CPA Firms Compliance: Essential Requirements Guide

Compliance in CPA firms involves adhering to federal, state, and professional standards that govern services and operations. This includes regulations such as the Sarbanes‑Oxley Act, state licensing rules, AICPA ethics, and PCAOB auditing standards, covering areas like financial reporting, tax preparation, client confidentiality, data security, and internal controls. Compliance is essential to protect client trust, avoid penalties, and reduce the risk of legal or reputational damage. For CPA firms, it’s about ensuring that staff, policies, and procedures align with these regulations daily, managing risk, supporting accountability, and maintaining a strong practice reputation.

Compliance is a fundamental aspect of operating a Certified Public Accountant (CPA) firm in the United States. The regulatory landscape is complex, and maintaining compliance with federal, state, and industry-specific standards is crucial for preserving the firm’s reputation, safeguarding client data, and ensuring seamless operations.

Roughly 80% of accounting firms in the U.S. must now comply with the Corporate Transparency Act (CTA), which has required the filing of Beneficial Ownership Information (BOI) reports since January 1, 2024. This change affects tens of millions of small businesses, including most small CPA firms. CPA firms must understand these compliance requirements to avoid legal risks, financial penalties, and reputational damage.

Key Takeaways (TL;DR)

-

Learn how CPA firm compliance ensures adherence to federal, state, and professional standards.

-

Understand key regulations including GAAP, IRS rules, PCAOB standards, and state licensing requirements.

-

Discover how ethics, client confidentiality, and data security underpin trust and professional integrity.

-

See how structured policies, audits, and staff training strengthen compliance and reduce operational risks.

-

Explore tools like VComply to automate tasks, track policies, and maintain audit-ready documentation.

Understanding Compliance in CPA Firms

Compliance in CPA firms refers to adhering to federal, state, and professional standards that govern the performance of services and the operation of firms. This includes regulations like the Sarbanes‑Oxley Act, state licensing rules, AICPA ethics, and PCAOB auditing standards. It covers areas such as financial reporting, tax preparation, client confidentiality, data security, and internal controls. Compliance isn’t optional; it’s required to protect client trust, avoid penalties, and reduce the risk of legal or reputational damage. For CPA firms, compliance is about making sure staff, policies, and procedures align with these rules every day. It’s a core part of managing risk, supporting accountability, and keeping the practice in good standing.

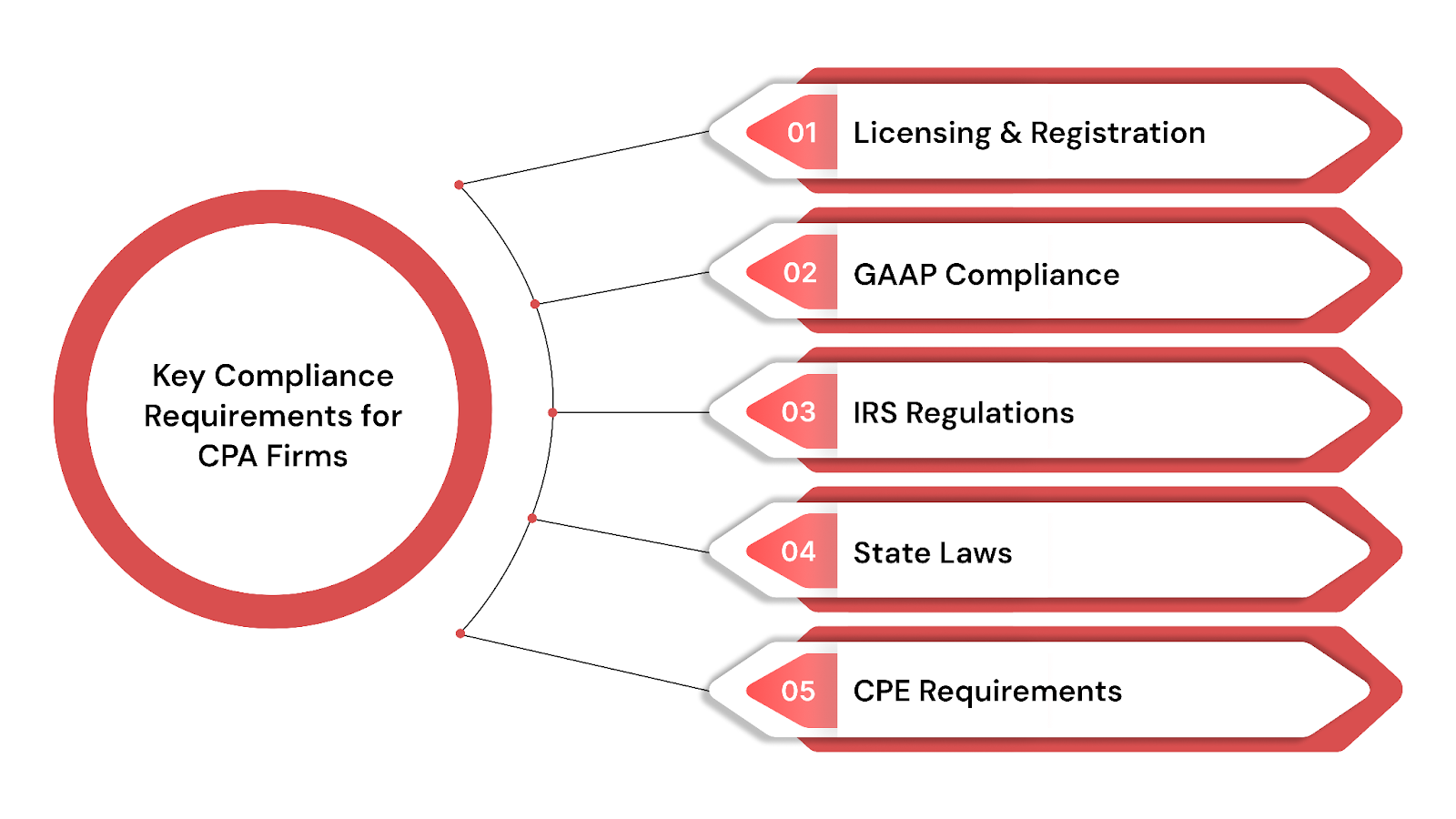

Key Compliance Requirements for CPA Firms

Adhering to compliance requirements is at the core of any CPA firm’s operations. Understanding the key regulatory areas and implementing best practices ensures firms meet legal obligations and maintain high professional standards. Here are the critical compliance areas every CPA firm must focus on:

1. Licensing and Registration

One of the first steps in ensuring compliance for CPA firms is making sure that both the firm itself and the individual CPAs are properly licensed and registered. Each state has its licensing requirements, including passing the CPA exam and meeting the necessary educational and professional experience standards. Firms must also ensure their registration is up to date, as expired licenses can lead to penalties and loss of the ability to perform certain tasks, such as audits or tax filing.

2. GAAP (Generally Accepted Accounting Principles)

GAAP is the standard accounting framework used in the U.S. to ensure consistency and transparency in financial reporting. CPA firms must adhere to these principles when preparing financial statements, ensuring that the statements are accurate, reliable, and meet the needs of stakeholders. Compliance with GAAP also aids in audits and financial analyses, helping firms maintain credibility with clients, investors, and regulatory bodies.

3. IRS Regulations

Compliance with IRS regulations is a top priority for CPA firms that handle tax matters. The Internal Revenue Service provides complex rules and guidelines for tax preparation and reporting. This includes proper documentation of income, deductions, and tax credits, as well as staying up-to-date on tax code changes. Failure to comply with IRS regulations can lead to severe penalties, including fines and audits, which could damage the firm’s reputation and business operations.

4. State and Federal Laws

Compliance requirements extend beyond federal regulations to include state-specific laws that vary by jurisdiction. CPA firms must understand and adhere to the regulatory standards in their respective states, including those related to client confidentiality, fraud prevention, and consumer protection. Many states have additional requirements for licensing, auditing, and tax services, which firms must meet to operate legally.

5. Continuing Professional Education (CPE)

To maintain licensure and stay current with the latest developments in the accounting field, CPAs are required to complete Continuing Professional Education (CPE). Most states mandate that CPAs complete a specified number of hours of CPE courses every year, covering various topics including changes to accounting standards, tax laws, and ethical practices. These educational requirements ensure that CPAs are knowledgeable about the industry’s evolving landscape and can provide high-quality services to their clients.

In addition to adhering to state and federal laws, CPA firms that perform audits of public companies must also meet specific standards set by regulatory bodies. One such body, the PCAOB, plays a crucial role in ensuring the quality and integrity of audits.

Also Read: How to Conduct an Effective Audit: A Step-by-Step Approach and a Checklist for Success

The Role of the PCAOB (Public Company Accounting Oversight Board)

The Public Company Accounting Oversight Board (PCAOB) was established to oversee the audits of public companies to ensure they are conducted in accordance with high standards. The PCAOB’s regulations are essential for CPA firms involved in the auditing of public companies, providing guidelines that promote transparency, consistency, and reliability in financial reporting.

Key Responsibilities of the PCAOB

The PCAOB is responsible for:

- Setting audit standards for public companies, ensuring that CPA firms follow consistent and reliable audit procedures.

- Inspecting audit firms to ensure they comply with PCAOB standards. This includes conducting regular inspections of firms that audit public companies to assess their compliance with auditing standards.

- Enforcing compliance by taking disciplinary actions against firms that fail to adhere to PCAOB regulations, including fines or sanctions.

Impact on CPA Firms Performing Audits

For CPA firms that audit public companies, adhering to PCAOB standards is not optional. Firms must maintain their independence, objectivity, and ethical standards while following specific auditing procedures to ensure that their audits are accurate and reliable. Non-compliance with PCAOB regulations can lead to significant legal consequences and damage the firm’s reputation.

By ensuring that audits meet the required standards, the PCAOB helps maintain public trust in the financial markets. For CPA firms, compliance with PCAOB regulations is crucial for maintaining credibility and ensuring the continued ability to perform audits for public companies.

Beyond regulatory compliance, CPA firms must also adhere to ethical standards that govern their professional conduct. Upholding these principles ensures the trust and integrity vital to the profession.

Also Read: Financial and Regulatory Compliance Management Software

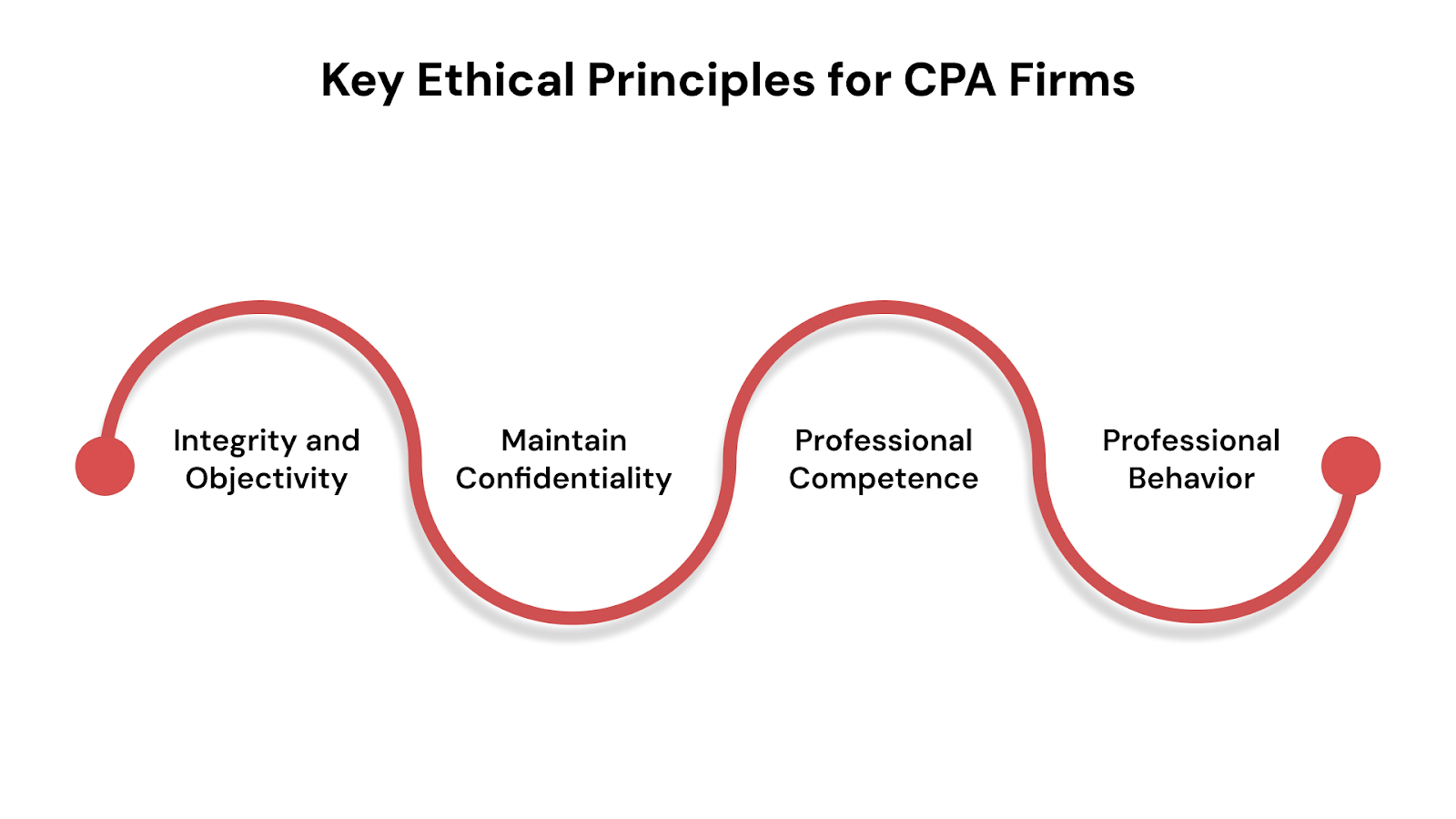

Ethical Standards and Professional Conduct

Ethics are at the core of the accounting profession. CPA firms must not only comply with legal and regulatory standards but also maintain high ethical standards to ensure trust, credibility, and transparency in all aspects of their operations. Professional conduct goes beyond financial reporting and auditing to encompass the integrity of all actions taken by a firm and its employees.

Key Ethical Principles for CPA Firms

The AICPA (American Institute of Certified Public Accountants) outlines several key ethical principles that guide the behavior of CPAs:

- Integrity and Objectivity: CPAs must act with honesty and fairness in all professional and business relationships. They are expected to avoid conflicts of interest and must not let personal or financial interests influence their professional judgment.

- Confidentiality: CPAs must safeguard client information and not disclose it without proper consent, except when required by law. This is especially important in today’s digital world where data breaches can severely harm both the firm and the clients.

- Professional Competence and Due Care: CPAs are required to maintain the necessary knowledge and skills to provide services competently. This includes staying current with changes in regulations, standards, and technologies.

- Professional Behavior: CPAs must comply with relevant laws and regulations and avoid any conduct that might discredit the profession. This includes refraining from actions that could cause harm to clients, colleagues, or the firm’s reputation.

While understanding the key ethical principles is essential, CPA firms must also be prepared to confront and manage the ethical challenges that can arise in everyday practice.

Addressing Ethical Challenges

Even with strong regulations in place, CPA firms often encounter situations where ethics can be tested, a conflict of interest with a client, pressure to overlook discrepancies in financial statements, or the temptation to misrepresent information. These dilemmas can arise in daily practice and, if mishandled, quickly affect trust and integrity.

To navigate these situations, firms need a clearly defined code of ethics that staff understand and apply. Equally important is fostering an environment where team members can openly discuss concerns before they evolve into serious problems.

Ethics and data protection also go hand in hand. Ensuring that client information is managed securely and used appropriately is a critical part of maintaining trust and reducing risk.

For many firms, using a centralized approach to policies and procedures makes it simpler to enforce these standards. A centralized policy and procedure system, such as PolicyOps, enables firms to maintain a single source of truth, making it far simpler to enforce standards, track changes, and demonstrate accountability when it matters most.

Compliance with Data Security and Client Privacy Laws

In today’s digital age, safeguarding client data is one of the most critical compliance requirements for CPA firms. Data protection regulations like HIPAA and other relevant U.S. laws impose stringent rules to ensure the confidentiality, integrity, and security of sensitive client information. Non-compliance can result in significant fines, lawsuits, and loss of client trust, making it essential for CPA firms to prioritize data security.

Ensuring Compliance with Data Protection Regulations

For CPA firms, HIPAA (Health Insurance Portability and Accountability Act) is a key regulation if they handle healthcare-related data. Even if a firm is not directly in healthcare, it may still be subject to HIPAA if it works with clients in the healthcare industry. HIPAA outlines stringent requirements for data protection, including:

- Access controls ensure that only authorized personnel can access sensitive client data.

- Audit logs track and document access to patient data, enabling the detection of any unauthorized activities.

- Encryption ensures that data is protected both during transmission and while at rest.

For CPA firms handling personal financial data, similar standards apply under financial privacy laws, such as the Gramm-Leach-bliley Act (GLBA), which mandates the securing of financial information and provides clear guidelines on disclosing personal financial data to third parties.

Implementing Effective Security Measures

To meet these data protection requirements, CPA firms must implement robust security measures to protect client data. This includes:

- Encryption of all sensitive client data, both for storage and during transmission across networks.

- Multi-factor authentication (MFA) to prevent unauthorized access to client accounts and systems.

- Regular vulnerability assessments and penetration testing to identify and address weaknesses in the firm’s security systems.

- Data backup and recovery systems to ensure that critical data can be restored in case of a breach or system failure.

By adhering to these security practices, CPA firms comply with legal requirements and also demonstrate their commitment to protecting client information, fostering trust, and long-term relationships. While ensuring compliance is critical for the smooth operation of CPA firms, the consequences of failing to meet these requirements can be severe and far-reaching.

The Consequences of Non-Compliance

Non‑compliance in CPA firms carries serious and far‑reaching consequences. In 2024, penalties levied by the PCAOB totaled $37.4 million, the highest in its history, with individual fines ranging from $25,000 to $50,000, and one group of firms fined $3.3 million for audit rule violations. These enforcement measures highlight how quickly lapses in compliance can escalate from costly penalties to restrictions on a firm’s ability to serve certain clients, such as those in the public company space. Just as critical, any breach damages trust, the cornerstone of the profession, making it harder to win or retain clients. Against this backdrop, a strong focus on compliance and internal controls is not just a requirement; it’s a safeguard for a firm’s reputation, stability, and long‑term success.

Also Read: What are the Penalties for HIPAA Violations in 2025?

Best Practices for Ensuring Compliance

To ensure consistent compliance and reduce the risks of legal and financial consequences, CPA firms must establish and maintain structured compliance frameworks. The following best practices provide a solid foundation for fostering a culture of compliance within the firm:

1. Develop Clear Policies and Procedures

A well-defined compliance program starts with creating comprehensive policies and procedures that align with the firm’s services and the relevant regulations. These policies should cover every aspect of the firm’s operations, from client interactions and data security to billing practices and staff conduct. Establishing clear procedures for compliance helps ensure that all staff are aware of their responsibilities and know how to handle situations that may involve regulatory concerns.

2. Regular Audits and Risk Assessments

Conducting regular internal audits and risk assessments is essential to identifying areas of non-compliance before they become major issues. These audits should evaluate all aspects of the firm’s operations, including financial reporting, staff performance, and data protection protocols. By assessing potential risks and monitoring compliance, firms can take timely corrective actions and continuously improve their processes.

3. Ongoing Staff Education and Training

Compliance is an ongoing effort, and staff education is crucial to maintaining high standards. CPA firms should provide continuous training to ensure all employees are up-to-date on the latest regulations, industry standards, and internal procedures. Regular training sessions covering ethics, tax laws, accounting standards, and client confidentiality will empower staff to understand their roles and the importance of compliance in everyday tasks.

4. Implement a Strong Internal Reporting System

Creating a clear reporting mechanism allows employees to report compliance violations or concerns without fear of retaliation. This encourages transparency within the organization and helps identify any potential issues early. A strong internal reporting system ensures that all compliance concerns are addressed promptly, improving accountability across the firm.

5. Partner with Legal and Compliance Experts

Lastly, it is valuable for CPA firms to consult with legal advisors or compliance experts to ensure their compliance programs are up-to-date with current regulations. Expert guidance helps manage complex legal requirements, especially for firms dealing with evolving standards like IRS regulations or state-specific laws. External consultations can provide clarity and assurance that the firm is meeting all necessary standards.

Consistent adherence to these practices will not only protect the firm legally but also enhance operational efficiency and client trust.

How VComply Supports Compliance for CPA Firms

Ensuring compliance is an ongoing task for CPA firms, and utilizing the right tools can simplify this process. VComply offers comprehensive solutions designed to support firms in managing compliance effectively and efficiently. Below are some key features that directly align with the compliance needs of CPA firms:

- Policy Management: VComply helps CPA firms create, distribute, and track policies across the organization. This ensures that all employees are familiar with the latest compliance requirements, and any updates or changes are promptly communicated and acknowledged.

- Audit Management and Tracking: VComply manages the audit process by enabling CPA firms to conduct internal audits and track compliance performance easily. The platform allows firms to document and monitor audit results, helping to identify gaps and implement corrective actions quickly.

- Staff Training and Attestation Tracking: With VComply, firms can assign role-based training with deadlines and track training completion status. The platform ensures that all staff members stay updated on key compliance topics, such as GAAP, IRS regulations, and confidentiality practices.

- Risk and Compliance Task Management: VComply automates the management of recurring compliance tasks, including risk assessments, document reviews, and staff evaluations. The platform helps firms stay on top of daily compliance responsibilities, ensuring nothing falls through the cracks.

- Incident Reporting and Follow-Up: CaseOps allows CPA firms to log any compliance violations or concerns. The system assigns follow‑up tasks, tracks resolution status, and ensures timely action to address issues, maintaining accountability across the firm.

To see how VComply can enhance your compliance efforts and simplify the management of regulatory requirements, book a demo today and discover how our platform can help you manage compliance tasks and reduce risks.

Wrapping Up

For CPA firms, staying compliant is about ensuring long-term success, building trust with clients, and protecting the firm’s reputation. By implementing robust compliance programs and adopting best practices, firms can avoid significant legal and financial risks. As the regulatory environment becomes more complex, staying ahead with proactive strategies and the right tools is essential for maintaining operational integrity and client confidence.

To simplify your compliance efforts and ensure your firm stays on track, consider using technology that automates processes, tracks tasks, and ensures that your team remains informed and accountable. Ready to take control of your compliance? Start your 21-day free trial and experience how our platform can help smooth your compliance management, reduce risks, and improve overall efficiency.