Insurance Compliance Framework in the U.S.: A Practical Guide for Modern Insurance Teams

U.S. insurers operate in a complex regulatory environment where overlapping federal and state requirements place sustained pressure on compliance teams and executives. Frequent updates and heightened scrutiny make it difficult to maintain consistent oversight without structured processes.

Research shows that regulatory complexity is linked to a greater share of labor devoted to compliance activities, increasing operational burden across industries, including insurance. In practice, organizations are not just meeting rules; they are dedicating more time and resources simply to keep pace, and documentation gaps can quickly turn routine examinations into prolonged disruptions.

A structured compliance framework shifts the organization from reactive firefighting to a defensible, predictable process. In this blog, we outline a practical U.S. insurance compliance framework you can implement and defend during examinations.

Key Takeaways

- A U.S. insurance compliance framework helps translate regulatory requirements into executable controls, evidence, and accountability.

- Insurance compliance is complex due to state-based regulation, NAIC model variations, and selective federal oversight.

- Strong frameworks focus on control ownership, standardized evidence, and continuous monitoring rather than reactive preparation.

- Most compliance gaps arise from fragmented tracking and a lack of visibility, not regulatory misunderstanding.

- VComply helps insurance teams operationalize and manage compliance frameworks across multiple jurisdictions.

Did you know?

A recent industry report estimated that regulatory compliance requirements now consume between 4% and 6% of gross written premiums in the insurance sector. This translates to $2.5 billion–$3.5 billion annually in regulatory costs due to overlapping reporting, governance, and oversight obligations.

That’s a clear reminder that compliance isn’t just a checkbox exercise; those costs and operational requirements shape how the entire industry functions.

What An Insurance Compliance Framework Means In The U.S.

In the U.S. insurance sector, compliance is not a static obligation. You operate in an environment shaped by state regulators, federal oversight, and continuous regulatory change. An insurance compliance framework gives you a structured way to manage this complexity with consistency, visibility, and defensible outcomes.

Below are the core elements that define an insurance compliance framework in the U.S.:

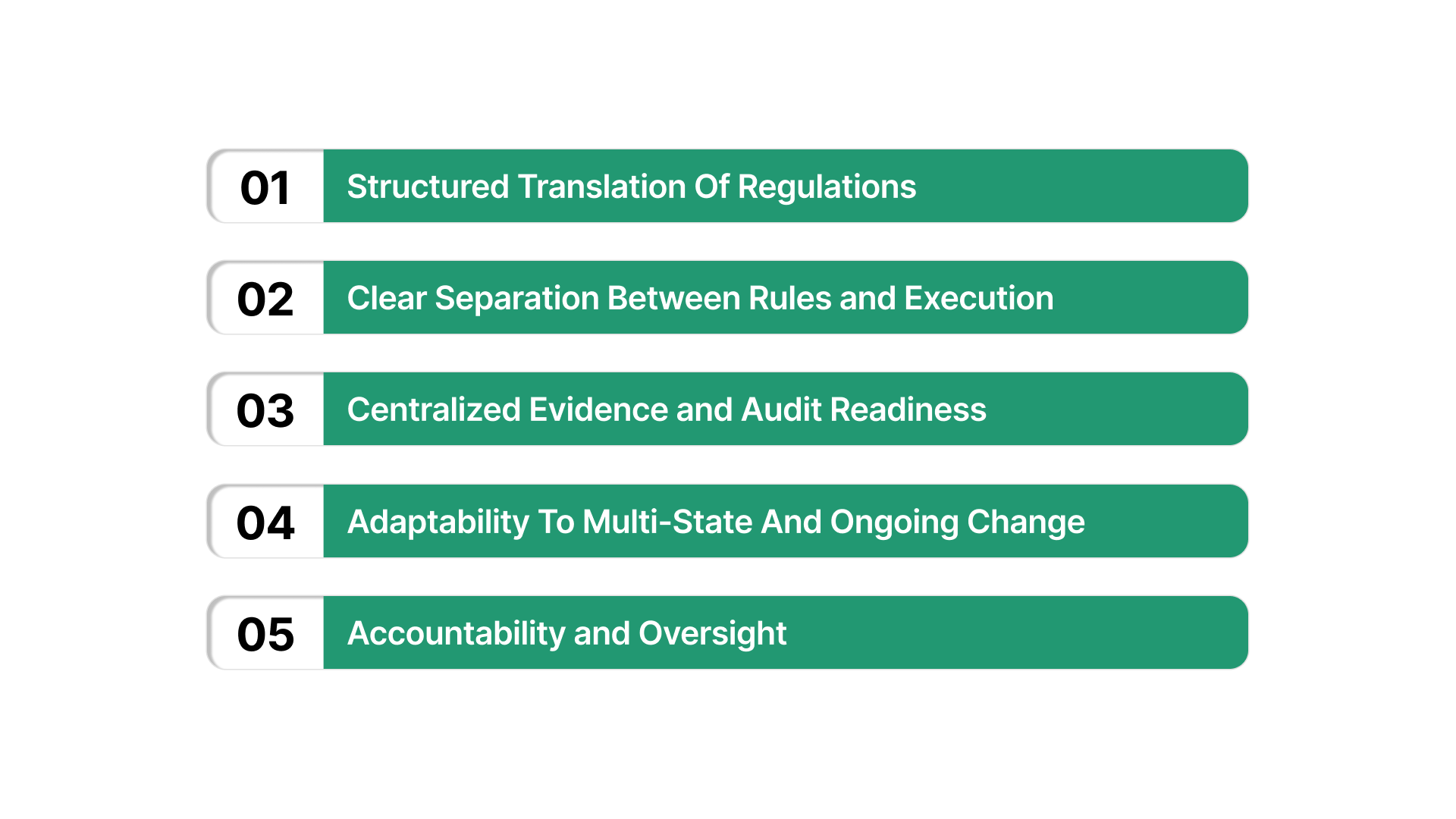

- Structured Translation Of Regulations: A compliance framework converts regulatory requirements into actionable internal policies, controls, and procedures. This ensures obligations are not interpreted differently across teams or business units.

- Clear Separation Between Rules and Execution: Regulations define what you must comply with. A framework defines how you operationalize those requirements through assigned ownership, timelines, and control activities.

- Centralized Evidence and Audit Readiness: A framework establishes clear expectations for evidence collection, retention, and accessibility, allowing you to respond to regulatory exams with confidence rather than urgency.

- Adaptability To Multi-State And Ongoing Change: Insurance compliance frameworks are designed to absorb regulatory updates across jurisdictions without disrupting existing operations or controls.

- Accountability and Oversight: A well-designed framework enables leadership visibility into compliance status, gaps, and remediation progress, strengthening governance and decision-making.

Also Read: Understanding the Purpose of a Policy Summary

Even with a strong insurance compliance framework in the U.S., the industry’s unique regulatory scene sets it apart from most other sectors.

Why Insurance Compliance Is Different From Most Other Industries

Insurance compliance operates under a regulatory structure that is fundamentally different from most regulated industries in the U.S. As an insurance compliance leader, you must explore layered oversight models, fragmented adoption of standards, and heightened scrutiny across operations, products, and partners, all while maintaining continuous exam readiness.

Below are the structural factors that make insurance compliance uniquely complex:

- State-Centric Regulatory Authority: Insurance regulation is primarily enforced at the state level, requiring you to comply with distinct rules, filing requirements, and enforcement practices across multiple jurisdictions.

- Inconsistent Adoption of NAIC Model Laws: While NAIC model laws provide guidance, states adopt, modify, or delay implementation independently, creating compliance gaps that must be actively monitored and reconciled.

- Conditional Federal Oversight: Federal compliance obligations apply based on specific insurance products, distribution models, and risk exposure, requiring precise applicability assessments rather than blanket controls.

- Product And Distribution Complexity: Different lines of business, agents, and third-party administrators introduce varying compliance obligations that cannot be managed through a single, static approach.

- Regulatory Examination Intensity: Insurance regulators expect structured documentation, traceable controls, and defensible evidence, making scalable frameworks essential for sustained compliance confidence.

Understanding an insurance compliance framework in the U.S. highlights why the regulatory scene is uniquely complex and sets the stage for mapping the obligations your organization must cover.

The Regulatory Scene Your Framework Must Cover

Before you can manage compliance effectively, you need a precise understanding of who regulates which parts of your insurance operations. U.S. insurance regulation is layered, conditional, and jurisdiction-specific. Without a clear regulatory map, obligations overlap, ownership blurs, and exam preparation becomes reactive rather than controlled.

The following regulatory layers define what your compliance framework must account for.

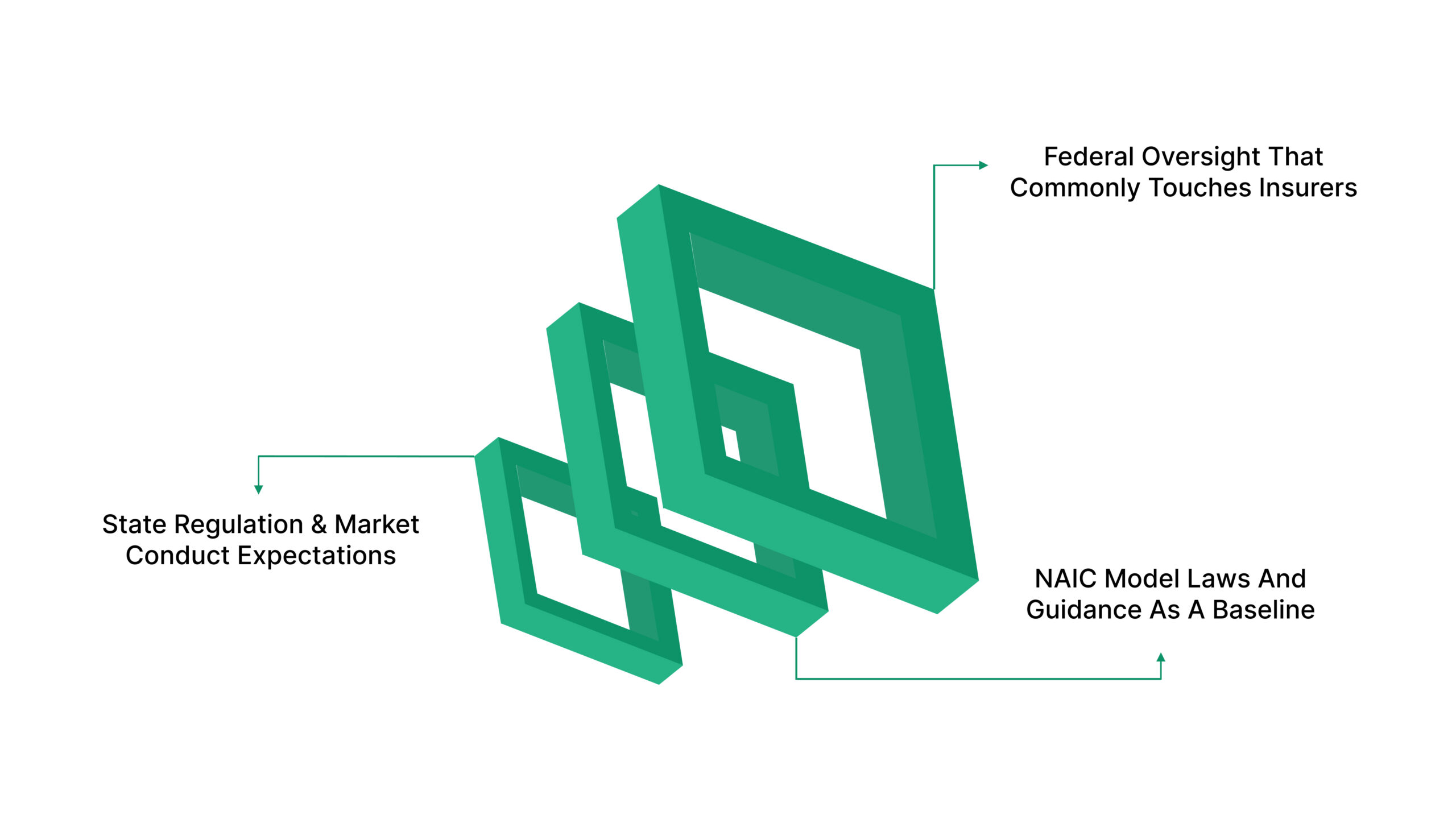

State Regulation And Market Conduct Expectations

State departments of insurance directly influence how you design, operate, and defend your compliance processes. Their oversight extends beyond licensing into how your organization sells products and services to policyholders and resolves claims. Meeting these expectations consistently requires structured controls that scale across jurisdictions without weakening accountability.

Below are the state-level compliance considerations your framework must address:

- Licensing And Authorization Management: You must maintain accurate licensing for entities, products, and producers, while tracking renewals, conditions, and state-specific approvals that often vary by jurisdiction.

- Market Conduct Oversight: State regulators closely examine sales practices, advertising accuracy, claims processing, and complaint handling to ensure fair treatment of consumers and adherence to approved standards.

- Consumer Protection Requirements: Your framework must support timely disclosures, transparent communications, and documented remediation when consumer impact issues arise.

- Multi-State Operational Consistency: Harmonizing controls across states reduces duplication, limits regulatory gaps, and enables you to demonstrate consistent governance despite jurisdictional differences.

- Examination Preparation and Evidence Traceability: Regulators expect clearly documented processes and readily available evidence that links obligations to actions, owners, and outcomes across each regulated state.

VComply’s GRCOps Suite provides a unified view of obligations, controls, and evidence across all states. This helps insurance teams manage licensing, market conduct, and consumer protection requirements consistently while staying audit-ready.

NAIC Model Laws And Guidance As A Baseline

The National Association of Insurance Commissioners plays a central role in shaping regulatory expectations across the U.S. insurance industry. While NAIC model laws provide a common starting point, they are not binding on their own. Your compliance framework must account for how each state interprets and enforces these models.

Below are the practical implications of using NAIC guidance within your compliance framework:

- Model Laws As Reference Standards: NAIC model laws establish baseline expectations for governance, risk oversight, data security, and consumer protection that inform state regulatory priorities.

- State-Specific Adoption Tracking: Each state adopts, modifies, or delays NAIC models independently, requiring structured tracking to avoid gaps caused by incorrect assumptions of uniformity.

- Version Control and Regulatory Alignment: Your framework must align internal policies and controls with the exact version of a model law adopted by each state, not the original NAIC text.

- Regulatory Examination Readiness: During exams, regulators assess compliance against state-enacted requirements, making documented mapping between NAIC guidance and state rules essential.

- Change Monitoring and Impact Assessment: Continuous monitoring of NAIC updates enables proactive assessment of how future state adoption may affect existing controls and compliance obligations.

Federal Oversight That Commonly Touches Insurers

Although insurance regulation is primarily state-driven, certain federal requirements apply based on your products, customer relationships, and risk exposure. These obligations introduce additional scrutiny and demand precise applicability assessments. Your compliance framework must integrate federal controls without disrupting state-level processes or creating fragmented oversight.

Below are the federal compliance areas most insurance organizations must address:

- AML Program Applicability And Scope: Insurance products with cash value or investment characteristics trigger anti–money laundering obligations, requiring documented risk assessments, monitoring controls, and defined escalation procedures.

- Customer Due Diligence Controls: Federal expectations require you to verify customer information, risk assessment profiles, and maintain records that support consistent due diligence across applicable products and channels.

- Sanctions and OFAC Screening Requirements: Where applicable, insurers must screen customers, beneficiaries, and transactions against sanctions lists, with clear procedures for handling potential matches and regulatory notifications.

- Third-Party And Distribution Risk Management: Federal oversight extends to agents, brokers, and service providers, requiring accountability for compliance controls beyond your direct operations.

- Regulatory Examination and Documentation Standards: Federal reviews focus on control effectiveness and traceable evidence, making centralized documentation and clear ownership critical for defensible compliance outcomes.

Also Read: Simplifying Compliance Workflows with VComply

Once you’ve mapped the regulatory scene, your insurance compliance framework in the U.S. must translate these requirements into actionable, enforceable controls that form the core of your compliance program.

Core Requirements Most U.S. Insurance Compliance Frameworks Need

A strong insurance compliance framework moves beyond identifying obligations and focuses on execution. Regulators expect you to demonstrate not only awareness of requirements, but also consistent oversight, documented controls, and verifiable outcomes. These core requirements form the foundation of a framework that withstands regulatory scrutiny and supports continuous compliance.

Below are the operational requirements your framework must address and sustain:

- Licensing and Producer or Entity Oversight: You must document licensing status across states, monitor renewal timelines, manage appointment changes, and record exceptions or lapses with defined remediation actions.

- AML and Financial Crime Controls: Your framework should support a risk-based AML program, including customer risk assessments, ongoing monitoring, escalation workflows, and documented decision-making for regulatory reporting where applicable.

- Data Security and Privacy Controls: Compliance requires regular risk assessments, defined security safeguards, incident response procedures, and maintained evidence that demonstrates control effectiveness during examinations.

- Operational Transparency And Consumer Protection: You need structured processes to track complaints, oversee claims handling, manage required disclosures, and retain records that show fair treatment and regulatory adherence.

- Ongoing Monitoring and Control Validation: Continuous testing and review of controls ensure obligations remain effective as regulations, products, and operational risks evolve.

VComply’s Compliance Ops helps insurance teams map state and federal obligations to clear controls, assign accountability, and centralize evidence. This turns fragmented compliance tasks into a structured, audit-ready workflow.

With the core requirements defined, your insurance compliance framework in the U.S. can be built on strong foundational blocks that connect obligations, controls, and accountability into a repeatable, auditable system.

The Building Blocks Of A Strong Insurance Compliance Framework

Building an effective insurance compliance framework requires more than documenting obligations. You need a repeatable structure that connects regulatory requirements to daily operations, ownership, and measurable outcomes. When these building blocks work together, compliance becomes predictable, defensible, and scalable across states and business units.

Below are the foundational components required to operationalize your insurance compliance framework:

- Regulatory Inventory and Applicability Mapping: Maintain a centralized inventory that identifies applicable requirements by state, product line, legal entity, and third party, with documented rationale for inclusion or exclusion.

- Policy And Procedure Layer: Translate regulatory expectations into clear internal policies and procedures that define how teams execute compliance activities consistently across the organization.

- Controls Library and Control Mapping: Establish a controls library that clearly links each regulatory requirement to specific preventive or detective controls, reducing duplication and coverage gaps.

- Ownership and Accountability Structure: Assign control owners, define responsibilities, and set timelines to ensure accountability for compliance execution and issue resolution.

- Evidence and Recordkeeping Standards: Define what evidence is required, where it is stored, retention periods, and access controls to support regulatory examinations and audits.

- Testing and Monitoring Cadence: Implement scheduled reviews and testing to validate that controls operate as intended and remain effective as regulatory conditions change.

- Issue Management and Remediation Process: Create a structured process to log findings, investigate root causes, implement corrective actions, and prevent recurrence across jurisdictions.

Once you understand the building blocks, implementing your insurance compliance framework in the U.S. in a real organization requires a structured, step-by-step approach that turns theory into consistent, auditable practice.

Step-By-Step: How To Implement The Framework In A Real Insurance Organization

Implementing an insurance compliance framework requires a phased approach that aligns regulatory expectations with operational capacity. A structured rollout helps you reduce disruption, focus on material risk, and build confidence across teams. This approach allows compliance to mature steadily while maintaining readiness for regulatory examinations.

Below is a practical, phased approach to implementing an insurance compliance framework:

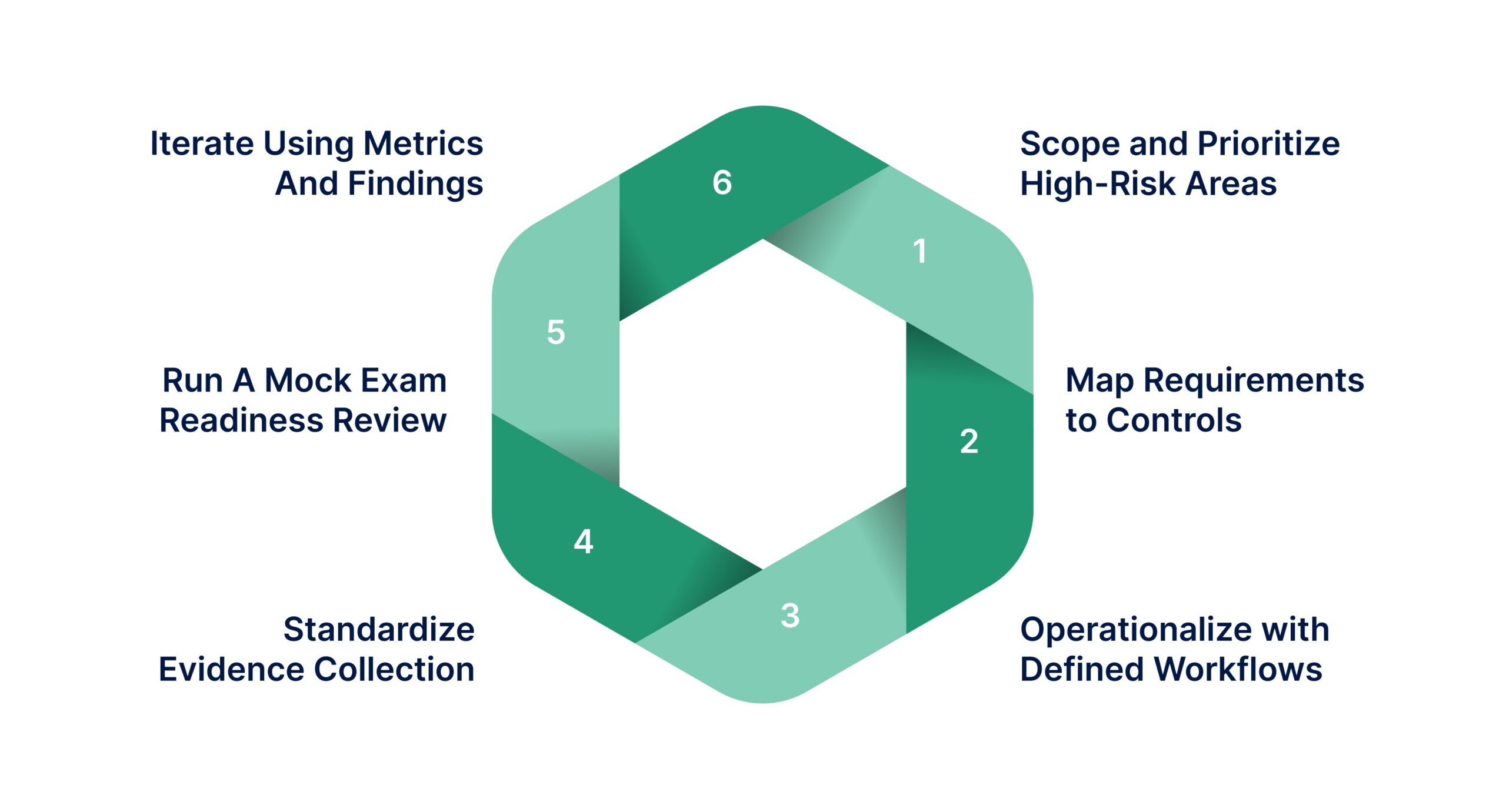

- Scope and Prioritize High-Risk Areas: Begin by identifying products, states, processes, and third parties with the highest regulatory exposure, enforcement history, or operational complexity.

- Map Requirements to Controls: Align regulatory obligations to existing and planned controls to eliminate duplication across states and ensure complete coverage.

- Operationalize with Defined Workflows: Assign tasks, establish approval paths, and set due dates so compliance activities occur consistently and are traceable to accountable owners.

- Standardize Evidence Collection: Define uniform evidence requirements and collection methods to eliminate fragmented documentation and reduce manual follow-ups.

- Run A Mock Exam Readiness Review: Simulate a regulatory examination by compiling expected requests, validating evidence completeness, and identifying gaps before regulators do.

- Iterate Using Metrics And Findings: Track control performance, overdue actions, and repeat issues to continuously strengthen the framework and reduce recurring examination findings.

Also Read: Workflow Automation for Compliance Programs

Even with a clear step-by-step plan, executing an insurance compliance framework in the U.S. in practice often reveals gaps and weaknesses that can undermine effectiveness if not addressed.

Where Most Insurance Compliance Frameworks Break Down

Many insurance compliance frameworks fail not because requirements are misunderstood, but because execution lacks structure and visibility. These breakdowns often surface during regulatory examinations, when gaps in ownership, documentation, or oversight become difficult to defend. Understanding the root causes helps you address weaknesses before they result in findings.

Below are the most common reasons insurance compliance frameworks lose effectiveness:

- Fragmented Compliance Tracking: Reliance on disconnected spreadsheets creates inconsistent data, limits traceability, and prevents a reliable view of compliance status across states and business units.

- Policies Detached From Execution: When policies are not directly linked to controls or employee training, compliance becomes theoretical rather than operational.

- Dispersed Evidence and Documentation: Evidence stored across teams, systems, and third parties increases response time and raises concerns about completeness during examinations.

- Reactive Examination Preparation: Preparing for regulatory exams only after receiving a notice leads to rushed evidence collection and a higher risk of missed obligations.

- Limited Leadership Visibility: Without consolidated reporting, executives lack insight into overdue tasks, unresolved issues, and emerging compliance risks that require timely intervention.

With VComply’s Risk Ops, you can continuously monitor control performance, track overdue actions, and identify emerging compliance risks. This reduces gaps before they escalate into regulatory findings.

Understanding where most insurance compliance frameworks in the U.S. break down highlights why modernizing with automation and reporting is essential for consistent, scalable execution.

Modernizing The Framework With Automation And Reporting

As regulatory expectations intensify, manual compliance processes no longer scale for insurance organizations operating across multiple states. Modernizing your compliance framework with automation and reporting enables consistency, accountability, and continuous readiness when technology supports execution.

Below are the modernization capabilities that strengthen insurance compliance frameworks:

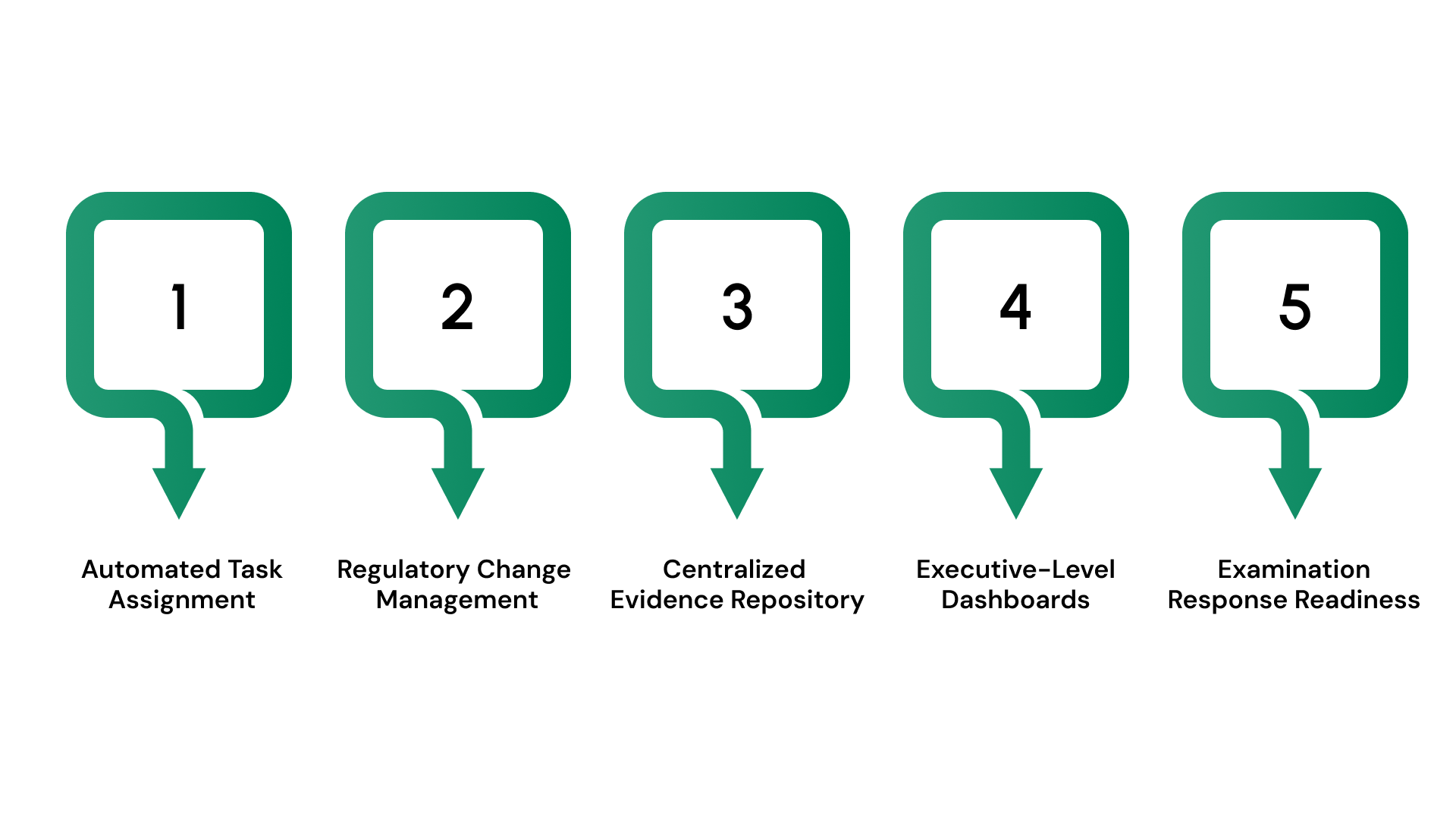

- Automated Task Assignment and Recurring Reminders: Automation ensures recurring obligations, renewals, and reviews are assigned on time, reducing reliance on manual follow-ups and individual memory.

- Regulatory Change Management Controls: Centralized tracking of regulatory updates enables timely impact assessments and coordinated updates to policies, controls, and workflows when state rules change.

- Centralized Evidence Repository Linked To Controls: Storing evidence directly against controls improves traceability, accelerates exam responses, and reduces duplication across teams.

- Executive-Level Dashboards and Reporting: Real-time dashboards provide leadership with visibility into compliance status, risk exposure, overdue actions, and unresolved issues.

- Audit compliance and Examination Response Readiness: Exportable evidence sets and structured response workflows allow you to respond to regulatory requests accurately and efficiently.

Modernizing your processes with automation and reporting lays the foundation for effectively executing an insurance compliance framework in the U.S., a task made easier with platforms like VComply.

How VComply Supports Insurance Compliance Framework Execution

Running an insurance compliance framework day-to-day requires more than documentation. You need a system that connects regulatory obligations, internal controls, evidence, and accountability across states, products, and teams. VComply enables you to operationalize your compliance framework with consistency, transparency, and exam-ready discipline, without increasing manual effort.

Below is how VComply supports execution across the full insurance compliance lifecycle:

- Framework and Obligation Management Across Jurisdictions: VComply allows you to define and manage regulatory frameworks by state, product, and entity, ensuring obligations are clearly mapped, assigned, and tracked. This structure helps you maintain alignment as requirements evolve across jurisdictions.

- Policy Oversight and Attestation Management: The platform enables centralized policy management, version control, and employee attestations, allowing you to demonstrate that regulatory expectations are formally communicated and acknowledged.

- Risk Assessment and Control Alignment: VComply supports linking risks to regulatory obligations and controls, helping you prioritize mitigation efforts and demonstrate a risk-based compliance approach during examinations.

- Audit Readiness and Evidence Tracking: Evidence can be securely stored and directly associated with controls and obligations, allowing you to respond to regulatory exams with complete, traceable documentation.

- Issue and Remediation Workflow Management: Findings, incidents, and compliance gaps can be logged, investigated, assigned, and remediated with full visibility into status and ownership.

- Unified Compliance Operations with The VComply Ops Suite: Through ComplianceOps, RiskOps, PolicyOps, and CaseOps, VComply delivers a connected execution layer that brings obligations, risks, policies, and issues into a single system of record.

Also Read: Why Are Internal Controls Critical for Your Organization?

With VComply supporting day-to-day execution, you can turn your insurance compliance framework from theory into everyday practice. See how continuous oversight and exam readiness become easier to manage in real workflows. Book a demo to understand how it fits your team.

Final Thoughts

An effective insurance compliance framework that U.S. organizations rely on is no longer defined by static documentation or one-time readiness efforts. It is defined by how well you can maintain consistency across states, adapt to regulatory change, and demonstrate control effectiveness at any point in time. Frameworks that are operational, evidence-driven, and continuously monitored reduce uncertainty and support long-term regulatory confidence.

VComply helps insurance organizations move from managing compliance in fragments to executing a unified, scalable framework. By bringing obligations, policies, risks, evidence, and issues into one connected system, VComply enables you to manage multi-state insurance compliance with clarity, accountability, and sustained exam readiness.

Start your free trial today to see how VComply can strengthen your insurance compliance framework execution.

FAQs

Insurance compliance frameworks should be reviewed at least annually and whenever regulatory changes, new products, or operational shifts occur. Ongoing monitoring ensures the framework remains aligned with state requirements, emerging risks, and regulatory expectations between formal review cycles.

Ultimate responsibility typically rests with senior management and the board, while compliance officers oversee execution. Regulators expect clearly defined ownership, documented accountability, and active oversight rather than reliance on informal or distributed responsibility models.

Regulators assess whether controls operate as designed, not just whether policies exist. They review documentation, evidence consistency, issue remediation, and management oversight to determine whether compliance processes are effective and sustainable.

Common requests include licensing records, policies and procedures, control evidence, complaint logs, training records, and remediation documentation. Regulators often focus on traceability between requirements, actions taken, and documented outcomes.

Third-party vendors can introduce compliance risk when they handle regulated activities or data. Insurers are expected to conduct due diligence, define oversight controls, and maintain evidence demonstrating ongoing monitoring of vendor compliance obligations.