersecurity Risk

Brokers routinely collect and store personal health information (PHI), financial data, and Social Security numbers. Compliance with laws such as GLBA, HIPAA (in health insurance), and state-level cybersecurity regulations such as New York’s 23 NYCRR 500 is vital to avoid breaches and the reputational fallout that follows.

5. Consumer Protection and Trust

Transparency in commission structures, full disclosure of product limitations, and proper documentation of client interactions are not just regulatory requirements. They also build long-term trust. Clients expect their brokers to act in their best interest, and a strong compliance culture supports that expectation.

Also read: Improve Risk Visibility and Demonstrate Insurance Compliance Now!

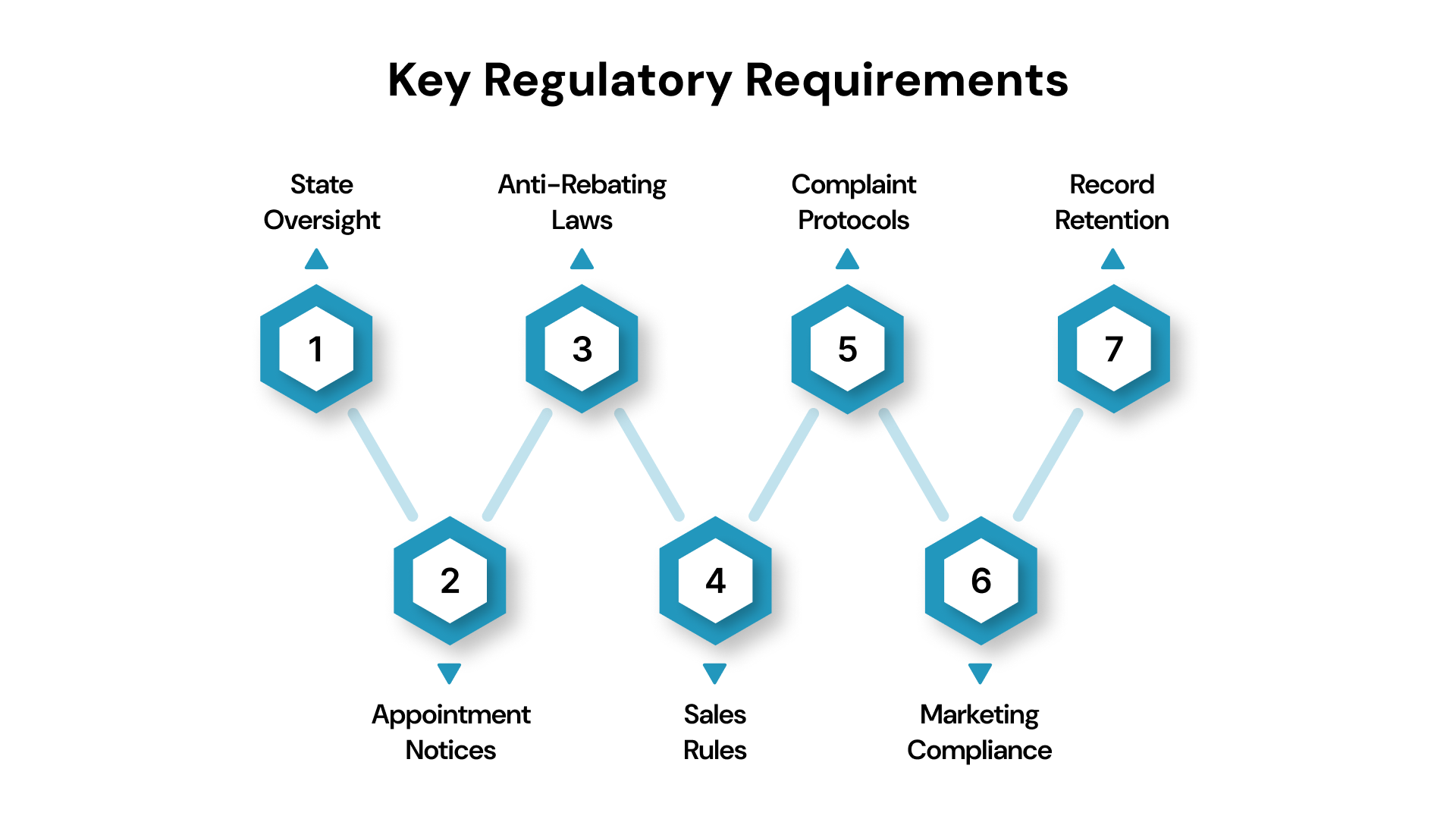

Key Regulatory Requirements for Insurance Brokers and Agencies

Insurance brokers and agencies are subject to a multi-layered regulatory framework that spans federal mandates, state-specific rules, and industry best practices. These requirements are not static; they evolve with market dynamics, consumer protection concerns, and technological advances.

1. State Insurance Department Oversight

Each state has its own Department of Insurance (DOI) that oversees broker and agency conduct. Compliance includes not only initial licensing but also adherence to continuing education mandates, ethical sales practices, and timely license renewals. Agencies with producers in multiple states must ensure all license data is current and correctly filed.

2. Appointment and Termination Notifications

Insurance carriers are required to formally appoint producers to sell on their behalf. Equally important is prompt termination reporting, especially when an agent leaves an agency or engages in misconduct. Failing to file these updates within state-mandated windows can lead to compliance violations for both the agency and the carrier.

3. Anti-Rebating and Anti-Inducement Laws

Most states prohibit the offering of anything beyond the policy terms as an incentive for purchase. Brokers must tread carefully when using giveaways, referral programs, or bundling offers to ensure they do not breach rebating laws. Clear documentation and legal review of marketing campaigns help stay within legal bounds.

4. Suitability and Sales Practice Rules

Brokers selling annuities or life insurance are often required to perform suitability assessments before issuing policies. This includes gathering financial information, assessing long-term objectives, and ensuring product fit. States like California and Florida enforce strict documentation for these suitability reviews, especially for senior clients.

5. Complaint Management and Response Protocols

State regulators track complaint ratios and response timelines. Agencies must have a defined process to log, investigate, and resolve consumer complaints within regulated timeframes. Repeated or unresolved complaints can trigger audits or license reviews.

6. Advertising and Marketing Compliance

All promotional materials such as websites, social media posts, and brochures must meet specific guidelines to avoid misleading statements or unsubstantiated claims. Some states require pre-approval or filing of advertising materials, especially for health and life insurance. This includes disclaimers, use of testimonials, and clarity in benefits explanation.

7. Record Retention and Audit Readiness

Insurance agencies are generally required to retain policy records, customer correspondence, disclosures, and compliance documentation for five to seven years, depending on state law. This recordkeeping must be audit-ready, digitally searchable, and safeguarded from unauthorized access.

Download the free ISO 9001 compliance template for Insurance Industry

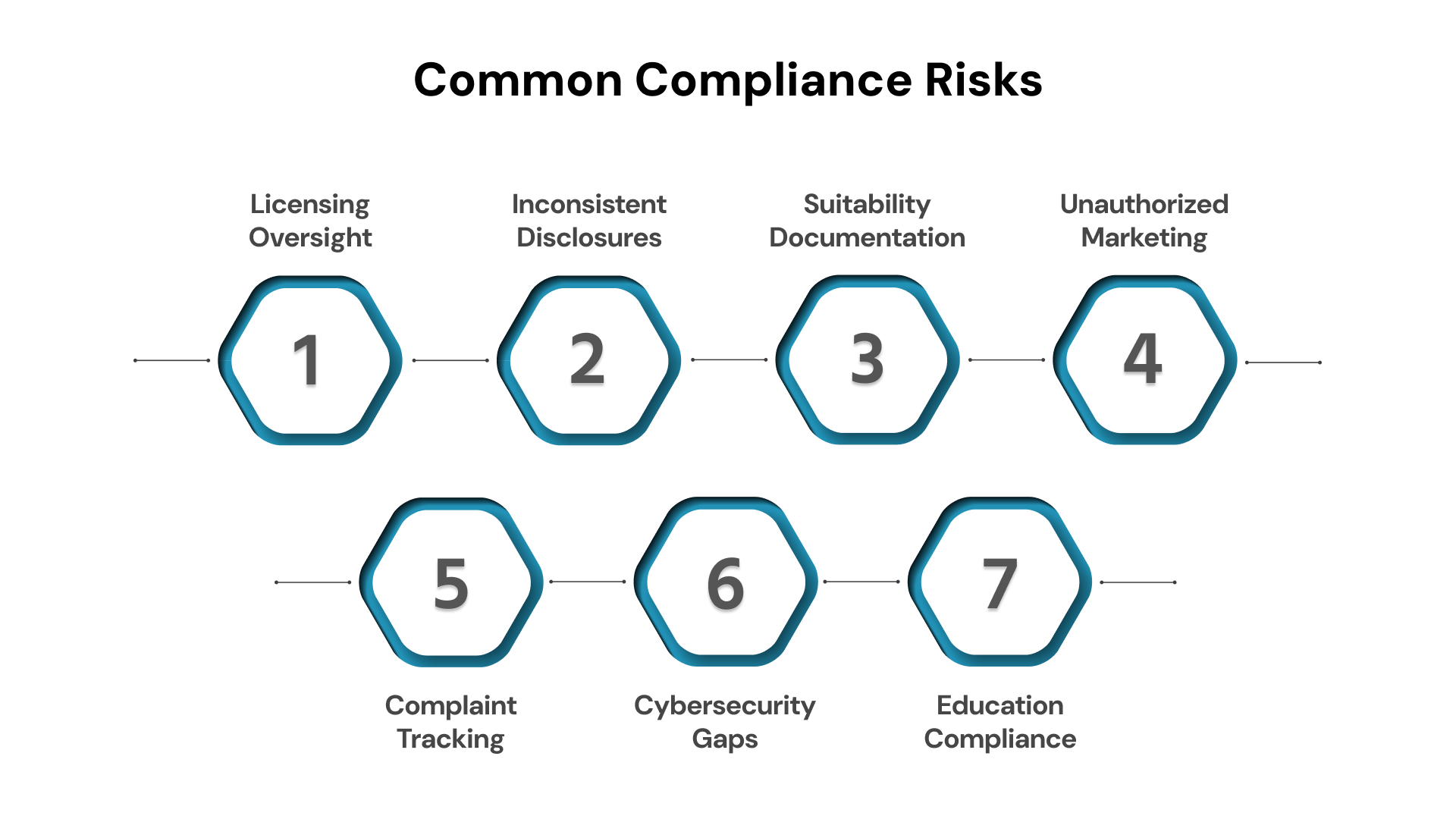

Common Compliance Risks for Insurance Brokers and Agencies

Despite well-established rules, insurance brokers and agencies often face practical challenges in implementing and maintaining compliance across distributed teams, diverse products, and evolving regulations. These vulnerabilities can lead to reputational harm, regulatory fines, or even license revocation.

1. Lack of Centralized Licensing Oversight

Managing producer licenses across multiple states without a centralized system often results in missed renewals or lapsed licenses. This can make sales activity illegal in certain jurisdictions and trigger disciplinary action.

2. Inconsistent Disclosures at Point of Sale

Failure to deliver required disclosures, such as compensation structure, product features, or risk warnings, can create legal exposure. This risk is especially acute in complex policies like variable annuities or indexed universal life products where transparency is critical.

3. Poor Documentation of Suitability Reviews

Even when suitability assessments are performed, inadequate documentation can make it difficult to prove compliance in the event of a dispute or audit. Forms left unsigned, missing financial details, or vague rationale for product recommendations are common gaps.

4. Unauthorized Marketing Practices

Producers sometimes use templated or third-party marketing materials that have not been reviewed for compliance. This increases the chance of misstatements, unapproved claims, or failure to meet state-specific advertising rules, particularly in Medicare Advantage and life insurance promotions.

5. Inadequate Complaint Resolution Tracking

Without a standardized system to log, escalate, and resolve complaints, agencies risk regulatory penalties and erosion of consumer trust. Missed deadlines, lack of follow-up, or informal handling of complaints are red flags during audits.

6. Failure to Implement Cybersecurity Safeguards

Insurance brokers handle large volumes of sensitive personal and financial data. Failing to follow basic cybersecurity protocols, such as two-factor authentication, encrypted storage, or breach notification procedures, exposes firms to data privacy violations under laws like GLBA and state breach notification rules.

7. Untracked Continuing Education Compliance

Many producers fall out of compliance simply due to untracked CE credits or missed deadlines. Without a mechanism to monitor training completion and renewal cycles, agencies risk allowing unauthorized individuals to transact business.

Also read: What is Compliance Risk Management?

Best Practices for Strengthening Compliance Programs

To meet regulatory expectations and reduce exposure, insurance brokers and agencies need to build compliance frameworks that are not just reactive but embedded into daily operations. The following best practices enable a more agile, accountable, and scalable compliance environment.

1. Establish a Role-Based Compliance Hierarchy

Clearly define roles and responsibilities across compliance, operations, and sales teams. Assign designated compliance officers or liaisons who oversee region-specific regulations, ensure licensing accuracy, and validate advertising approvals before materials go live.

2. Adopt a Pre-Approval Workflow for Sales and Marketing Materials

Set up standardized review and approval workflows for marketing collateral. Implement digital checkpoints to flag materials that contain benefit guarantees, performance claims, or non-standard disclosures that might trigger regulatory review.

3. Use Licensing and Appointment Management Tools

Leverage compliance software that automatically tracks license status, appointment renewals, CE requirements, and state-specific rules for every producer. Automated alerts and dashboards can help prevent lapses that could lead to penalties.

4. Standardize Client Onboarding and Suitability Assessments

Develop unified digital forms for onboarding, disclosures, and suitability reviews. Embedding logic into forms (e.g., mandatory fields for income, risk tolerance) helps ensure all relevant factors are considered and documented before product recommendations are made.

5. Create a Centralized Complaint Handling Protocol

Establish a formal workflow that includes complaint intake, categorization, assignment to the appropriate team, resolution deadlines, and reporting. Logging every interaction not only ensures transparency but creates an audit-ready trail for regulators.

6. Implement Quarterly Internal Audits and Random File Reviews

Regular internal reviews can uncover compliance weaknesses before regulators do. Include randomized client file reviews to check for missing signatures, outdated disclosures, or suitability gaps, and use findings to refine training programs.

7. Maintain a Compliance Playbook and Escalation Matrix

Codify policies, procedures, and escalation paths in a centralized document repository. Include guidance for responding to audit requests, breach notifications, and regulatory inquiries so all team members know how to act swiftly and consistently.

8. Foster a Compliance-First Culture Through Ongoing Education

Go beyond CE credits. Host regular webinars, case study breakdowns of enforcement actions, and interactive policy workshops. Recognize and reward staff who report red flags or suggest improvements to compliance processes.

Also read: Insurance Risk and Compliance Management Software Solutions

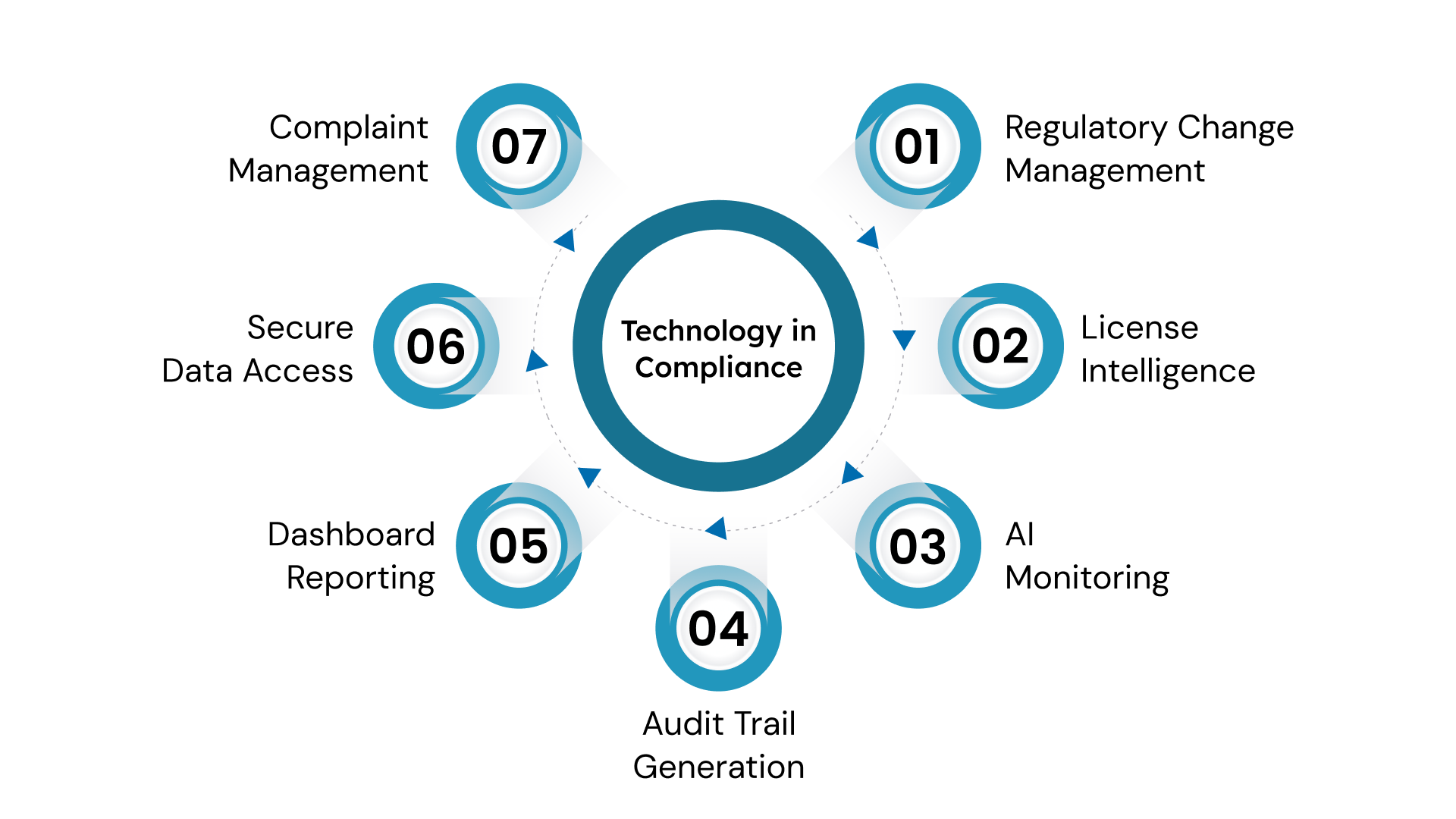

The Role of Technology in Insurance Compliance

Technology is becoming a foundational pillar in managing insurance compliance, especially as firms scale across geographies and product lines. It reduces manual effort, brings consistency across processes, and ensures that real-time oversight is possible at every step.

1. Automated Regulatory Change Management

Regulations change frequently at both federal and state levels. Technology platforms equipped with regulatory feeds or alerts help compliance teams stay ahead by flagging changes, mapping them to internal controls, and assigning follow-up tasks.

2. License and Appointment Intelligence

Advanced compliance tools not only track license validity and appointment statuses but also validate whether a producer is authorized to sell specific products in a given state. This avoids unintentional violations stemming from cross-jurisdictional sales.

3. AI-Powered Document Monitoring

Artificial intelligence can scan marketing and sales documents to identify prohibited phrases, outdated disclosures, or missing disclaimers. This enables scalable review processes even across thousands of materials and ensures consistent regulatory alignment.

4. Integrated Audit Trail Generation

Modern compliance platforms automatically log every action taken, from policy issuance and producer onboarding to client communications and complaint resolutions. These logs create immutable audit trails that are crucial during regulator reviews or investigations.

5. Real-Time Dashboard Reporting

Dashboards provide a live view into compliance metrics across branches, producers, and regions. Whether it is tracking the status of training completions or identifying overdue complaints, dashboards empower proactive intervention before issues escalate.

6. Secure Data Access and Version Control

Role-based access ensures sensitive client and regulatory data is only available to authorized personnel. Platforms with document version control also prevent the circulation of outdated forms or disclosures, which is a common source of regulatory violations.

7. Centralized Complaint and Risk Management

Technology allows firms to map complaints to root causes and recurring policy gaps. Over time, this data becomes invaluable for identifying risk patterns, updating internal controls, and demonstrating continuous improvement to regulators.

Also read: The Impact of Technology on Compliance: Interview with Patrick Henz

How VComply Supports Insurance Compliance for Brokers & Agencies

VComply is purpose-built to help insurance brokers and agencies manage compliance with clarity, control, and continuity. Its modular, cloud-based structure makes it easy to adapt to regulatory changes, automate recurring tasks, and ensure every stakeholder is aligned with current requirements.

- Centralized Compliance Hub: VComply brings all compliance policies, licensing records, disclosures, and internal controls into one system. This eliminates silos across departments or branches and enables faster audits and internal reviews.

- Automated License Tracking and Reminders: The platform can track individual and entity-level license statuses across all U.S. states, triggering alerts before expiration dates. It also helps manage appointments and renewals to prevent lapses in authority.

- Configurable Workflows for Compliance Tasks: From onboarding a new agent to issuing a product-specific disclosure, firms can build automated workflows that standardize compliance procedures across the organization. Each task is tracked, time-stamped, and assigned to ensure nothing falls through the cracks.

- Real-Time Monitoring and Escalation: Dashboards flag pending acknowledgments, unresolved risks, and policy deviations, allowing compliance managers to escalate issues before they evolve into violations. Custom risk scores and visualizations also support reporting to executives or regulators.

- Audit Readiness and Evidence Capture: VComply automatically records document changes, approvals, policy acceptances, and incident logs, creating a complete audit trail. This on-demand access to evidence simplifies external reviews and strengthens internal compliance posture.

- Complaint and Incident Tracking: Built-in modules help log, assign, and resolve complaints or compliance incidents with full visibility. This ensures timely responses and helps identify recurring gaps across product lines or teams.

VComply’s insurance compliance solution is not just about ticking regulatory boxes. It’s designed to simplify complexity and build lasting operational discipline. Whether you’re managing a national brokerage or a growing agency network, VComply equips you with the tools to stay compliant, scalable, and audit-ready. Book a demo!

Final Thoughts

Compliance for insurance brokers and agencies is no longer a static checklist. It requires continuous attention, operational integration, and adaptability to regulatory change. From licensing to client communications and data protection, each aspect must align with a framework that ensures accountability and client trust.

Maintaining compliance is not just about avoiding penalties. It also builds credibility with policyholders, partners, and regulators. Agencies that treat compliance as a strategic function, rather than a reactive obligation, are better positioned for sustainable growth.

Want to simplify how your agency manages compliance? Start a free trial with VComply that supports real-time tracking, centralized documentation, and audit-ready workflows.

FAQs

1. What are the main regulatory authorities that govern compliance for insurance brokers and agencies?

Compliance obligations typically come from state Departments of Insurance (licensing, renewals, advertising), the NAIC’s model laws, and federal regulations like AML rules under the PATRIOT Act and data privacy laws such as GLBA.

2. Do brokers need a formal compliance function or officer?

While not required by law, many agencies appoint a compliance officer or team to manage licensing, training, regulatory updates, documentation, and oversight. This helps avoid missteps and ensures ongoing adherence.

3. What continuing education (CE) obligations apply to insurance producers?

Producers must complete state-mandated CE hours, typically every two to four years, covering insurance law, ethics, and product training. States may revoke or suspend licenses for missed CE.

4. What key protections are required under GLBA for brokers?

GLBA requires the creation of an information security plan, implementation of safeguards including risk assessment and encryption, and procedures to prevent unauthorized access or pretexting.

5. How long must brokers retain records and complaint documentation?

Most states require retention of policy files, disclosures, licenses, and complaint records for five to seven years to ensure audit-readiness and regulatory proof of compliance.