Understanding AML Screening: Complete Guide

The primary challenge for compliance leaders in 2026 is balancing the need for speed with the mandate for absolute data accuracy. When matching logic is too broad, it creates a backlog of false positives that drain resources; when it is too narrow, it risks missing an OFAC or FinCEN hit that could lead to personal liability for executives.

Effective AML screening solves this friction by acting as a precision filter. By moving away from fragmented, manual checks and toward integrated data workflows, institutions can intercept high-risk entities at the point of entry without disrupting legitimate customer growth.

This guide provides a functional breakdown of the screening lifecycle, the technical hurdles of 2026, and the governance frameworks required to maintain a defensible compliance program.

Key Takeaways

- Effective screening blocks high-risk actors at the point of onboarding, preventing the need for costly post-transaction remediation.

- Modern programs prioritize high-availability, cloud-native infrastructure that can handle real-time screening without creating operational bottlenecks.

- Success depends on breaking down silos between Know Your Customer (KYC) data and screening results to create a holistic risk profile.

- As AI tools become more prevalent, the ability to provide an auditable rationale for screening decisions is a mandatory requirement for federal examiners.

What is AML Screening?

AML screening is the process of verifying a customer’s identity against diverse lists of sanctioned individuals, entities, and jurisdictions. Unlike transaction monitoring, which evaluates a customer’s behavior over time, screening serves as a checkpoint that establishes the eligibility and risk level of a client before or during the start of a relationship.

For US-based firms, this process is dictated by the Bank Secrecy Act (BSA) and the Office of Foreign Assets Control (OFAC). The objective is to identify risk factors, such as hidden beneficial ownership, that make a relationship legally untenable. In 2026, this requirement involves resolving complex corporate layers to identify the actual individuals behind an entity.

Why is AML Screening a Strategic Priority?

A precise screening program maintains regulatory adherence and mitigates institutional risk. By identifying high-risk actors during onboarding, firms prevent the entry of funds from sanctioned regimes, narcotics traffickers, or terrorist organizations.

Beyond the legal mandate, effective screening supports institutional stability. It ensures that resources are not diverted to managing the fallout of enforcement actions or the public loss of investor confidence that follows a significant compliance failure.

Also Read: Step-by-Step Guide to AML/CTF Compliance Programs

A comprehensive framework relies on several specialized datasets to move from basic checks to a defensible, risk-based program.

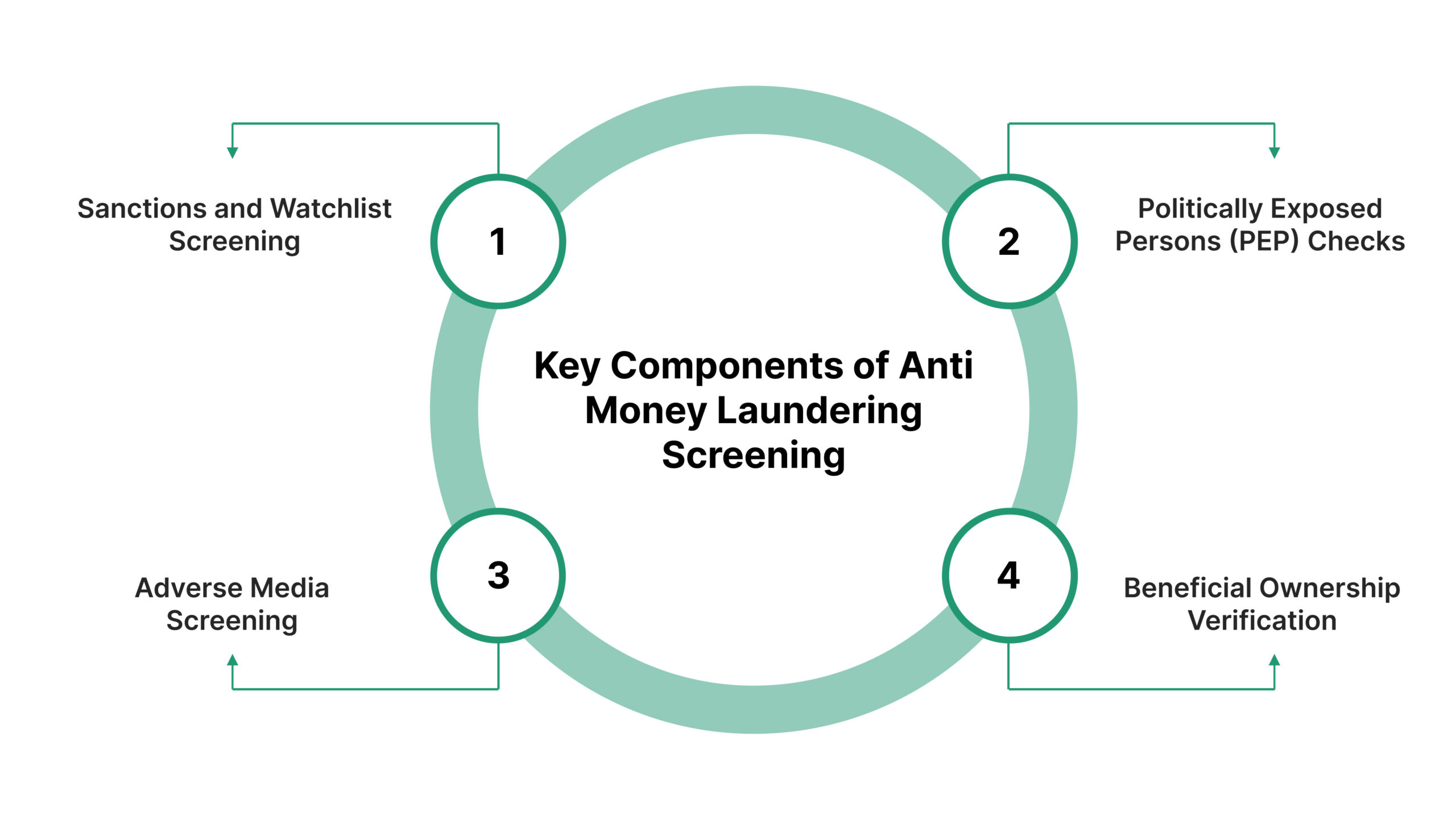

What are the Primary Components of AML Screening?

A precise framework in 2026 relies on four specific data layers. These components allow an institution to identify different risk profiles during the onboarding and periodic review processes.

1. Sanctions and Watchlist Screening

This is the most immediate requirement for any US financial institution. It involves cross-referencing names against the Specially Designated Nationals (SDN) list and other official watchlists. As sanctions are frequently updated in response to global events, real-time integration with OFAC updates is necessary to prevent violations that result in severe enforcement penalties.

2. Politically Exposed Persons (PEP) Checks

A PEP is an individual who holds a prominent public position, which inherently increases their exposure to potential bribery or corruption. Anti-money laundering screening must identify these individuals, as well as their family members and close associates.

While being a PEP is not a crime, it requires Enhanced Due Diligence (EDD) to ensure the source of their wealth and funds is legitimate.

3. Adverse Media Screening

Information regarding a person’s involvement in criminal activity often appears in public reports long before they are added to an official sanctions list. Adverse media screening involves scanning news, social media, and court records for reports of fraud, money laundering, or other financial crimes.

In 2026, this is powered by natural language processing tools that can distinguish between a person being a subject of an investigation and a person mentioned in an unrelated context.

4. Beneficial Ownership Verification

Under the Corporate Transparency Act (CTA), screening a corporate entity requires identifying the “Ultimate Beneficial Owners” (UBOs), the individuals who own or control at least 25% of the company.

Even though certain reporting requirements for domestic US companies are currently under review as of January 2026, foreign entities doing business in the US must still comply, making UBO screening a critical task.

Effective screening provides the initial risk profile, but the accuracy of these results depends on the underlying technology and logic used to process the data.

How Do AML Screening and Monitoring Function as a Unified System?

In a mature compliance framework, screening and monitoring are not siloed activities; they are interconnected data streams that provide continuous oversight. While they serve different immediate purposes, their integration is what allows an institution to maintain a defensible, risk-based program.

Screening: The Identity Check

Screening is about identity. It asks who the person is and whether they are allowed to use your services. It is typically performed at onboarding and during periodic intervals when watchlists are updated. It is a snapshot in time that determines the baseline risk level of a new client.

Monitoring: The Behavioral Check

Transaction monitoring is about activity. It asks what the person is doing and whether that activity makes sense for their profile. If a customer passes the initial AML screening, the monitoring system then watches their transactions for anomalies such as rapid fund movement or unusual cash deposits.

What are the Benefits of a Unified Approach?

By integrating AML screening and monitoring, you create a feedback loop. For example, if a customer’s risk status changes during a periodic rescreening, such as a new association with a high-risk jurisdiction, the system can automatically lower the alert thresholds in the transaction monitoring module. This ensures that resources are prioritized toward higher-risk entities without increasing manual workloads.

| Feature | AML Screening | AML Transaction Monitoring |

| Focus | Identity and Status | Behavior and Patterns |

| Timing | Onboarding and Periodic | Ongoing and Continuous |

| Data Source | Watchlists, PEP lists, Media | Transaction logs, peer groups |

| Primary Goal | Block prohibited entities | Detect suspicious activity |

Suggested Read: Understanding the Biggest AML Fines in 2024

While a unified framework reduces systemic gaps, managing it day-to-day often creates operational friction that can strain your team. Explore how ComplianceOps provides the framework to link these data streams, giving you a clear and continuous view of customer risk without the manual overhead.

What are the Primary Challenges in the AML Screening Process?

Operational efficiency is the greatest challenge for many compliance departments in 2026. High volumes of data and the need for precision often lead to bottlenecks that can stall customer onboarding and increase costs.

1. Managing False Positives

The most common issue in anti-money laundering screening is the false positive, where a legitimate customer is flagged because they share a name with a sanctioned individual.

In 2026, the cost of manually reviewing these alerts is unsustainable. Firms are now utilizing secondary identifiers, such as date of birth, nationality, and physical address, to automatically dismiss matches that do not meet a specific similarity threshold.

2. Resolving Name Variations and Scripts

Criminals often use aliases or different spellings to evade detection. Furthermore, names translated from non-Latin scripts, such as Cyrillic or Arabic, can have multiple English variations.

To solve this, sophisticated screening engines use approximate string matching, often called fuzzy matching, to identify potential matches even when the spelling is not identical.

3. The Complexity of Global Jurisdictions

As geopolitical tensions rise, the list of high-risk jurisdictions is constantly in flux. Screening systems must be able to handle “jurisdictional divergence,” where different regulators may have different levels of restrictions on the same country. Maintaining a dynamic and up-to-date database is critical for avoiding regulatory gaps.

4. Data Silos and Inefficiency

When KYC data is stored separately from screening tools, analysts lack the context needed to make quick decisions. For example, knowing that a customer is a high-ranking government official (PEP) is only useful if that information is immediately available to the analyst reviewing an alert for a large wire transfer.

The transition from manual, legacy processes to intelligent, automated systems is the only way to resolve these structural inefficiencies.

How are AI and Automation Reshaping AML Screening in 2026?

Compliance frameworks in 2026 prioritize systems that can process logic, justify decisions, and integrate into real-time workflows. The shift is away from basic rule-based automation toward models that can reason, prioritize, and explain their decisions to human overseers.

Agentic AI and Explainability

Regulators now demand that any AI used in AML screening be explainable. This means the system must provide a clear audit trail showing why it determined a match was a false positive or why it elevated a specific alert.

This transparency is a key focus of the SEC’s 2026 priorities, which aim to prevent misleading claims about AI capabilities.

Real-Time, Cloud-Native Infrastructure

The speed of modern finance requires screening to happen in milliseconds. Legacy systems that rely on batch processing are being replaced by cloud-native platforms that offer sub-100ms API performance.

This ensures that AML screening remains a background process that does not negatively impact the customer experience during onboarding.

Reducing Noise with Machine Learning

Machine learning algorithms are now being trained on historical alert data to predict which matches are likely to be false positives. By filtering out the noise, these systems allow human analysts to focus their attention on the small percentage of alerts that represent a significant risk.

These technical improvements set the stage for a mature compliance program, which ultimately relies on disciplined, risk-based operational practices.

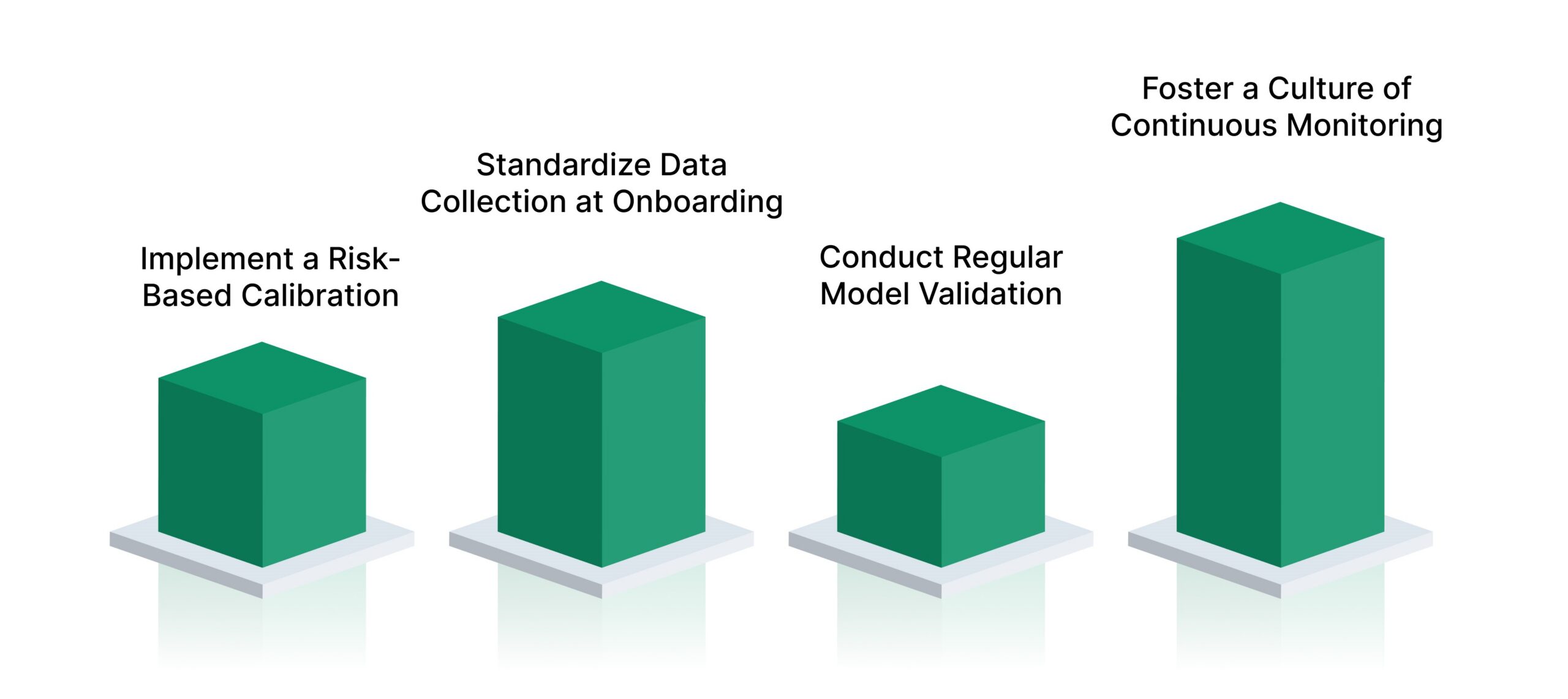

What are the Best Practices for an Effective AML Screening Program?

To withstand the scrutiny of a federal examination in 2026, compliance programs must move away from check-the-box activity. A defensible framework requires a risk-based structure, robust data quality, and continuous model validation.

1. Implement a Risk-Based Calibration

Compliance programs cannot treat every customer equally. Calibrate your screening thresholds based on the risk profile of your customer segments. A domestic retail customer may require a different level of approximate string matching than a high-net-worth international client. This prioritization ensures that your team is focusing on the most likely threats.

2. Standardize Data Collection at Onboarding

Data quality is the foundation of screening accuracy. By enforcing strict standards for data entry during the onboarding process, you can provide your screening engine with the secondary identifiers it needs to reduce false positives. Missing dates of birth or incomplete addresses are the primary drivers of alert noise.

3. Conduct Regular Model Validation

Your screening engine is a model, and like any model, it must be validated. Perform regular stress tests by running known aliases through the system to see if they are flagged. This independent testing is a requirement for both the BSA and the SEC, ensuring that your controls are functioning as intended.

4. Foster a Culture of Continuous Monitoring

Screening is not a one-time event. Implement perpetual KYC (pKYC) workflows that automatically rescreen your entire customer base whenever a major watchlist is updated. This ensures that you are the first to know when a client’s risk status changes, allowing for immediate action.

Suggested Read: Master 2026 Compliance With Risk Management and Governance Practices

Implementing these best practices requires a centralized platform that can manage the complex interplay of data, risk, and regulation.

Strengthen AML Screening Governance with ComplianceOps

AML screening is only effective when institutions can prove how decisions were made, who approved them, and whether controls were consistently executed. ComplianceOps supports this by turning AML screening from a point-in-time check into a governed, auditable compliance process.

With ComplianceOps, organizations can:

- Centralize AML screening controls and obligations: Map AML screening requirements to defined controls with clear ownership, review frequency, and accountability across onboarding and rescreening workflows.

- Maintain examiner-ready evidence: Attach screening outcomes, alert resolutions, and reviewer decisions directly to controls, creating time-stamped, immutable audit trails that regulators expect.

- Track screening effectiveness over time: Monitor missed screenings, overdue reviews, and unresolved alerts through real-time dashboards instead of manual follow-ups and spreadsheets.

- Standardize screening governance across teams: Ensure consistent screening practices across business units by enforcing defined procedures, approval flows, and documentation standards.

- Support explainability and oversight: Preserve the rationale behind screening decisions, especially when automation or AI-assisted tools are used, helping teams respond confidently to regulatory inquiries.

Start a 21-day free trial to see how ComplianceOps helps centralize AML screening oversight and maintain continuous audit readiness.

Conclusion

Effective AML screening in 2026 is no longer about simply clearing names against a static list. As regulatory enforcement intensifies, the true measure of a mature program is the ability to prove that decisions are governed, evidence is archived, and risk is managed in real-time.

Institutions that fail to bridge the gap between screening data and actionable governance risk not only face enforcement penalties but also significant operational friction. Conversely, those that centralize their compliance operations gain the transparency required to satisfy examiners while maintaining the agility needed for growth.

Moving away from fragmented tools toward an integrated, audit-ready framework is the only way to transform compliance from a defensive hurdle into a source of operational resilience.

Book a demo to see how VComply’s ComplianceOps can strengthen AML screening governance and support regulator-ready compliance across your organization.

Frequently Asked Questions (FAQs)

Exact matching only flags a result if the input name is identical to the entry in the database. Approximate string matching, often used in AML screening, assigns a similarity score that accounts for typos, aliases, and name variations. This is essential for identifying criminals who intentionally use slight variations of their names to avoid detection.

In January 2026, FinCEN announced a delay of the rule until 2028. This decision was made to allow the agency more time to tailor the requirements to the diverse business models within the investment adviser sector and to ease the immediate compliance burden on the industry.

Generally, yes. Adverse media is unstructured data, meaning it can contain many reports that are not relevant to financial crime. However, it is a vital early warning system. Modern AI tools help manage this by using sentiment analysis to filter out irrelevant news and focus on credible reports of criminal activity.

While certain requirements for US companies have fluctuated, foreign entities authorized to do business in the US must still report their beneficial owners to FinCEN. For financial institutions, this means you must screen not only the foreign entity but also the individuals identified in their BOI reports.

The SEC has signaled a zero-tolerance policy for systemic failures in AML programs. Consequences include significant monetary penalties, public enforcement actions, and potentially being prohibited from certain types of business activities until the deficiencies are remediated.