Money Transmitter Compliance Requirements 2025 Guide

In 2025, compliance is no longer just a checkbox for money transmitters—it’s a critical factor for success. The cost of noncompliance has never been greater. Under 18 U.S.C. § 1960, operating without a license is a federal offense, with penalties of up to $250,000 in fines and five years in prison. And it’s not just smaller businesses feeling the heat—large institutions are being scrutinized too. For instance, in January 2024, City National Bank faced a $65 million fine from the OCC for risk management failures. The takeaway is clear: in today’s high-stakes regulatory landscape, a strong compliance program is more than just protection from penalties—it’s a strategic asset that safeguards your reputation, maintains key banking relationships, and sets the stage for sustainable, long-term growth.

As the global financial landscape becomes more interconnected, money transmitters face increasing pressure to meet complex compliance requirements. With penalties for violations climbing, the cost of non-compliance has never been higher. global AML/KYC penalties surged to $4.5 billion in 2024 alone.

For businesses in the money transmission industry, staying on top of the money transmitters compliance requirements in 2025 is no longer optional. It’s critical to ensure that operations not only meet regulatory standards but also safeguard against significant financial and reputational risks.

In this guide, we’ll explore what businesses need to know about money transmitters compliance requirements in 2025, to stay compliant and avoid costly pitfalls.

Key Takeaways (TL;DR)

-

Money transmitters must strengthen AML/KYC programs to meet 2025 federal and state requirements.

-

FinCEN registration, SAR reporting, and recordkeeping are critical to avoid severe penalties.

-

State licensing, MTMA adoption, and cryptocurrency regulations add complexity to compliance obligations.

-

Cybersecurity, data privacy, and cross-border transaction monitoring are essential for operational integrity.

-

VComply helps automate compliance, manage risks, and maintain readiness across money transmission operations.

Why Compliance Will Be Mission-Critical for Money Transmitters in 2025

In 2025, compliance isn’t just a checkbox for money transmitters; it’s a make-or-break factor. The cost of noncompliance has never been higher. Under 18 U.S.C. § 1960, operating without a license is a federal offense that can result in fines up to $250,000 and prison time of up to five years. And enforcement isn’t limited to smaller players — even large institutions are under scrutiny. In January 2024, City National Bank was fined $65 million by the OCC for lapses in risk management and internal controls, a penalty tied to what regulators described as “unsafe and unsound practices.”

The message is clear: in an increasingly high-stakes regulatory environment, a strong compliance program is no longer just a shield against penalties. It’s a strategic asset, one that protects your reputation, keeps critical banking relationships intact, and lays the foundation for long-term, scalable growth.

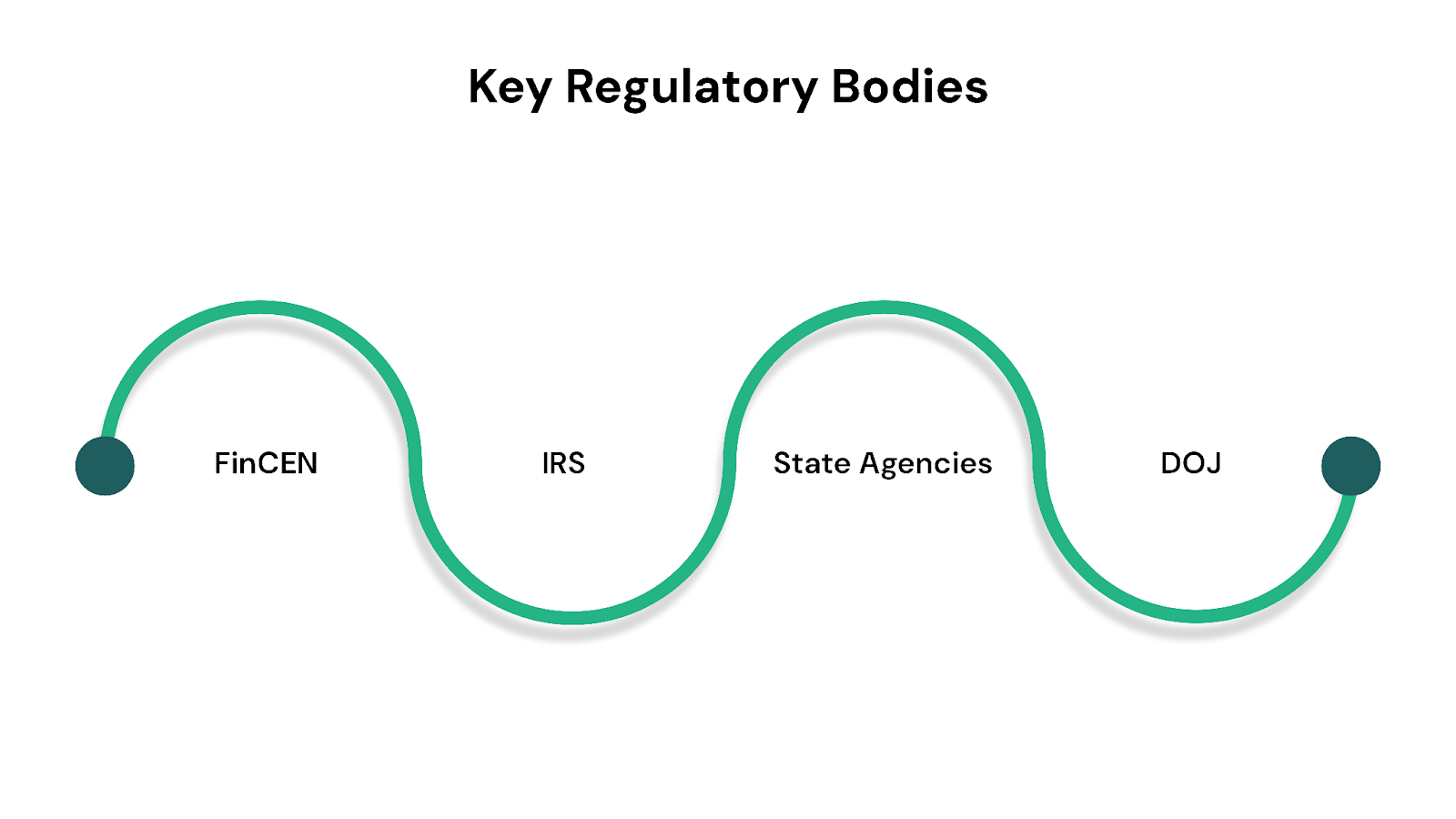

Key Regulatory Bodies Overseeing Money Transmitters

With the increasing complexity of money transmitters compliance requirements in 2025, choosing the right regulatory body can be a challenge. Each agency plays a distinct role, and ensuring you align with all of them requires a deep understanding of their scope and responsibilities.

- Financial Crimes Enforcement Network (FinCEN): FinCEN, a bureau of the U.S. Department of the Treasury, is the primary federal regulator for money transmitters. Money transmitters must register with FinCEN as Money Services Businesses (MSBs) and comply with the Bank Secrecy Act (BSA), which includes Anti-Money Laundering (AML) program requirements, suspicious activity reporting, and recordkeeping.

- Internal Revenue Service (IRS): The IRS enforces tax compliance and certain BSA requirements for MSBs, including money transmitters. The agency also guides on regulatory obligations related to taxation and financial reporting.

- State Regulatory Agencies: Each state requires money transmitters to obtain a state-specific license and comply with local regulations. These regulations often include additional consumer protection, financial, and reporting requirements.

- U.S. Department of Justice (DOJ): The DOJ investigates and prosecutes violations of federal financial laws, including those related to money laundering and unlicensed money transmission.

Read more: Maintaining Regulatory and Compliance Adherence as a Money Transmitter

Essential Money Transmitters Compliance Requirements in 2025

Selecting the right approach to Compliance Requirements for Money Transmitters in 2025 is more complex than ever. With regulations tightening and technology advancing, organizations face the dual challenge of meeting stringent standards while maintaining operational clarity.

Federal Compliance Requirements

Federal Compliance Requirements for Money Transmitters present a complex web of obligations that demand careful attention. With regulatory scrutiny intensifying, organizations must weigh the risks of non-compliance against the operational challenges of meeting each mandate.

FinCEN Registration and Reporting

- Money transmitters must register with the Financial Crimes Enforcement Network (FinCEN) as Money Services Businesses (MSBs).

- Businesses must file Suspicious Activity Reports (SARs) for suspicious transactions and maintain comprehensive transaction monitoring systems.

- Record retention requirements mandate that all transaction records and compliance documentation be kept for at least 5 years.

Anti-Money Laundering (AML) Compliance

- Implementation of a strong Anti-Money Laundering program with written policies and procedures.

- Regular independent reviews of AML programs to identify and address compliance gaps.

- Annual employee training on BSA/AML/OFAC regulations and compliance procedures.

- Deployment of AI-driven transaction monitoring systems to improve the detection of suspicious patterns while reducing false positives.

Know Your Customer (KYC) Requirements

- Improve KYC protocols for thorough identity verification, risk profiling, and ongoing monitoring of high-risk customers.

- Implementation of continuous KYC (cKYC) with dynamic risk assessments and perpetual monitoring.

- For high-risk customers, KYC information must be refreshed annually; for low-risk customers, every 3 years.

- Valid photo ID, proof of address (less than 90 days old), and source-of-funds documentation for high-risk customers.

State Licensing Requirements

State Licensing Requirements for Money Transmitters can be a significant challenge, as each state imposes its own standards, documentation, and approval processes.

Money Transmission Modernization Act (MTMA)

- As of June 2025, thirty-one states have enacted the MTMA in full or in part, creating more uniform standards across states.

- The MTMA establishes consistent requirements for net worth (capital), surety bonds, and permissible investments (liquidity).

- Recent adopters include Virginia (effective 7/1/2026), Mississippi (effective 7/1/2025), and Colorado (expected effective 8/6/2025).

- Money transmitters licensed in at least one MTMA-adopting state account for 99% of reported money transmission activity.

State-Specific Documentation Requirements

- Money Transmitter License (MTL) applications require MSB registration documentation, AML/KYC compliance program details, and surety bond proof.

- Comprehensive business plans detailing financial models, target markets, and operational processes must be submitted.

- Financial statements, including balance sheets, income statements, and proof of adequate capital reserves, are mandatory.

- Background checks for owners, officers, and directors are required as part of the licensing process.

Check this out: Anti-Money Laundering (AML) Policy Template

Virtual Currency and Cryptocurrency Requirements

Virtual currency and cryptocurrency Compliance Requirements for Money Transmitters add another layer of complexity, as regulatory expectations shift rapidly and vary widely across jurisdictions.

Travel Rule Implementation

- 100% of Virtual Asset Service Providers (VASPs) plan to be Travel Rule compliant by the end of 2025, with 85% targeting compliance by H1 2025.

- The Travel Rule requires the collection and sharing of sender and receiver information before transaction execution, including names, account numbers, and addresses.

- VASPs are increasingly enforcing compliance by blocking withdrawals until beneficiary information is confirmed (15.4% in 2025, up from 2.9% in 2024).

- EU’s Transfer of Funds Regulation (TFR) enforcement has led to a 200x increase in Travel Rule-compliant transaction volumes from EU-based firms.

State Cryptocurrency Regulations

- California’s Digital Financial Assets Law (DFAL) takes effect in July 2025, creating a new licensing framework for cryptocurrency businesses.

- Many states have updated their money transmitter laws to explicitly include virtual currency in the definition of money transmission.

- Virtual currency provisions in the MTMA are optional, and several states (including Virginia, Mississippi, and Colorado) have excluded these provisions from their implementations.

- Cryptocurrency exchanges, wallet services, and ATM operators generally require money transmitter licenses in states that regulate virtual currency.

Data Security and Privacy Requirements

Data Security and Privacy Compliance Requirements for Money Transmitters demand a careful balance between regulatory mandates and safeguarding sensitive customer information, especially as cyber threats and privacy expectations continue to rise.

Security Safeguards

- Implementation of comprehensive security measures, including encryption, obfuscation, masking, and use of virtual tokens.

- Access controls, regular backups, and systems for detection of unauthorized access are required.

- Maintenance of logs and personal data for at least one year to enable the detection and investigation of unauthorized access.

- Contracts with data processors must include provisions ensuring implementation of reasonable security measures.

Cybersecurity Compliance

- Annual certification of compliance with cybersecurity regulations, particularly for entities regulated by the New York Department of Financial Services (NYDFS).

- Implementation of transaction monitoring systems that comply with NYDFS Part 504 Rule requirements.

- Regular risk assessments to identify and address potential cybersecurity vulnerabilities.

- Development of incident response plans for addressing potential data breaches or security incidents.

International Compliance Standards

International Compliance Requirements for Money Transmitters introduce another layer of scrutiny, as cross-border operations must satisfy both local and global regulatory expectations that frequently shift.

FATF Recommendations

- Compliance with Financial Action Task Force (FATF) Recommendation 15 updates for virtual assets, including stricter Travel Rule deadlines.

- Implementation of FATF Recommendation 16 requirements for wire transfers and electronic funds transfers.

- Adoption of new cryptocurrency red flag indicators as defined in the FATF guidance.

- Alignment with global standards for beneficial ownership transparency and information sharing.

Cross-Border Transaction Requirements

- Compliance with the Remittance Transfer Rule for international money transfers, including disclosure of fees, exchange rates, and delivery timelines.

- Error resolution and cancellation rights for consumers sending international remittances.

- Improved due diligence for cross-border transactions, particularly those involving high-risk jurisdictions.

- Implementation of blockchain analytics tools to monitor and assess risks in cross-border cryptocurrency transactions.

Enforcement and Penalties

Enforcement and penalties tied to money transmitters compliance requirements in 2025 present significant risks, as regulators have shown little tolerance for lapses and are quick to impose severe consequences for violations.

Regulatory Scrutiny

- Record-breaking penalties for BSA/AML violations, including a $3 billion penalty in 2024 for systemic compliance failures.

- FinCEN imposed a $1.3 billion penalty on a depository institution in 2024, the largest in the history of both FinCEN and the U.S. Department of the Treasury.

- Increased focus on accountability, with mandatory independent monitoring and long-term remediation requirements for non-compliant institutions.

How VComply Can Help Meet Money Transmitters Compliance Requirements in 2025

VComply is a compliance and risk management platform designed to help financial institutions, including money transmitters, streamline and automate complex regulatory requirements. Its suite of features supports organizations in staying ahead of evolving regulations, reducing manual effort, and maintaining strong compliance programs.

Key Features for Money Transmitter Compliance:

- Automated Compliance Management: VComply integrates regulatory frameworks to automate compliance processes, assign tasks, and provide timely updates on regulatory changes, ensuring money transmitters stay current with state and federal requirements.

- Risk Management Tools: The platform enables proactive risk assessment, issue tracking, and mitigation planning, helping organizations identify and address potential compliance threats before they escalate.

- Audit Management: Centralizes audit documentation, automates audit-related tasks, and generates comprehensive reports to streamline the audit process and improve preparedness for regulatory reviews.

- Policy Management: Allows drafting, approval, and distribution of compliance policies through a centralized system, with version control and workflow management to ensure all staff are aligned with the latest requirements.

- Real-Time Dashboards and Reporting: Provides customizable dashboards and real-time reports for continuous monitoring of compliance status and risk exposure, enabling quick responses to emerging issues.

- User-Friendly Interface and Secure Data Management: Offers an intuitive design for easy adoption across teams and strong security features, including advanced encryption and access controls, to protect sensitive compliance data.

VComply’s platform is customized to the needs of financial services, making it a strong fit for money transmitters seeking to automate compliance, manage risk, and maintain regulatory readiness in a dynamic environment. Start a free trial today!

Wrapping Up!

Complying with the money transmitters’ compliance requirements in 2025 is becoming more demanding, with penalties for non-compliance rising. Businesses must be diligent in meeting these regulations to avoid potential risks and costly consequences. Keeping up with these changes is essential for smooth operations and maintaining customer trust. Staying informed and adopting the right compliance practices will help protect your business in the long run.

To simplify your compliance process, explore Vcomply. Our platform offers an easy way to manage and track compliance requirements, ensuring your business stays on top of the latest regulations. Get a free demo with Vcomply today to streamline your compliance management.