ESG Disclosure Requirements in Canada: CSA and OSFI Compliance Explained

ESG disclosure refers to a company’s public sharing of information on how it manages its environmental, social, and governance impacts and risks, including carbon emissions, employee welfare, and ethical practices. With over 90% of S&P 500 companies reporting on ESG factors, transparent and verifiable disclosures have become an industry standard for maintaining market access and a strong reputation.

Canadian companies face mounting pressure to comply with new ESG disclosure obligations under CSA and OSFI guidance, yet significant reporting gaps threaten compliance and competitiveness.

Recent analysis shows 58% of Canadian companies do not detail how sustainability issues affect business strategy, and 70% fail to disclose potential financial impacts of climate-related opportunities, leaving them exposed to regulatory and reputational risks.

Understanding these obligations is critical for leaders to ensure transparency, meet stakeholder expectations, and strengthen market position.

This blog provides a comprehensive, actionable breakdown of ESG Disclosure Obligations under CSA & OSFI Guidance, its requirements, reporting strategies, and risk mitigation.

Key Takeaways (TL;DR)

-

Understand what ESG disclosure obligations mean and why transparent reporting is vital for compliance.

-

Learn how CSA and OSFI frameworks shape Canada’s evolving ESG reporting requirements for businesses.

-

Discover which organizations must comply with mandatory ESG disclosure rules and when they apply.

-

Explore key challenges companies face in meeting ESG obligations and proven best-practice solutions.

-

See how VComply simplifies ESG reporting through automation, real-time analytics, and framework alignment.

What are ESG Disclosure Obligations?

ESG disclosure means a business publicly shares information on how it manages its Environmental, Social, and Governance (ESG) impacts and risks. This covers clear data about actions affecting the environment (like carbon emissions), social matters (such as employee welfare), and governance (including leadership and ethical practices).

These disclosures are sets of data, statements, and documented processes that must be complete and verifiable.

Today, over 90% of S&P 500 companies publish ESG disclosures, making detailed, transparent reporting the industry standard for market access and reputation management.

Below are some specific expectations for Environmental, Social, and Governance (ESG) disclosures as set by evolving CSA and OSFI guidance.

Environmental Disclosure:

You must report accurate data on greenhouse gas (GHG) emissions, broken down by:

- Scope 1: Direct emissions from company-owned operations

- Scope 2: Indirect emissions from purchased energy

- Scope 3: Indirect emissions across the value chain (e.g., suppliers, customers).

Include your calculation methodologies and, where applicable, third-party verification.

Social Disclosure:

This section covers the company’s practices related to workforce safety, employee rights, diversity and inclusion, data privacy, community impacts, and relationships with suppliers. The company is expected to disclose policies, summary data (such as injury rates or workforce diversity breakdown), and describe how these factors are managed and improved over time.

Governance Disclosure:

For governance, the disclosure must address the composition and independence of the board, how executives are held accountable for ESG risks, ethics policies, anti-bribery measures, whistleblower protections, and oversight structures.

For example, names and roles of board committees responsible for ESG oversight, and how often related topics are discussed at the board level.

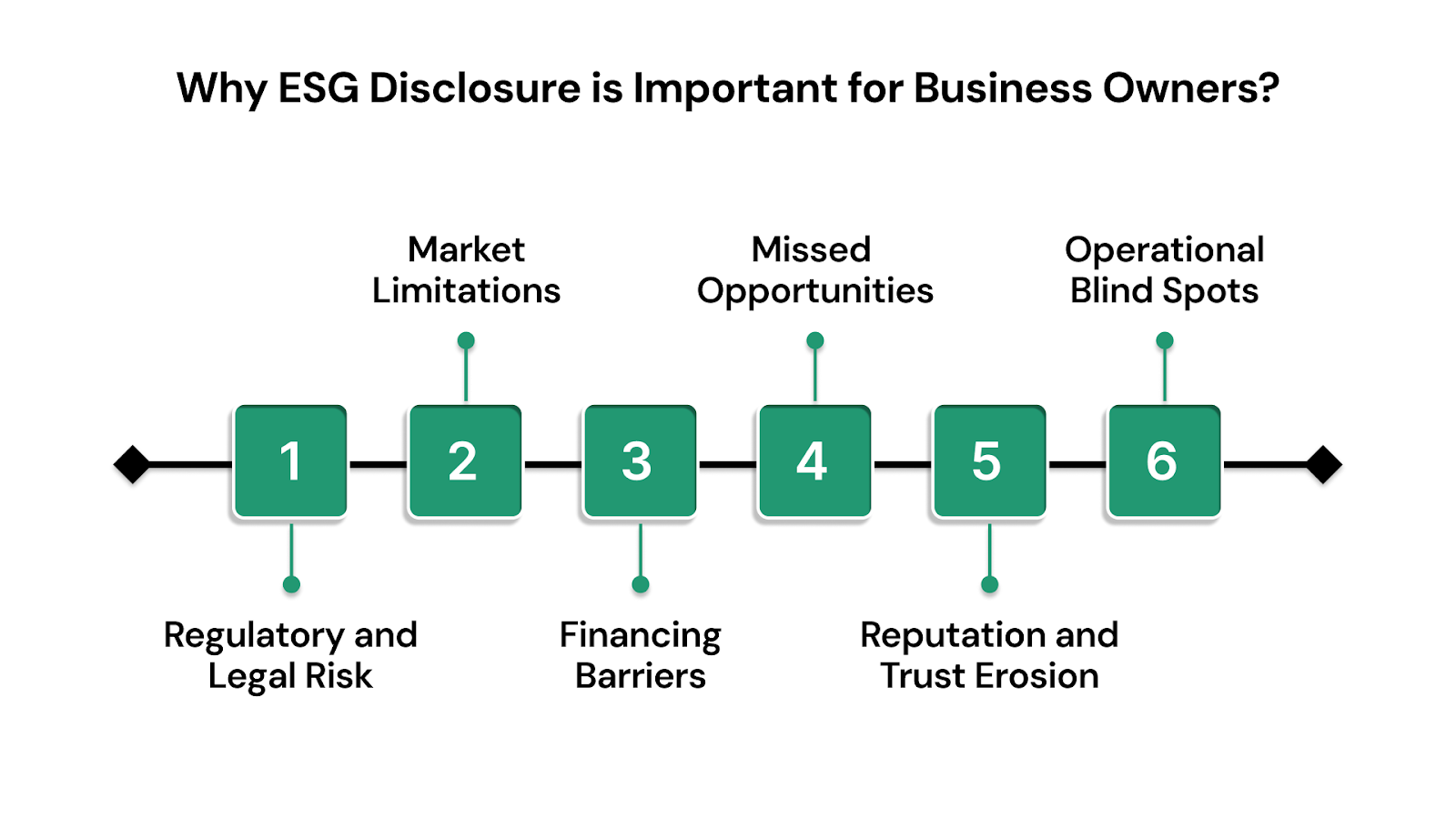

Why ESG Disclosure is Important for Business Owners?

ESG disclosure obligations under CSA & OSFI guidance is now a mandatory requirement for most regulated entities in Canada, including public companies and federally regulated financial institutions, influenced by investor demand, market expectations, and national regulations that align with global standards.

Businesses that fail to comply face multifaceted risks across legal, financial, and reputational domains. These include:

- Regulatory and Legal Risk: The Canadian Securities Administrators (CSA) and the Office of the Superintendent of Financial Institutions (OSFI) are strengthening oversight. Companies submitting inaccurate or non-compliant disclosures may face regulatory penalties and formal investigations.

- Capital Market Limitations: Non-compliance can disqualify businesses from meeting stock exchange ESG listing requirements and can negatively impact Environmental, Social, and Governance scores used by institutional investors to assess risk.

- Financing Barriers: Banks and institutional lenders increasingly incorporate ESG performance into credit evaluations. Weak disclosures may result in higher risk premiums and reduced borrowing capacity.

- Missed Incentive Opportunities: Businesses without valid climate-related disclosures may be ineligible for government clean energy tax credits and grants tied to ESG performance metrics.

- Reputation and Trust Erosion: Stakeholders, including investors, customers, insurers, and supply chain partners, expect publicly verifiable ESG data. No transparency or evidence of greenwashing can cause reputational damage, investor divestment, and reduced market competitiveness.

- Operational Blind Spots: ESG reporting requirements force organizations to assess material risks. Companies that ignore these frameworks may remain unaware of emerging climate, social, or regulatory risks embedded in their operations or supply chains.

Also Read: ESG Reporting Requirements for Renewable Energy Firms

Before understanding the specifics of what must be disclosed, its important to get a clarity of regulatory ecosystem governing ESG reporting in Canada.

Understanding ESG Regulatory Framework: CSA, OSFI, and Global Standards

As of 2025, Canada’s ESG regulatory framework is governed by multiple authorities, each with distinct mandates but increasing coordination.

The CSA require climate and diversity disclosures for public companies, while OSFI enforces specific climate-risk reporting for federally regulated banks and insurers. The new Canadian Sustainability Disclosure Standards (CSDS) are voluntary as of January 2025 but are expected to influence upcoming rules.

The chart below summarizes the principal authorities, their mandates, and the current status of key ESG disclosure initiatives.

| Authority/Standard | Covered Entities | Mandate/Focus | Current Status |

| Canadian Securities Administrators (CSA) | Public companies, investment funds | Securities regulation, ESG-related disclosure for issuers | Paused further mandatory climate and diversity disclosure rules in 2025. |

| Office of the Superintendent of Financial Institutions (OSFI) | Financial institutions (FRFIs), banks, insurers | Risk management, climate risk, ESG in prudential oversight | Maintains climate risk disclosure expectations for FRFIs, aligned with TCFD and ISSB. |

| Canadian Sustainability Standards Board (CSSB)/CSDS | All reporting entities (voluntary for now) | ISSB-aligned sustainability standards and guidance | Published first voluntary Canadian Sustainability Disclosure Standards (CSDS) in Dec 2024, referencing ISSB and TCFD. Not yet mandatory |

| International Standards (TCFD, ISSB) | Referenced by CSA, OSFI, and CSSB | Global frameworks for climate and sustainability reporting | ISSB standards launched globally in 2023; TCFD now incorporated into ISSB. |

Now that you are aware of all the regulatory frameworks it’s impotant to understand which organization is subject to ESG disclosure obligations under CSA & OSFI guidance.

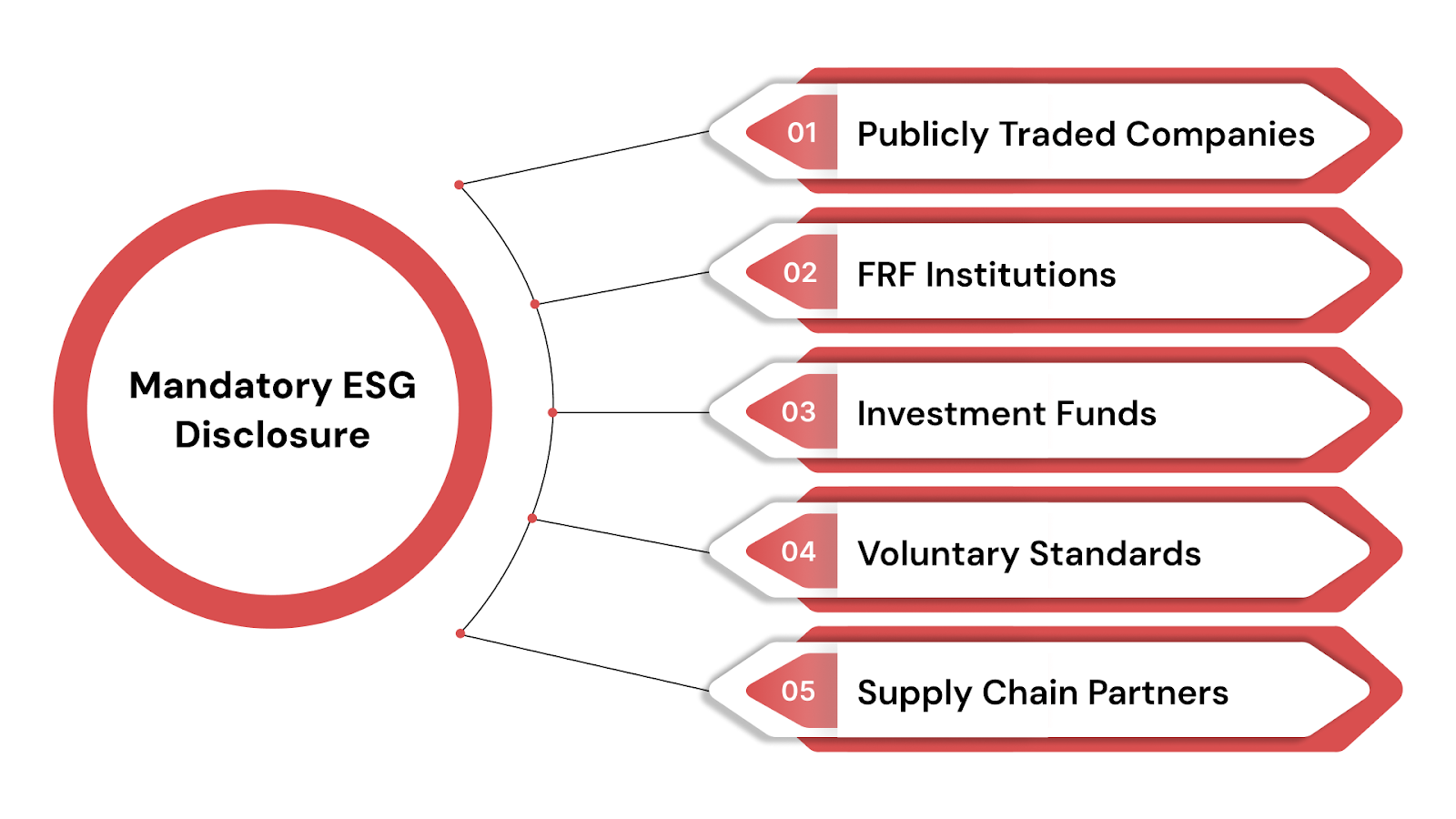

Mandatory ESG Disclosure: Who Must Report and When?

Canada’s mandatory ESG disclosure requirements are targeted, not universal. As of 2025, public companies, investment funds, and federally regulated financial institutions are the primary entities required to report, with each group assigned sector-specific obligations and phased compliance schedules.

While the Canadian Sustainability Disclosure Standards (CSDS) remain voluntary for now, listed companies must comply with existing CSA rules on climate and diversity, and banks and insurers must meet OSFI’s stringent climate-risk disclosure requirements.

Below is a detailed, structure-wise breakdown:

1. Publicly Traded Companies

- Applies to all companies listed on Canadian stock exchanges and other reporting issuers governed by the CSA.

- Must disclose material climate-related risks and board/management diversity, regardless of size or sector, under National Instruments 51-102 and 58-101.

- Phased deadlines apply for new requirements: while proposed climate and diversity rules are paused, existing obligations are actively enforced.

2. Federally Regulated Financial Institutions (FRFIs)

- Covers banks, federal credit unions, and insurance companies regulated by OSFI.

- OSFI’s Guideline B-15 requires FRFIs to disclose climate risk management practices, scenario analyses, and Scope 1 and Scope 2 emissions data; Scope 3 disclosures are encouraged for major institutions.

- Mandatory reporting is active; most requirements must be met within OSFI’s specified annual cycles as of 2024, and there is no pause on enforcement.

3. Investment Funds

- Investment funds classified as reporting issuers fall under CSA ESG mandates.

- Required to report on climate and diversity risks tied to portfolios and governance structures.

- Expect phased compliance, with transitional relief for funds newly captured by regulations.

4. Voluntary Standards: All Entities

- The CSDS are not yet mandatory but encourage all reporting and non-reporting companies to align reporting with emerging ISSB and TCFD standards.

- Early adoption is strategically encouraged, as future regulatory expansion is likely to make such standards compulsory.

5. Supply Chain Partners and Private Companies

- Direct disclosure obligations may not apply unless these companies are part of a listed group or FRFI’s consolidated reporting.

- However, suppliers and service partners are increasingly pressured by customers (public companies, FRFIs) to provide ESG data for value chain assessments.

Many Canadian organizations still face significant roadblocks in meeting ESG disclosure obligations. Addressing these challenges is essential for compliance, credibility, and access to capital.

Challenges in Meeting ESG Disclosure Obligations

Canadian organizations are contending with daily changing mandatory ESG regulations and heightened investor expectations. Below are the key challenges most frequently encountered, with a practical solution:

- Lack of ESG Reporting Readiness: Many organizations are still in the early stages of ESG reporting maturity and may not realize they’re subject to international frameworks like ISSB or CSRD due to global operations or investor demands.

- Confusing and Overlapping Regulatory Standards: Companies have to comply with multiple regimes (CSA, OSFI, CSDS, ISSB, CSRD), risking double reporting and compliance errors.

- Gaps in Financial Quantification of Climate Risks: Organizations often struggle to assign meaningful financial values to climate-related risks, limiting the usefulness of disclosures for investors and internal decision-making.

- Inadequate Assurance and Data Integrity: Many ESG disclosures lack third-party assurance, leaving companies vulnerable to reporting errors and accusations of greenwashing.

- Incomplete Value Chain (Scope 3) Emissions Reporting: Scope 3 emissions, a key focus of emerging standards and investor scrutiny, remain underreported due to data collection difficulties and unclear methodologies.

- Nature and Biodiversity Reporting Lag: Despite growing focus on nature-related risks and frameworks like TNFD, most companies have yet to meaningfully incorporate biodiversity into ESG reporting.

- Poor Integration of ESG into Business Strategy: Over 70% of companies do not fully factor ESG into long-term planning and may treat ESG as “add-on” instead of core strategy.

These challenges highlight the need for a more structured, proactive approach to ESG reporting. The best practices below offer a clear path to closing compliance gaps and aligning with CSA and OSFI expectations.

Best Practices for ESG Disclosure Obligations Under CSA & OSFI Guidance

Below are key best practices to ensure full compliance and long-term reporting success:

1. Disclose Using Recognized Frameworks

Use globally recognized standards (TCFD, ISSB’s IFRS S1/S2), and structure reports by Governance, Strategy, Risk Management, and Metrics & Targets. For banks and insurers (FRFIs), embed all OSFI Guideline B-15 requirements within your ESG reporting, including scenario analysis and board oversight.

2. Materiality Assessment

Regularly identify and update which ESG topics materially affect your business and stakeholders, clearly document your assessment methodology, and explain how climate risks could impact financial performance and company value.

3. Board and Management Accountability

Ensure the board formally oversees ESG risks, make committee structures and meeting frequencies transparent, and link executive pay metrics directly to ESG and climate targets where relevant.

4. Scenario Analysis & Risk Modelling

Conduct and report on scenario analyses of both physical and transition climate risks, disclosing your assumptions, timeframes, and projected business impacts; banks/insurers and CSDS early adopters should move toward quantitative outputs by 2027.

5. GHG Emissions Reporting (Scopes 1, 2, 3)

Track and report Scope 1 and 2 emissions using the GHG Protocol, begin collecting Scope 3 data, and state your calculation boundaries and assumptions, Scope 3 becomes mandatory with CSDS/ISSB alignment by 2027.

6. Maintain Data Integrity and Auditability

Establish internal controls and audit trails for ESG data, ensure consistency across all published reports, and get third-party assurance for emissions and climate data where possible to increase trust.

7. Clear, Consistent, and Stakeholder-Centric Disclosure

Write disclosures in plain language, customize content for investors and other core stakeholders, meet all filing deadlines, and be fully transparent about any data gaps or estimate limitations.

8. Early Adoption of CSDS Standards:

Voluntarily adopt CSDS 1 and CSDS 2 now for climate and ESG disclosures, positioning your company for smooth future compliance and signaling strong sustainability leadership to the market and investors.

Also read: Why Policy Management is the Infrastructure of ESG

Using the right technology can turn ESG disclosure obligation from a manual struggle into a scalable, efficient process.

Simplify ESG Reporting with VComply

VComply is a Governance, Risk, and Compliance (GRC) platform that offers an intuitive, centralized platform designed to help organizations easily manage, track, and report their ESG disclosure obligations under CSA & OSFI guidance.

Key benefits include:

- Centralized Data Management: Consolidate and manage all ESG data in a single, secure platform, ensuring data accuracy and consistency.

- Automated Framework Mapping: Map ESG data to relevant frameworks and standards (e.g., GRI, SASB, TCFD), streamlining compliance efforts.

- Real-time Reporting and Analytics: Generate comprehensive ESG reports and dashboards, providing stakeholders with clear insights into performance.

- Workflow Automation: Automate data collection, approvals, and reporting processes, reducing manual effort and improving efficiency.

With VComply, ESG reporting becomes predictable, verifiable, and regulator-ready. Start your 21-Day Free Trial with VComply today.

Wrapping Up

Canada’s ESG disclosure obligations under CSA & OSFI guidance mandates public companies, financial institutions, and investment funds, along with strong momentum toward compliance with global standards.

To efficiently navigate these requirements, organizations must adopt best-in-class practices, stay agile as rules evolve, and ensure ESG reporting is consistent, credible, and ready for analysis.

Take the next step with VComply. Learn how our GRC platform can simplify and automate your ESG reporting processes. Ensure your renewable energy firm is prepared for the evolving demands of a sustainable future. Request a demo of VComply now and transform your ESG practices.

FAQs

1. What penalties can organizations face if they fail to comply with ESG disclosure deadlines in Canada?

Missing ESG disclosure deadlines can lead to regulatory fines, public reprimands, or delisting for public companies. Delays or incomplete reports may also trigger CSA or OSFI investigations, damaging your company’s reputation and access to capital.

2. How often should ESG data (such as GHG emissions or board diversity) be updated and reported?

ESG data tied to regulatory filings should be updated at least annually, aligned with your fiscal year-end. Many organizations also publish semi-annual or quarterly updates to show progress and maintain transparency with internal and external stakeholders.

3. Do Canadian subsidiaries of foreign companies need to comply with Canadian ESG disclosure requirements?

Yes. If a subsidiary is a reporting issuer in Canada or a federally regulated financial institution, it must meet local ESG disclosure rules, regardless of its parent company’s location. It may also need to align with global standards like ISSB or CSRD, depending on broader reporting obligations.

4. What role do external consultants or assurance providers play in ESG compliance?

Consultants can help design ESG strategies, conduct materiality assessments, and support disclosure preparation. Third-party assurance providers verify data quality—especially emissions and risk modeling—boosting credibility with investors and meeting OSFI or CSA expectations.

5. How can small and medium-sized enterprises (SMEs) prepare for future ESG reporting even if not currently required?

SMEs can begin by identifying ESG factors that affect their operations, customers, or supply chains. Starting with voluntary frameworks and basic metric tracking (like energy use or DEI) builds readiness for future mandates and meets increasing expectations from business partners.