Choosing Compliance Management Solutions for Financial Services

Regulatory failure can cost more than fines; it can cost your license, reputation, and market access.

The SEC secured $8.2 billion in remedies in FY2024, underscoring rising enforcement intensity. Meanwhile, banks’ compliance hours and IT spend have climbed sharply, driving higher overhead and manual process risk.

That’s exactly why choosing the right compliance management solution matters, not just to avoid fines, but to protect growth, reputation, and customer trust.

In this post, we’ll walk you through how to evaluate and select compliance management solutions tailored for financial services: what to prioritize, how solutions map to FFIEC/GLBA/SOX expectations, and metrics to quantify ROI so you can choose a platform that reduces audit burden and strengthens regulatory resilience.

Key Takeaways

- Financial services compliance requires execution, not documentation. Regulators evaluate how controls are performed, tested, and evidenced, not just whether policies exist.

- Generic or document-centric tools increase regulatory risk. Without control mapping, audit trails, and remediation tracking, institutions struggle during exams.

- Effective compliance software operationalizes regulations. GLBA, SOX, FFIEC, and SEC requirements must translate into assigned controls, scheduled testing, and real-time accountability.

- Continuous audit readiness is a competitive advantage. Capturing evidence at the point of execution reduces exam disruption and follow-up findings.

- Common selection mistakes undermine compliance maturity. Weak evidence controls, poor remediation workflows, and limited visibility create governance gaps.

What Is A Compliance Management Solution For Financial Services?

A compliance management solution for financial services is a specialized software platform that centralizes, automates, and evidences how a bank, insurer, asset manager, or fintech complies with all applicable regulations, internal policies, and industry standards.

Instead of scattered spreadsheets, email trails, and standalone tools, it becomes the “control tower” for regulatory obligations, risks, controls, monitoring, and reporting across the institution.

A compliance management solution does not replace AML, transaction monitoring, or cybersecurity tools. Instead, it governs the controls, documentation, and oversight around how those tools are used and how regulatory expectations are met.

Once you understand what a true compliance management solution is meant to do, the next step is recognizing that not all solutions in the market are built for the same regulatory depth or financial services scrutiny.

Types of Compliance Management Solutions In The Market

Compliance management solutions vary widely in scope, maturity, and suitability for financial services. Many platforms appear similar on the surface, but their underlying design determines whether they can withstand regulatory examinations, audits, and enforcement reviews.

Below is a clear breakdown of the primary solution types you will encounter and where each fits or falls short.

1. Manual and Spreadsheet-Based Systems (Legacy Approach)

Many financial institutions still rely on spreadsheets, shared drives, and email-based workflows to manage compliance activities.

- Controls are tracked in static files with limited version control.

- Evidence is stored across folders, which slows and degrades retrieval.

- Accountability depends on individual follow-ups rather than automated workflows.

This approach cannot scale, lacks audit trails, and creates high risk during FFIEC exams or SOX audits where regulators expect structured, time-stamped evidence.

2. Generic Enterprise Compliance Tools

These platforms are designed for broad corporate compliance use across industries.

- Offer basic task management, document storage, and reporting.

- Often configurable but not mapped natively to financial regulations.

- Require heavy customization to support GLBA, SOX, or SEC workflows.

They treat compliance as a project-management exercise rather than a regulated control environment, leading to gaps in examiner-ready documentation.

3. Point Solutions for Specific Functions

These tools focus on one compliance area, such as policy management or issue tracking.

- Strong depth in a single function.

- Limited visibility across the full compliance lifecycle.

- Poor integration between controls, policies, risks, and issues.

Fragmentation forces teams to reconcile data manually, increasing the likelihood of inconsistencies during audits or regulatory reviews.

4. Legacy GRC Platforms (On-Prem or Semi-Cloud)

Older GRC systems were built primarily for large enterprises.

- Comprehensive feature sets, but complex to configure and maintain.

- Long implementation cycles and high total cost of ownership.

- Limited flexibility for evolving regulatory requirements.

These platforms struggle to support agile compliance operations, especially for fintechs and mid-sized banks facing frequent regulatory change.

5. Cloud-Native, FS-Focused Compliance Management Platforms

Modern platforms are purpose-built for regulated industries, including financial services.

- Native mapping to US financial regulations and frameworks.

- Automated workflows for control testing, attestations, and remediation.

- Centralized, immutable evidence repositories aligned with examiner expectations.

- Modular design supporting compliance, risk, policy, and incident

VComply delivers cloud-native compliance management solutions purpose-built for financial services, enabling teams to automate control testing, centralize evidence, and maintain continuous audit readiness.

Once the right category of solution is clear, the real test is how effectively it supports the day-to-day compliance realities unique to financial services.

Key Compliance Management Use Cases Specific to Financial Services

Compliance in financial services is not a single workflow—it is a series of interdependent activities that regulators expect to be executed continuously and documented without gaps.

Below are the most critical use cases where purpose-built compliance management solutions deliver measurable value.

1. Translating Regulations Into Executable Controls

Financial regulations are written at a principal level, but exams are conducted at the control level. A compliance management solution acts as the translation layer.

In practice, this means regulations such as GLBA or FFIEC guidance are broken down into internal control statements, each assigned to a specific owner, business unit, and testing frequency. Instead of relying on institutional knowledge, the platform preserves this structure as a living system, one that can be reviewed, tested, and updated as regulations evolve.

2. Proving Continuous Control Execution

Financial institutions are increasingly evaluated on consistency, not annual readiness.

A compliance management solution supports this by scheduling recurring control tests and owner attestations throughout the year. Evidence screenshots, reports, and approvals are attached directly to each test, creating a time-stamped history of execution rather than a last-minute audit scramble.

3. Governing Policies as Enforceable Controls

Policies are a frequent focus area during exams because they reflect management intent.

With a compliance management solution, policies are not static documents. Each policy is version-controlled, mapped to applicable controls, distributed to the correct audience, and supported by employee attestations. This ensures institutions can demonstrate that policies are current, approved, communicated, and acknowledged.

4. Responding to Exams and Audits Without Disruption

Exams often fail institutions not because controls are missing, but because evidence is fragmented.

A centralized compliance platform enables teams to respond to examiner requests by generating structured evidence packages that show control definitions, testing history, issues, and remediation in a single view. This reduces back-and-forth with regulators and minimizes operational disruption during exams.

5. Managing Findings and Remediation as a Closed Loop

Every audit or exam produces findings. What regulators care about is how quickly and effectively those findings are resolved.

Compliance management solutions formalize this process by logging each finding, assigning remediation tasks, tracking progress, and capturing evidence of closure. Management sign-off and timelines are documented automatically.

6. Maintaining Oversight of Third-Party Compliance Risk

Vendors are an extension of a financial institution’s risk posture.

A compliance management solution enables institutions to document vendor obligations, track due diligence, and link third-party risks to internal controls. This ensures vendor compliance is monitored continuously rather than revisited only during exams.

When regulatory expectations, evidence standards, and oversight intensity are viewed together, it becomes clear why financial services cannot rely on generic compliance tools.

Why FS-Specific Compliance Solutions Are Needed

Financial services organizations operate under continuous regulatory supervision where compliance is evaluated through execution, evidence, and governance.

FS-specific compliance management solutions are designed to meet examiner expectations by embedding regulatory structure, accountability, and audit defensibility into daily operations, rather than relying on manual processes or post-hoc documentation.

FS-specific compliance management solutions are necessary because they address requirements that generic platforms are not built to handle:

- Continuous regulatory oversight: Financial institutions face ongoing examinations and supervisory reviews, requiring controls to be executed and documented consistently throughout the year.

- Examiner-grade evidence standards: Regulators expect time-stamped, traceable proof of who performed actions, what was reviewed, and when approvals occurred.

- Overlapping regulatory frameworks: Controls must map simultaneously to GLBA, SOX, FFIEC guidance, and SEC requirements without manual reconciliation.

- Clear and enforceable accountability: Control ownership, approvals, and remediation responsibilities must be formally assigned and auditable across business units.

- Integrated third-party oversight: Vendor compliance and risk must be monitored continuously and linked directly to internal controls and remediation workflows.

Once the need for FS-specific solutions is clear, the next step is to identify the capabilities that determine whether a platform can withstand regulatory scrutiny.

Must-Have Features For FS Compliance Management Solutions

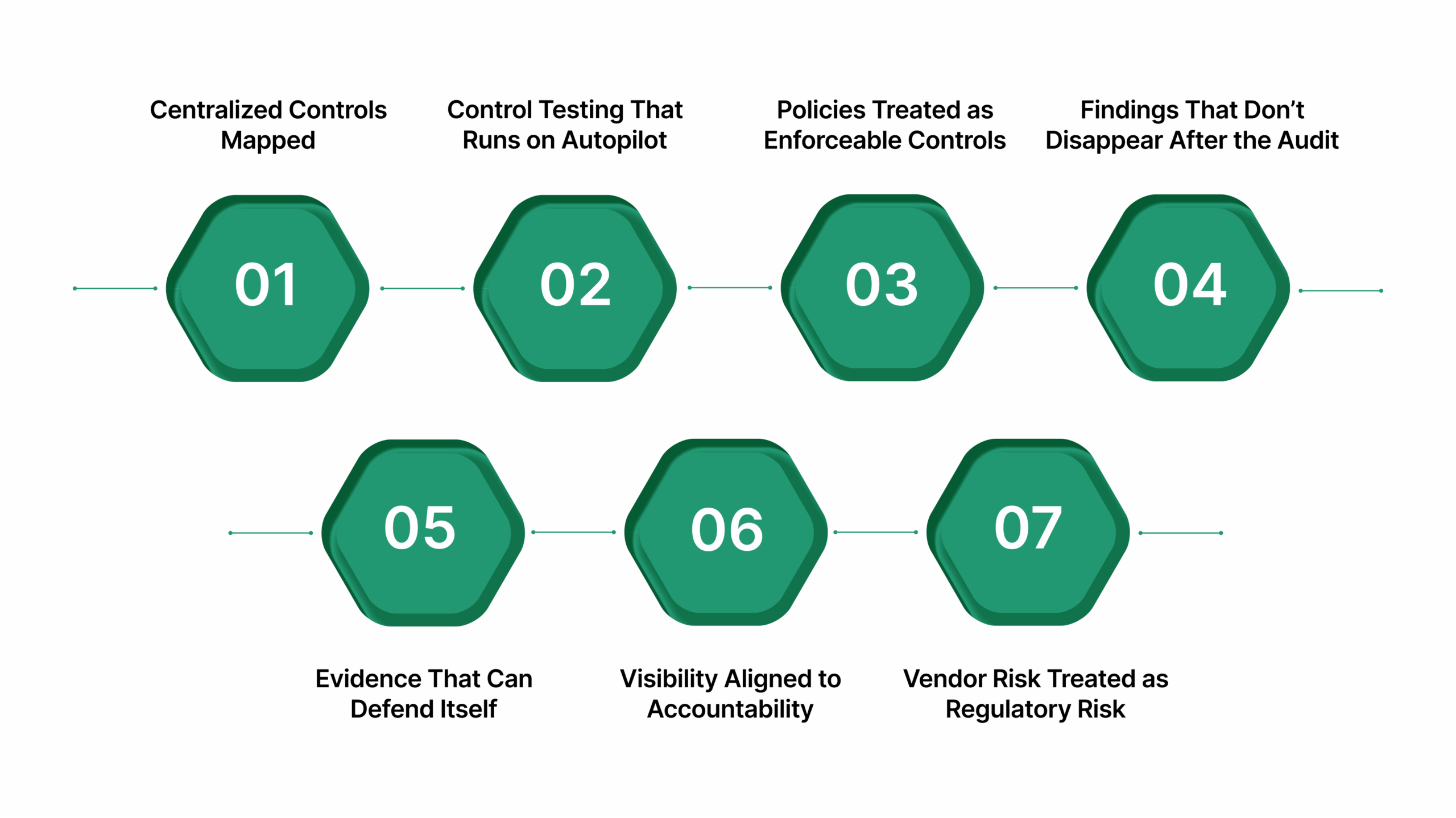

For financial institutions, compliance software must support execution, proof, and governance, not just tracking. The following features determine whether a solution can withstand regulatory examinations.

1. Centralized Controls Mapped to Financial Regulations

Financial institutions operate under overlapping mandates, including GLBA, SOX, FFIEC, and SEC regulations. Compliance software must structure controls around these requirements, not around departments.

A single control, such as access reviews, should map to multiple regulations, retain its change history, and show when and how it was executed. This structure allows examiners to trace regulatory intent directly to operational proof.

2. Control Testing That Runs on Autopilot

Regulators expect controls to be tested consistently, not ad hoc.

Effective platforms automate testing schedules based on risk, collect owner attestations, and attach evidence when the control is performed. The result is a living compliance record that reflects real operations rather than end-of-quarter scrambling.

3. Policies Treated as Enforceable Controls

In financial services, policies are not reference documents; they are enforceable standards.

A strong solution manages policy versions, approvals, employee distribution, and acknowledgments in one place. When examiners ask how a policy is enforced, the system must show who approved it, who received it, and who attested to it.

4. Findings That Don’t Disappear After the Audit

Audit and examination findings signal governance maturity.

Instead of static spreadsheets, modern platforms log findings with severity, assign remediation owners, track deadlines, and require closure evidence. Management sign-off completes the accountability loop that regulators look for.

5. Evidence That Can Defend Itself

Evidence must be credible before it is complete.

That means time-stamped uploads, immutable records, and a clear history of actions taken. When evidence is structured and searchable, institutions reduce examiner follow-ups and avoid rework during regulatory reviews.

6. Visibility Aligned to Accountability

Different roles require different insights.

Control owners need task-level clarity. Compliance leaders need real-time readiness views. Executives need a summarized risk exposure. Role-based dashboards ensure the right decisions are made at the right level without overexposing data.

7. Vendor Risk Treated as Regulatory Risk

Third-party failures remain the institution’s responsibility.

Compliance software must track vendor obligations, link vendor risks to internal controls, and document ongoing monitoring. This ensures outsourced services meet the same regulatory standards as internal operations.

Once the right capabilities are in place, the real value comes from how those capabilities operate together as a single, defensible compliance workflow.

How Financial Services Compliance Software Works?

At its core, financial services compliance software functions as a control execution and evidence system, not a document store.

Regulatory obligations such as GLBA, SOX, FFIEC guidance, and SEC rules are first converted into defined controls. Each control has a named owner, a required frequency, and a risk rating. Where regulations overlap, the same control is reused, eliminating duplicate testing and documentation.

Execution then becomes automatic.

Controls generate scheduled tasks with clear deadlines. Owners know exactly what is required, and compliance teams can immediately see progress, delays, and gaps without chasing emails or spreadsheets.

Proof is captured at the moment of work.

Evidence is uploaded directly to the control, time-stamped, and supported by attestations. Every action is logged, creating an audit trail regulators can trust.

Failures trigger a structured response.

If a control fails or an audit issue arises, the system records severity, assigns remediation, and requires evidence before closure. Issues remain visible until resolved.

Policies reinforce compliance behavior.

Policy updates are distributed automatically, acknowledgments are tracked, and policy alignment with controls is maintained, demonstrating enforcement, not just intent.

Oversight is continuous, not retrospective.

- Control owners see assigned actions

- Compliance teams track readiness in real time

- Executives view the summarized compliance status

Together, this structure replaces reactive, exam-driven compliance with a continuous, defensible operating model.

Even the strongest compliance workflows can break down if the underlying platform is poorly chosen, often in ways that only surface during regulatory exams.

Common Mistakes To Avoid When Choosing Compliance Solutions

Financial institutions often select compliance solutions based on convenience or cost rather than regulatory defensibility. These decisions usually surface as problems during audits, regulatory exams, or remediation reviews when gaps are hardest to fix.

The following mistakes consistently weaken compliance outcomes in financial services environments.

- Choosing document-centric tools instead of control-driven systems. Platforms that store files but do not link to regulations, controls, tasks, and evidence cannot prove how compliance is executed.

- Using generic GRC software without financial services alignment. Tools lacking native support for GLBA, SOX, FFIEC, and SEC requirements force manual workarounds and weaken examiner confidence.

- Accepting weak evidence and audit trail controls. Missing time stamps, editable records, or unclear ownership undermines evidence credibility during exams.

- Separating remediation from compliance tracking. Managing audit findings outside the system results in poor accountability and unresolved issues.

- Treating policies as static documents. Without policy distribution and employee attestations, institutions cannot demonstrate enforcement.

- Ignoring role-based visibility needs. When owners, compliance teams, and executives lack tailored views, risks remain hidden until audits.

- Failing to plan for regulatory change and scale. Platforms that cannot adapt to new rules, entities, or exam expectations become long-term liabilities.

Once institutions understand what to avoid, the next step is choosing a platform purpose-built to meet financial services regulatory expectations at scale.

How VComply Supports Financial Services Compliance at Scale?

VComply is a US-based, cloud-native GRC platform designed to help financial institutions operationalize compliance across complex regulatory environments.

Rather than functioning as a tracking or document storage tool, ComplianceOps acts as a centralized system of record for compliance execution, connecting regulatory requirements, controls, testing, and evidence in one defensible workflow.

This enables financial institutions to demonstrate how compliance is performed, not just that policies exist.

Here’s how ComplianceOps supports financial services compliance:

- Regulatory-aligned control management: Manage GLBA, SOX, FFIEC, and SEC-aligned controls across multiple business units within a single framework, reducing duplication and inconsistency.

- Automated control testing and scheduling: Controls trigger testing activities based on defined regulatory cadence, ensuring continuous compliance instead of point-in-time readiness.

- Evidence captured at execution: Proof is uploaded directly to controls with time stamps and ownership, creating the immutable audit trails examiners expect.

- Clear ownership and accountability: Control owners, deadlines, and completion status are visible in real time, reducing reliance on manual follow-ups.

- Continuous audit readiness: Compliance teams can quickly respond to examiner requests using centralized, pre-validated evidence without last-minute scrambling.

For financial institutions seeking scalable, defensible compliance operations, VComply ComplianceOps delivers a purpose-built platform aligned with how regulators evaluate compliance in practice.

Start a 21-day free trial of ComplianceOps to see how VComply helps financial services teams centralize controls, automate compliance execution, and maintain continuous audit readiness at scale.

Final Thoughts

Choosing the right compliance management solution for financial services is no longer a technology decision it is a regulatory risk decision.

Financial institutions operate under constant scrutiny from regulators enforcing GLBA, SOX, FFIEC guidance, and SEC requirements, where exam outcomes depend on the ability to demonstrate consistent control execution, credible evidence, and disciplined remediation.

VComply addresses these challenges by providing a unified, cloud-native GRC platform built for financial services scale. By aligning ComplianceOps and GRCOps into a single system of record, VComply enables institutions to move from reactive, audit-driven compliance to continuous, regulator-ready operations without increasing operational burden.

If your organization is evaluating compliance management solutions for financial services, explore how VComply’s ComplianceOps and integrated GRC platform can centralize controls, automate evidence, and strengthen regulatory defensibility across your enterprise. Book a demo today!

FAQs

It provides centralized access to controls, evidence, and audit trails, allowing institutions to respond to examiner requests quickly without manual data gathering or last-minute document preparation.

Yes. Advanced solutions allow one control to map to multiple regulatory requirements, enabling institutions to manage overlapping obligations from federal and state regulators efficiently.

By assigning clear control ownership, tracking task completion, and recording attestations, the platform ensures responsibilities are documented and enforceable across teams.

It supports continuous compliance by scheduling control activities, capturing ongoing evidence, and tracking remediation so readiness is maintained year-round, not just before audits.

ROI is measured through reduced audit preparation time, fewer exam findings, faster remediation cycles, and improved visibility for compliance leadership and executives.