Navigating Mortgage Lenders and Servicers Compliance Requirements

For mortgage lenders and servicers, compliance is not just a regulatory checkbox. It is a daily operational challenge. Managing disclosures, maintaining accurate records, and responding to shifting federal and state rules can feel like trying to hit a moving target. In the post-Dodd-Frank era and amid persistently high interest rates in 2025, these pressures are…

For mortgage lenders and servicers, compliance is not just a regulatory checkbox. It is a daily operational challenge. Managing disclosures, maintaining accurate records, and responding to shifting federal and state rules can feel like trying to hit a moving target.

In the post-Dodd-Frank era and amid persistently high interest rates in 2025, these pressures are only increasing. According to the Office of the Comptroller of the Currency (OCC), 97.6 percent of first-lien mortgages were current and performing at the end of Q1 2025, up from 97.4 percent a year earlier.

The Consumer Financial Protection Bureau (CFPB) remains vigilant. As of January 30, 2025, approximately $19.7 billion in consumer relief and $5 billion in civil monetary penalties had been issued. Servicing continues to be a top enforcement priority, particularly in areas such as fair servicing, loss mitigation, and error resolution.

Key Takeaways (TL;DR)

-

Learn how mortgage lenders must comply with TILA, RESPA, and ECOA regulations effectively.

-

Understand the importance of accurate HMDA reporting to prevent enforcement actions and criticism.

-

Discover strategies to build audit-ready servicing processes with immutable, lifecycle-based documentation.

-

See how technology and CMS platforms automate disclosures, borrower communications, and regulatory updates.

-

Explore best practices for vendor oversight, fair lending, and real-time compliance monitoring.

Key Compliance Requirements Mortgage Entities Must Meet

U.S. mortgage lenders and servicers operate under a layered regulatory framework. These are the primary laws and rules they must comply with in 2025:

Truth in Lending Act (TILA) and Real Estate Settlement Procedures Act (RESPA)

TILA and RESPA govern disclosure and transparency in mortgage transactions. Lenders must provide accurate Loan Estimates, Closing Disclosures, and periodic statements. Errors in APR calculations or failure to meet timing requirements can result in severe penalties. RESPA also regulates kickbacks and requires proper handling of escrow.

Equal Credit Opportunity Act (ECOA) and Fair Lending

ECOA prohibits discrimination in any aspect of a credit transaction. Lenders must ensure that underwriting models, pricing strategies, and marketing practices do not create disparate impacts. Fair lending reviews are standard in CFPB and DOJ audits, especially for digital lending platforms.

Home Mortgage Disclosure Act (HMDA) Reporting

HMDA requires detailed reporting of loan-level data to monitor potential discrimination and assess access to credit. Lenders must submit accurate information on loan applications, approvals, and denials. Errors or omissions in HMDA reports can result in enforcement actions and public criticism.

CFPB’s Mortgage Servicing Rules

Regulations under RESPA (Regulation X) and TILA (Regulation Z) mandate how servicers handle delinquency, foreclosure, and borrower communication. These rules include requirements for early intervention, continuity of contact, and accurate escrow disclosures.

UDAAP Risk (Unfair, Deceptive, or Abusive Acts or Practices)

UDAAP remains a broad enforcement tool for the CFPB. Mortgage companies must avoid deceptive marketing, hidden fees, or servicing practices that mislead or harm consumers by implementing transparent policies and regular staff training.

State-Level Compliance

States like California (DFPI) and New York (NYDFS) have enacted their own servicing rules, often stricter than federal mandates. These may cover licensing, borrower disclosures, and complaint resolution timelines.

Also read: What is Regulatory Compliance?

Compliance Risks Lenders and Servicers Commonly Face

Despite established regulations, mortgage lenders and servicers continue to face recurring compliance challenges. These risks not only lead to regulatory penalties but also damage consumer trust and operational efficiency.

Incomplete Disclosures or RESPA Violations

Failing to provide accurate and timely Loan Estimates or Closing Disclosures can trigger RESPA violations. Common issues include miscalculations, omitted fees, and noncompliance with timing rules.

Improper Foreclosure Practices or Late Fee Mismanagement

Some servicers proceed with foreclosure without properly evaluating borrowers for loss mitigation options. Others incorrectly apply or overcharge late fees, leading to scrutiny from the CFPB and state regulators.

Data Integrity Issues in Loan Servicing Systems

Outdated or siloed systems can result in incorrect escrow calculations, missing payment histories, or inaccurate loan balances. These errors complicate audits and expose firms to enforcement actions.

Fair Lending Violations Due to Algorithmic Bias or Redlining

Automated underwriting or pricing tools may inadvertently produce discriminatory outcomes. If not regularly audited, these models can lead to redlining, disparate treatment, or denial of credit in protected communities.

Lack of Borrower Communication During Loss Mitigation

Failure to engage with borrowers in a timely and consistent manner during delinquency or hardship results in compliance breaches. This includes missed early intervention notices, unresponsive support channels, or incomplete documentation of borrower interactions.

Also read: What is Compliance Risk Management?

Best Practices for Managing Mortgage Compliance

With increasing enforcement activity from the CFPB, state regulators, and investor oversight bodies, mortgage compliance can’t be an afterthought. Leading lenders and servicers are adopting systematic, tech-supported practices that not only reduce regulatory exposure but also increase borrower transparency and operational integrity.

1. Build Disclosure Processes Around Regulatory Timelines and Error Triggers

Federal laws like RESPA and TILA require precise delivery of Loan Estimates, Closing Disclosures, initial escrow statements, and ARM change notices within strict timeframes. Instead of relying on static calendars or manual checks, lenders should integrate real-time regulatory calendars into their LOS (Loan Origination Systems) and servicing platforms.

Use conditional logic to flag exceptions, such as redisclosures triggered by APR increases or new fees, and automatically escalate them to compliance leads before deadlines are breached. Built-in tolerances for fee variances and use version control to retain prior disclosures for audit comparison.

2. Design an Immutable, Lifecycle-Based Audit Trail

To withstand CFPB examinations or investor due diligence, firms need a time-stamped, tamper-proof record of every servicing action—from borrower communication and loss mitigation reviews to escrow adjustments and payoff quotes.

This means tying each action to a user, timestamp, data source, and justification. Instead of scattered emails or loosely tracked Excel logs, use centralized systems that auto-log changes, generate audit-ready PDFs, and retain them in secure repositories aligned with document retention laws (typically 3–7 years).

3. Institutionalize Servicing Rule Updates Through Structured Training and Policy Acknowledgment

Servicing regulations, such as the CFPB’s Mortgage Servicing Rule or state-specific mandates from NYDFS or DFPI, are subject to updates with limited notice. When rules shift, lenders must go beyond updating PDFs or sending email memos.

Publish new procedures in a centralized compliance portal, require digital acknowledgment from relevant staff, and auto-assign training modules with pass/fail checkpoints. Tie acknowledgment data to employee performance files and maintain logs to prove compliance in a personnel audit.

4. Embed Vendor Oversight into Your Operational Risk Program

Third-party servicers and tech vendors handling escrow, subservicing, collections, or borrower outreach can expose lenders to downstream violations. Regulators hold lenders responsible for oversight failures.

Establish a comprehensive vendor risk management framework to oversee partners involved in escrow, collections, subservicing, or borrower communications. Start by collecting and validating key details, such as licensing, financial stability, regulatory history, and data security certifications like SOC 2 or ISO 27001.

Use risk scoring during onboarding to evaluate exposure levels and determine appropriate oversight. Set clear contractual expectations, including breach notification timelines and service-level commitments. Conduct periodic audits or request independent attestations, especially for vendors handling sensitive borrower data. Document all risks and remediation plans in a centralized vendor risk register to maintain visibility and accountability across the relationship lifecycle.

5. Monitor Lending Disparities Using Geographic and Demographic Segmentation

Fair lending violations often stem from unintended disparities in pricing, approvals, or servicing quality across racial, ethnic, or geographic lines. Relying solely on annual HMDA submissions or post-mortem analysis limits response time.

Implement real-time dashboards that segment loan outcomes by borrower demographics and census tracts. Flag anomalies in denial rates, loan terms, or rate spreads using benchmarks aligned with peer institutions. Use regression models to identify drivers of disparity and feed those insights back into policy or underwriting revisions.

Also read: Best Audit Analytics Software for Decision Making

The Role of Technology in Mortgage Compliance

Technology is no longer optional in mortgage compliance. With growing regulatory pressure and operational complexity, lenders and servicers are turning to digital tools to stay ahead of risk, reduce manual errors, and respond to audits with confidence.

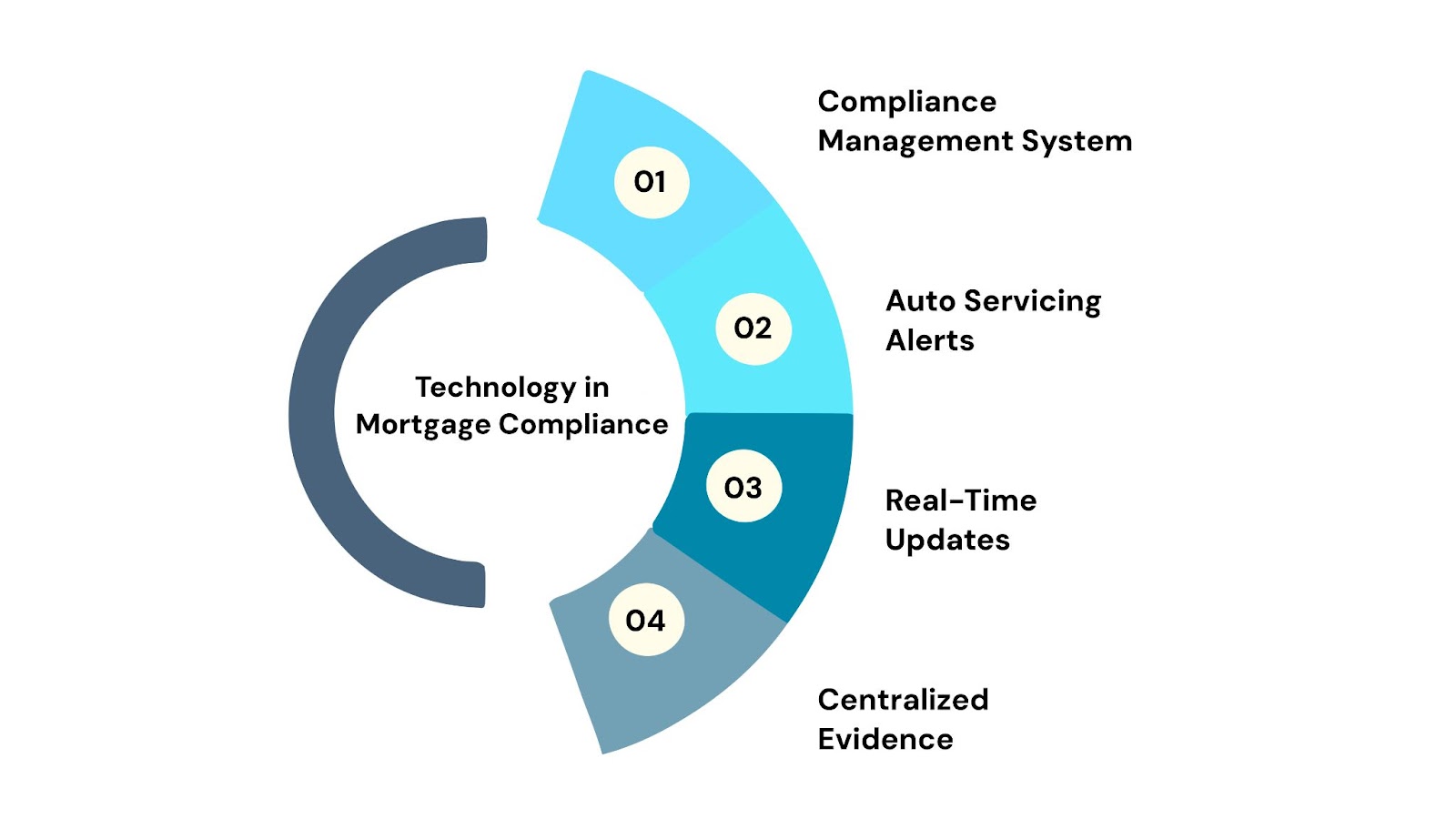

Benefits of Using a Compliance Management System (CMS)

A modern Compliance Management System (CMS) goes far beyond tracking deadlines. It serves as the central nervous system of your compliance function, tying together policies, procedures, licensing, task ownership, and audit trails.

When regulations shift or a borrower enters delinquency, a CMS can automatically route tasks to the right teams, flag overdue actions, and log every step taken. This helps lenders maintain consistent, auditable responses under laws like RESPA or TILA, and reduces the risk of violations tied to missed timelines or unclear accountability.

Automating Servicing Task Checklists and Borrower Notifications

Compliance often hinges on timely communication. Automation ensures that recurring servicing tasks such as payment reminders, delinquency notices, and escrow updates are completed without delay. Pre-built workflows can reduce manual intervention and lower the risk of missed deadlines.

Managing Policy and Regulatory Updates in Real Time

U.S. regulations can shift quickly at both the federal and state levels. A digital compliance platform can push updates instantly, assign review tasks, and track acknowledgments. This ensures that all departments stay aligned with the latest rule changes without relying on fragmented communication.

Centralizing Evidence for CFPB Exams or Internal Audits

During audits or regulatory reviews, documentation gaps can be costly. A centralized system allows lenders and servicers to maintain up-to-date logs of disclosures, borrower communications, and compliance checks. Having a single source of truth improves preparedness and reduces the scramble to locate evidence.

Also read: What Is the Importance of Compliance Technology?

How VComply Supports Mortgage Lenders and Servicer’s Compliance Requirements for 2025

VComply offers a centralized, automation-driven compliance platform that helps mortgage lenders and servicers stay ahead of federal and state regulations. By streamlining disclosures, automating borrower communication tasks, and maintaining real-time audit readiness, VComply minimizes the risk of non-compliance and strengthens operational consistency.

How VComply Supports Mortgage Compliance Requirements:

- Automated Servicing Workflows: VComply automates recurring obligations such as RESPA disclosures, billing notices, and early intervention communications, ensuring that nothing slips through the cracks.

- Centralized Oversight and Documentation: All compliance tasks, borrower communications, and servicing actions are recorded and managed from a single platform, giving compliance leaders complete visibility across all loans.

- Audit Readiness and Evidence Management: Built-in logs and time-stamped records support fast, accurate responses to CFPB audits or internal reviews, eliminating the need to compile documentation manually.

- Case Management for Complaints and Inquiries: From borrower complaints to compliance breaches, VComply logs every incident, assigns owners, and tracks resolution through a clear workflow. Built-in deadlines, reminders, and audit trails ensure timely, transparent handling, reducing risk and improving accountability.

- Real-Time Alerts and Policy Acknowledgment: Compliance updates can be pushed instantly to teams with task assignments and acknowledgment tracking, reducing the risk of outdated processes or missed regulatory changes.

- Scalable for Multi-State Operations: As mortgage lenders and servicers grow or face new state-level compliance requirements, VComply adapts without disrupting existing workflows or increasing manual effort.

Experience how VComply can help your mortgage compliance team reduce risk and stay exam-ready. Start your free trial today.

Final Thoughts

Mortgage compliance is no longer just about meeting minimum requirements; it’s about maintaining trust, reducing exposure, and operating with agility in a fast-changing regulatory environment. From RESPA timelines to state-specific servicing rules, every missed step can trigger penalties, delays, or reputational damage.

Manual tracking and fragmented systems can’t keep up. Lenders and servicers need centralized, scalable platforms that bring oversight, automation, and real-time visibility into one place.VComply helps you manage servicing workflows, borrower communication, policy updates, and audit documentation, without the stress of last-minute scrambles or compliance gaps. Request a personalized demo to see how VComply simplifies mortgage compliance and keeps your team audit-ready, no matter the regulatory landscape.