2025 Corporate Transparency Act: Key Compliance Deadlines

The Corporate Transparency Act (CTA) aims to prevent financial crimes by revealing the true owners of companies. As of March 2025, only foreign companies doing business in the U.S. are required to disclose ownership details, with reports due within 30 days of registration. U.S.-formed businesses, however, are exempt from filing CTA reports.

The Economic Crime and Corporate Transparency Act (CTA), effective since January 1, 2024, represents one of the most significant regulatory shifts for US businesses in decades.

Mandating more than 32 million entities, primarily small businesses, to provide beneficial ownership information to the Financial Crimes Enforcement Network (FinCEN), the CTA is designed to prevent criminal activities, including money laundering and terrorist financing.

Companies face civil penalties of $500 per day for violations and criminal penalties up to $10,000 and two years in prison for non-compliance. Understanding and adhering to the CTA is vital for organizations not just to avoid these severe penalties, but also to safeguard reputational standing and operational continuity in a stricter regulatory climate.

This blog outlines the recent changes in the 2025 Corporate Transparency Act and key reporting obligations mandated by the 2025 CTA.

Key Takeaways (TL;DR)

-

Learn how the 2025 Corporate Transparency Act reshapes beneficial ownership reporting for foreign entities.

-

Understand why CTA compliance is vital to avoid steep financial penalties and reputational damage.

-

Discover key 2025 CTA updates, including narrowed reporting scope and accelerated filing deadlines.

-

Explore practical strategies to ensure smooth, ongoing compliance with FinCEN’s BOI requirements.

-

See how VComply simplifies CTA compliance through automation, real-time dashboards, and secure data management.

What Is the Corporate Transparency Act (CTA) 2025?

The Corporate Transparency Act (CTA) is a U.S. law aimed at exposing the real people behind companies. Its core purpose is to prevent money laundering, tax evasion, and other financial crimes by ending the use of anonymous shell companies.

2025 reshaped the Corporate Transparency Act (CTA) more than any prior year. After a ping-pong of injunctions and deadline resets early in the year, the U.S. Treasury and FinCEN issued an interim final rule (IFR) in late March that removed beneficial-ownership reporting for U.S. companies and U.S. persons. Today, only “foreign reporting companies”—entities formed under non-U.S. law but registered to do business in a U.S. state or tribal jurisdiction—must file beneficial ownership information (BOI) with FinCEN, and on revised deadlines. A final rule is expected later in 2025 following a public comment period.

If you’re a U.S.-formed company, the headline is simple: under the IFR now in effect, you are exempt from BOI reporting (and you don’t need to update or correct any BOI previously filed). If you’re a foreign entity registered to do business in the U.S., you still have to report BOI under the CTA on an accelerated timeline

These foreign entities must report who owns or controls at least 25% of the company. For those who were registered before March 26, 2025, the deadline to file was April 25, 2025. Any new foreign company registering after that must submit its report within 30 days of registration. While many small U.S. businesses are now exempt, foreign-owned companies operating in the U.S. must stay compliant to avoid legal trouble and penalties.

Let’s break down why meeting these reporting obligations isn’t optional, and what happens if your business ignores them.

Why Compliance With CTA is Important?

Complying with the 2025 Corporate Transparency Act is important for companies because the statute directly addresses the risks of money laundering, terrorist financing, and tax evasion that often exploit the anonymity of business ownership.

For foreign companies registered in the United States, strict adherence to the CTA is required. The consequences for non-compliance are severe and can be both financial and legal, with penalties that are cumulative and extend to individuals within the organization.

The specific impacts include:

- Civil penalties of $500 per day for each day a violation persists, which can quickly escalate if non-compliance is prolonged.

- Criminal fines as high as $10,000 and imprisonment for up to two years for intentional or willful violations of reporting requirements.

- Direct exposure of company officers and beneficial owners to personal liability affects both business continuity and individual reputations.

- Potential damage to the business’s reputation, reduced investor trust, and difficulties securing banking or investment services, if a public record of enforcement action is established.

Now that you understand the basics, it is essential to understand the specific regulatory changes introduced to the Corporate Transparency Act (CTA) and economic crime rules in 2025.

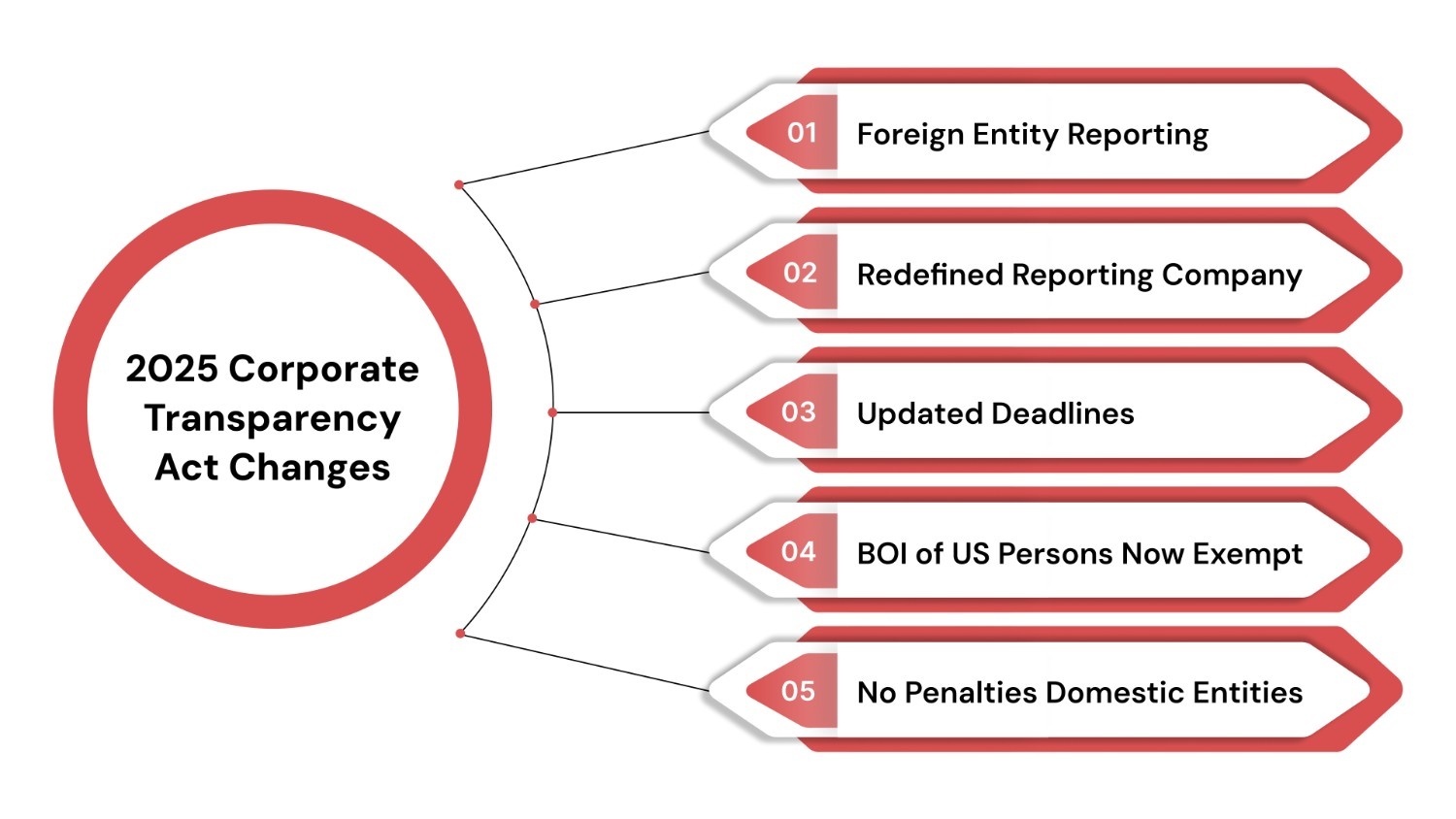

Compliance Changes under the 2025 Corporate Transparency Act

The 2025 amendments to the Corporate Transparency Act fundamentally narrowed the law’s application, directly impacting which business entities must comply with beneficial ownership reporting. Effective March 26, 2025, only companies established under foreign law and registered to do business in a US state or tribal jurisdiction are classified as “reporting companies” for CTA purposes.

Some of the key changes introduced in the 2025 Corporate Transparency Act are:

- Reporting Scope Restricted to Foreign Entities: U.S.-formed entities no longer need to report BOI; only foreign entities registered to do business in the U.S. must file with the Financial Crimes Enforcement Network (FinCEN).

- Redefined “Reporting Company”: Only foreign companies that have filed registration documents with the US Secretary of State qualify as “reporting companies” under the CTA.

- Updated Deadlines: Foreign reporting companies registered before March 26, 2025, must submit initial BOI reports by April 25, 2025. Those registering after this date have 30 days from approval to file.

- BOI of US Persons Now Exempt: Only non-US beneficial owners are subject to reporting for qualifying foreign companies. U.S. persons are not required to be disclosed, and reporting companies controlled solely by U.S. owners are generally exempt.

- No Future Penalties for Domestic Entities: The Department of the Treasury has formally suspended enforcement actions and penalties for U.S. companies or their beneficial owners relating to the CTA.

The following table provides a clear and detailed overview of key deadlines and penalty applicability for business entities under the 2025 Corporate Transparency Act amendments.

| Entity Type | Initial Filing Deadline | Are Penalties Applicable? |

| Domestic entities (U.S.-formed LLCs, corporations) | Not required | No |

| Foreign entities registered before 3/26/2025 | April 25, 2025 | Yes |

| Foreign entities registered on/after 3/26/2025 | 30 days from registration approval | Yes |

With the core compliance basis established, it is essential to outline exactly what is required of businesses still covered by the Corporate Transparency Act following the 2025 changes.

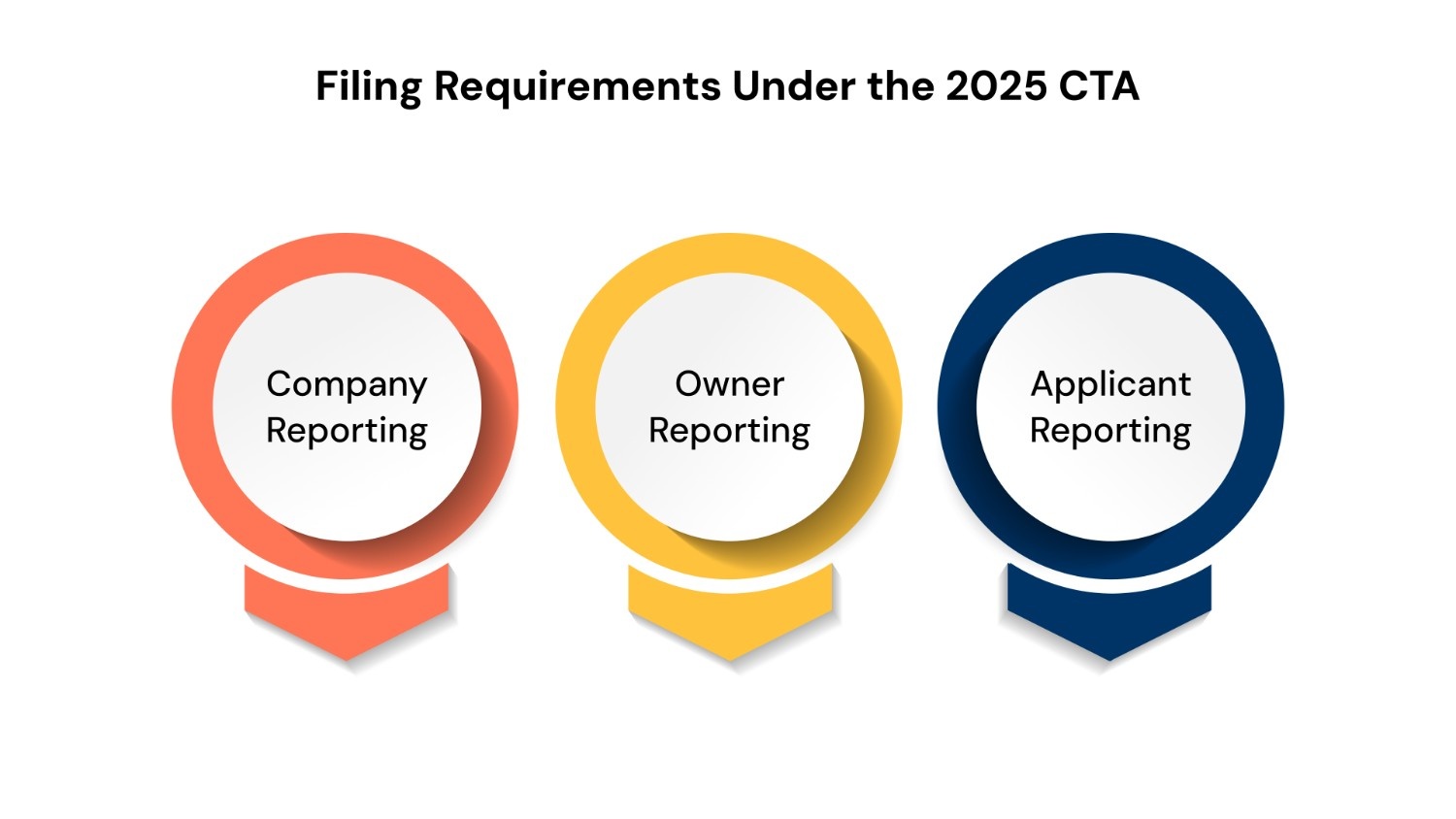

What Are the Filing Requirements Under the 2025 CTA?

Under the 2025 Corporate Transparency Act, only entities formed under foreign law and registered to do business in the United States by filing documents with a state or tribal authority must file beneficial ownership information (BOI) reports.

To ensure compliance, each foreign reporting company must gather and submit comprehensive information about itself, its beneficial owners, and, if the company is newly registering, its company applicants.

Here’s a breakdown of all the data points required for filing under the 2025 Corporate Transparency Act:

1. Reporting Company Information

The BOI filing must include key identifiers about the entity itself:

- Full legal name of the foreign entity

- Any trade, “doing business as” (DBA), or assumed names used in the United States

- Principal business address in the United States

- Jurisdiction (the country and US state) where the entity is formed and registered

- Taxpayer Identification Number (TIN/EIN) assigned by the IRS, or if unavailable, a non-U.S. tax ID number

2. Beneficial Owner Information

For each non-US person who directly or indirectly owns or controls at least 25% of the entity, must be provided:

- Full legal name

- Date of birth

- Residential address (no business or company addresses allowed)

- Unique identifying number from an acceptable document (such as a passport, non-U.S. national ID, or driver’s license), plus the issuing country or state

- Image or scan of the identification document (e.g., passport or national ID photo page).

3. Company Applicant Information

It is required only for foreign entities newly registering in the US in 2025 or later:

- Full legal name of the individual who files or directly oversees the entity’s registration

- Date of birth

- Residential or business address

- Unique identifying number from a government-issued identification document (plus image/scan and the issuing country or state).

Note: If any information about beneficial owners or applicants changes, the reporting company must file an updated BOI report within 30 days of the change.

Let’s now understand the practical steps and strategies foreign entities should follow to ensure sustainable compliance.

Strategies to Ensure Compliance under the 2025 Corporate Transparency Act

Staying compliant with the 2025 Corporate Transparency Act requires foreign entities registered to do business in the U.S. to follow a structured, practical approach. The following concise steps make compliance easy, efficient, and reliable for organizations of any size.

- Assign Clear Responsibility: Designate a compliance officer or team specifically responsible for BOI reporting and related compliance functions.

- Keep Entity Records Current: Frequently update and verify company records, ensuring beneficial owner details are accurate and changes are recorded immediately.

- Track Filing Deadlines Proactively: Use digital compliance calendars and automated reminders to manage all initial and update deadlines, reducing the risk of late or missed filings.

- Entity Management Software: Centralize storage of BOI data, monitor deadline alerts, and maintain an audit trail of compliance actions in a secure, cloud-based system.

- Automated Reporting Tools: Use software that connects directly to FinCEN’s electronic submission portal for quick, accurate, and compliant BOI filings.

- Targeted Training Sessions: Deliver compliance training to everyone with BOI responsibilities, including guidance on identifying beneficial owners and documenting regulatory-compliant data.

- Promote Internal Transparency: Create an open environment in which employees are encouraged to report suspected compliance issues or errors without fear of retaliation.

- Maintain Training Records: Keep detailed records of who attended training, topics covered, and communications regarding compliance for potential regulatory review.

By assigning clear responsibility, staying on top of deadlines, and using the right tools, businesses can meet CTA obligations without added stress. Consistency matters more than complexity; small, repeatable actions go a long way. Let’s take a closer look at how these compliance requirements can be handled clearly and consistently, without adding unnecessary layers.

How Does VComply Simplify Compliance With 2025 CTA Reporting?

Meeting the reporting requirements of the Corporate Transparency Act takes more than reminders and spreadsheets. VComply brings structure to the process, helping businesses manage ownership records, track deadlines, and stay ready for changes, without the scramble.

Here’s how it works:

- Automate Governance Processes: VComply automates the entire GRC management process, from policy creation to risk management, ensuring smooth, efficient governance reporting and compliance.

- Comprehensive Dashboards: VComply’s dashboard gives compliance professionals a single view of all CTA-related tasks, deadlines, and document requirements. The system automatically flags critical dates for initial and updated BOI filings.

- Automated Workflow: Approval hierarchies and workflow automation ensure that no BOI update or amendment is missed when there are changes in beneficial ownership or control, maintaining compliance with 30-day correction windows.

VComply not only reduces administrative time and risk exposure but also positions compliance teams to act decisively when new reporting mandates or enforcement criteria are announced by FinCEN or related authorities.

Start your 21-Day Free Trial with VComply today to see how our platform can transform your compliance workflows.

Wrapping Up,

The 2025 Corporate Transparency Act introduces rigorous ownership disclosure requirements, accompanied by serious penalties for non-compliance, and fundamentally reshapes reporting expectations for foreign entities doing business in the US.

Staying ahead of regulatory deadlines and maintaining accurate data are now essential to protect business integrity and reputation.

Get audit-ready compliance with VComply. Automate your reporting, safeguard sensitive ownership data, and ensure you never miss a deadline.

Schedule a demo with VComply to secure your organization’s CTA readiness.

FAQs

1. How will reporting companies be notified of their CTA obligations?

FinCEN and state authorities provide outreach via email, official notices, and website updates. However, ultimate responsibility for compliance rests with each qualifying company.

2. If a company’s beneficial ownership changes but is not reported within 30 days, what is the penalty?

Failure to update BOI within 30 days may result in civil penalties of $500 per day until compliance, and willful violations can trigger additional fines or criminal penalties.

3. Are trusts required to report under the CTA if they hold ownership in a reporting company?

Yes, if a trust directly or indirectly owns at least 25% of a reporting company or exercises substantial control, information about the trust’s beneficial owners (such as trustees or grantors) must be reported.

4. How does the CTA define “substantial control” for beneficial ownership reporting?

Substantial control includes individuals with significant influence over important company decisions, regardless of formal title or direct ownership percentage. Guidance specifies roles such as senior officers or those with authority over significant business functions.

5. What happens if a company is unsure whether it qualifies for a CTA exemption?

The company should conduct a detailed review of the exemption categories provided by FinCEN. When in doubt, it is advisable to consult legal counsel or file a report to avoid potential non-compliance and penalties.