Master AML Data Today and Learn Best Practices to Strengthen Compliance

A single missing data field can be the difference between a clean AML audit and a seven-figure regulatory penalty.

One overlooked data gap can leave millions in illicit funds undetected and expose your organization to crippling enforcement action. Money laundering accounts for an estimated 2–5% of global GDP annually, translating to roughly $800 billion–$2 trillion in illicit value flowing through financial systems each year.

So why does AML data matter? Because it connects customer profiles, transactions, risk scoring, and regulatory reporting into one defensible compliance narrative.

This blog explains what AML data is, why it’s essential for meeting BSA and FinCEN expectations, and the best practices compliance leaders use to strengthen AML outcomes and audit readiness.

Key Takeaways

- AML data quality is critical; accurate, complete, and traceable data underpins every regulatory decision.

- Connected data across the AML lifecycle ensures alerts, investigations, and SARs are consistent and explainable.

- Data retention and decision documentation are essential for exam readiness and regulatory defensibility.

- Traditional AML approaches fail due to fragmented systems, static rules, and weak governance.

- Implementing best practices, governance, traceability, and context preservation strengthens AML effectiveness.

- VComply GRCOps operationalizes AML controls, providing audit-ready workflows, unified data, and actionable insights.

What is AML (Anti-Money Laundering)?

Anti-Money Laundering (AML) refers to the set of laws, regulations, and internal controls designed to stop criminals from turning illegally obtained funds into money that appears legitimate.

In the United States, AML expectations are largely driven by the Bank Secrecy Act (BSA) and related rules, which require financial institutions to detect, monitor, and report suspicious activity that may indicate money laundering or terrorist financing.

AML is not a single tool or system. It is a continuous, data-driven process that connects customer information, transaction behavior, risk assessment, and regulatory reporting into one defensible compliance program.

Regulators assess AML programs based on whether they can consistently demonstrate the following capabilities:

- Identify customers accurately by collecting and verifying identity and beneficial ownership data

- Understand customer risk based on geography, products, behavior, and transaction patterns

- Monitor activity continuously to detect unusual or suspicious behavior

- Investigate alerts with full context, not isolated transactions

- Report suspicious activity (SARs) accurately, completely, and on time

- Prove decisions after the fact through clear documentation and audit trails

How AML Works In Day-To-Day Operations?

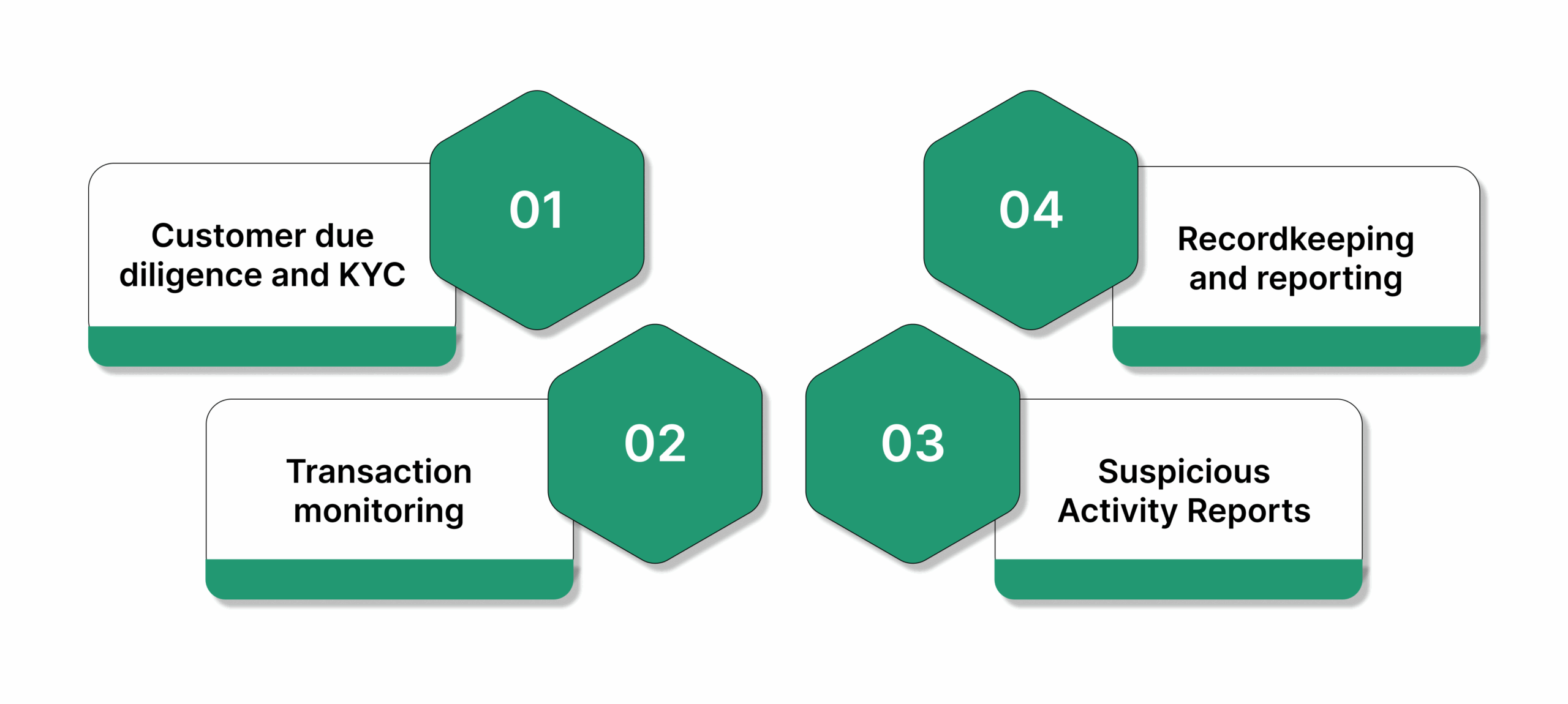

AML programs convert regulatory obligations into concrete workflows that rely heavily on data. Here’s the list of daily operations that AML performs:

- Customer due diligence (CDD) and KYC: Institutions must identify customers, understand the nature and purpose of their relationships, and assign risk ratings that drive the intensity of ongoing monitoring.

- Transaction monitoring: Systems continuously screen transfers, deposits, withdrawals, and payments against rules and models that flag unusual behavior based on customer profiles and historical patterns.

- Suspicious Activity Reports (SARs): When monitoring, alerts, or staff observations indicate potential money laundering, institutions are required to investigate and file SARs with FinCEN, supplying detailed context and supporting data.

- Recordkeeping and reporting: AML rules mandate retention of specific records (for example, transaction data) for multiple years and timely filing of Currency Transaction Reports (CTRs) for large cash activity.

If AML is only as strong as the decisions it produces, then the quality of the data behind those decisions determines whether your program protects the business or exposes it to regulatory risk.

Why AML Data Quality Is Now a Business-Critical Issue?

At a basic level, AML data quality means that information used for customer due diligence, transaction monitoring, risk scoring, and reporting is accurate, complete, timely, consistent, and traceable. When any of these elements break down, the entire AML lifecycle is compromised.

Low-quality AML data does not fail quietly. It shows up in predictable and costly ways:

- False positives overwhelm teams when customer profiles lack context or transactions are misclassified

- True risks go undetected when fragmented data prevents pattern recognition across accounts or products

- SAR filings become inconsistent due to missing transaction history or unclear alert logic

- Exams and audits stall when teams cannot explain how risk decisions were made

The weakest points in AML data typically occur at handoffs between systems and teams:

| AML Stage | Common Data Quality Issue | Resulting Impact |

| Onboarding | Incomplete or unverified customer data | Weak risk profiling from day one |

| Monitoring | Inconsistent transaction labeling | Excess alerts and missed patterns |

| Investigation | Missing historical context | Slower, inconsistent case decisions |

| Reporting | Poor data lineage | SARs that cannot be defended in exams |

What makes this business-critical is the compounding effect. Weak data at onboarding inflates alerts during monitoring, slows investigations, and ultimately undermines regulatory reporting. Fixing these problems after the fact requires costly remediation, additional staffing, and prolonged regulatory oversight.

This is why AML data quality is now closely tied to regulatory outcomes, operating costs, and executive accountability.

Once it’s clear that weak data can compromise the entire AML program, the next step is understanding exactly which data matters, when it’s used, and how it supports regulatory decisions.

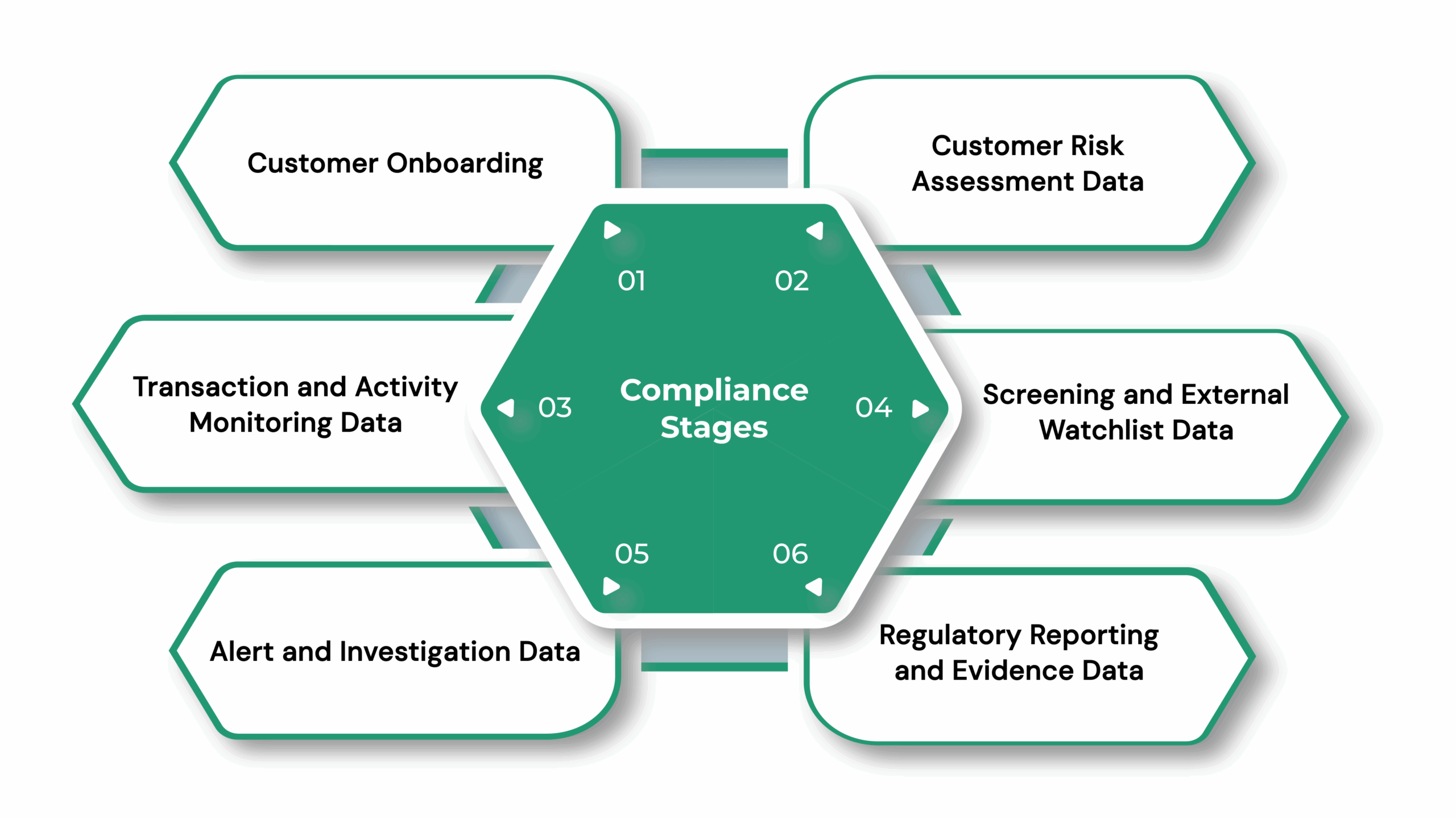

Types of AML Data Across Key Compliance Stages

AML does not rely on a single dataset. It depends on multiple, interconnected data types that support customer risk assessment, transaction monitoring, investigations, and regulatory reporting.

Each compliance stage uses different data, and failures in one stage directly weaken the next. Below are given core data types based on compliance stages:

1. Customer Onboarding and Due Diligence Data

This is the foundation of the AML program. Errors here affect every downstream control. This data determines the initial risk rating and defines what “normal behavior” looks like. Incomplete or outdated onboarding data leads to inaccurate risk profiles and misaligned monitoring rules.

Key data elements include:

- Legal name, address, date of birth, and government-issued identifiers

- Beneficial ownership information for legal entities

- Customer type, industry, geography, and expected activity

- Verification status and supporting documentation

2. Customer Risk Assessment Data

Risk scoring data determines how closely a customer is monitored over time. Risk assessments drive alert thresholds, escalation paths, and review frequency. Poorly documented or inconsistent risk data makes it impossible to justify monitoring decisions during exams.

Key data elements include:

- Inherent risk factors (industry, jurisdiction, products used)

- Behavioral indicators derived from transaction history

- Risk scoring logic and weighting

- Risk review dates and approvals

3. Transaction and Activity Monitoring Data

This data supports the detection of unusual or suspicious behavior. Transaction data must be complete and linked across accounts and products. Fragmented or misclassified transactions result in high false positives and missed suspicious patterns.

Key data elements include:

- Transaction amount, frequency, type, and channel

- Counterparty information and account relationships

- Time stamps and geographic indicators

- Normalized transaction codes across systems

4. Screening and External Watchlist Data

This data identifies known or emerging risk indicators. Screening data must be current, well-matched, and auditable. Outdated lists or unclear matching logic weaken enforcement defenses and increase regulatory exposure. It includes:

- Sanctions lists (e.g., OFAC)

- Politically Exposed Person (PEP) data

- Adverse media and negative news indicators

- List update timestamps and match logic

5. Alert and Investigation Data

This data captures how potential risks are reviewed and resolved. Regulators expect a clear decision trail from alert generation to resolution. Missing context or undocumented decisions often result in examination findings. It includes:

- Alert triggers and rule or model references

- Supporting transaction and customer context

- Investigator notes and decision rationale

- Escalation actions and approvals

6. Regulatory Reporting and Evidence Data

This data supports regulatory filings and post-exam reviews. Reporting data must be accurate, complete, and retrievable. Inability to reproduce SAR decisions or source data is treated as a control failure.

Key data elements include:

- SAR narratives and supporting documentation

- Filing dates, acknowledgments, and amendments

- Data lineage linking SARs to source transactions

- Retention status and access controls

Once data flows correctly through these stages, institutions must preserve it long enough to prove compliance during audits and investigations.

What is Data Retention in AML and Why is it Important?

In AML, data retention means keeping customer, transaction, and decision records long enough and in a form that allows regulators to fully reconstruct past actions. Under U.S. Bank Secrecy Act (BSA) requirements, many AML records must be retained for at least five years, including customer due diligence files, transaction records, alerts, investigations, and SARs.

When retention fails, AML controls fail even if monitoring systems worked as designed. Poor retention creates immediate problems in real examinations:

- Investigators cannot access the original data behind an alert

- Rule or model changes overwrite historical logic

- Case notes exist, but approvals or evidence are missing

- SARs cannot be traced back to source transactions

Strong AML programs treat retention as part of decision integrity, not an afterthought. Effective retention ensures records are:

- Stored for the full regulatory period

- Protected from alteration

- Searchable without manual reconstruction

- Linked from source data to alert to SAR

This is what allows compliance teams to answer the most important examiner question with confidence:

“Show us how this decision was made.”

While retention rules create a compliance safety net, most institutions still struggle with outdated tools that can’t deliver reliable data in real time.

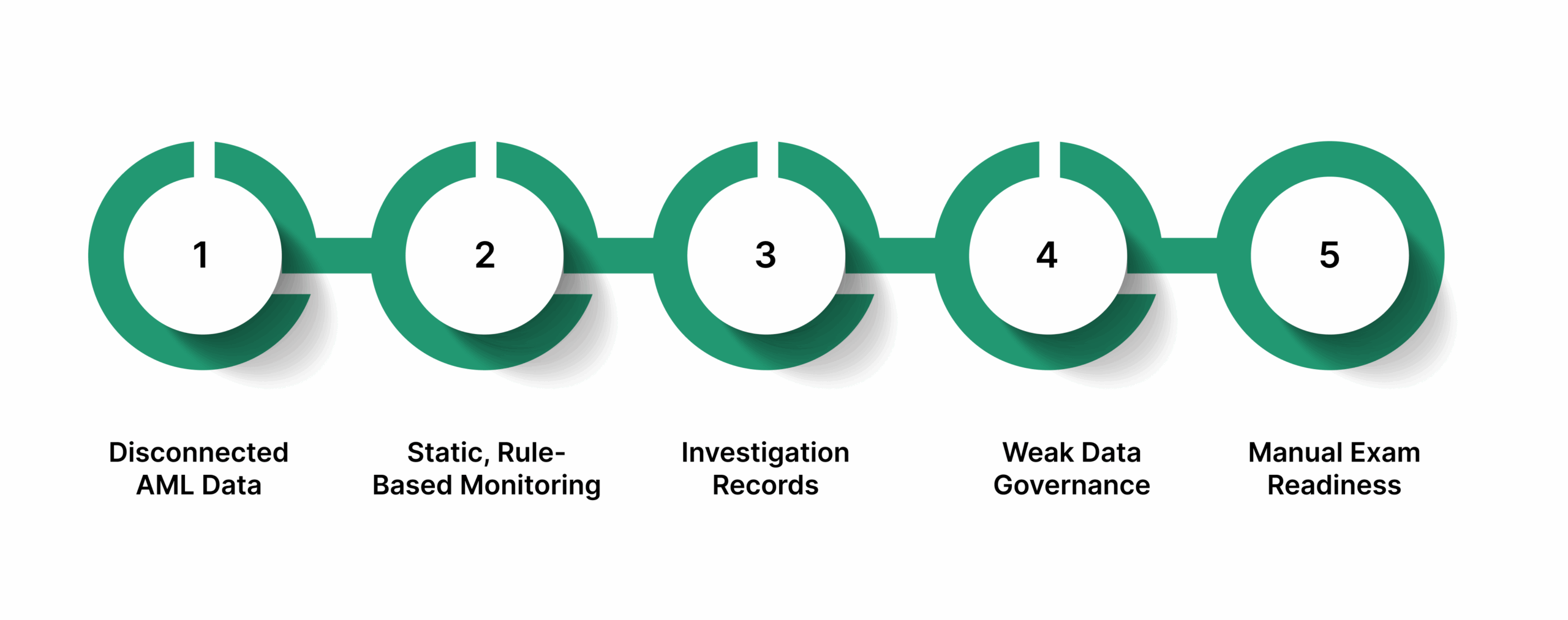

Where Traditional AML Approaches Break Down

Traditional AML frameworks were built to detect suspicious transactions, not to explain how risk decisions were made over time. As data volumes grow and enforcement actions become more granular, these legacy approaches expose predictable weaknesses, such as:

Disconnected AML Data

Customer profiles, transactions, alerts, and investigations often exist in separate systems. This fragmentation prevents teams from showing how customer risk influenced alert thresholds or investigative decisions, weakening the audit trail that regulators expect.

Static, Rule-Based Monitoring

Fixed thresholds fail to adapt to changing customer behavior or emerging typologies. The result is excessive false positives, delayed escalation of real risk, and an inability to explain why alerts triggered under earlier rule versions.

Incomplete Investigation Records

Case outcomes are documented, but the supporting data, analyst reasoning, and approvals are inconsistently captured. During exams, institutions can show conclusions but struggle to prove decision integrity.

Weak Data Governance

Ownership of AML data is unclear, quality checks are reactive, and rule or model changes lack version control. This creates gaps in accuracy, consistency, and accountability across the AML lifecycle.

Manual Exam Readiness

Preparing for regulatory reviews requires pulling data from multiple sources and recreating histories. This increases response time, operational stress, and the risk of adverse findings.

Also Read: Why “AML on Paper” No Longer Satisfies Regulators

Once traditional AML approaches break under regulatory scrutiny, the path forward becomes clear: stronger AML outcomes depend on how data is governed, connected, and used, not just collected.

Best Practices to Strengthen AML Data and Insights

Strengthening AML data is not about adding more tools or generating more alerts. It is about ensuring that every AML decision is supported by accurate, complete, and explainable data, from onboarding through regulatory reporting.

High-performing AML programs focus on a small set of disciplined practices.

1. Treat AML Data as a Controlled Asset

AML data must be managed with the same rigor as financial or security data. This means clearly defining ownership, validation rules, and quality checks across customer, transaction, and investigation data. Teams that formalize data governance reduce inconsistencies that often surface during exams.

Key focus areas include:

- Standardized customer and transaction data definitions

- Ongoing data quality monitoring, not one-time fixes

- Clear accountability for data accuracy and completeness

2. Connect Data Across the AML Lifecycle

Strong insights come from context, not isolated data points. Best-in-class programs ensure that customer risk profiles, transaction behavior, alerts, investigations, and SARs are logically connected. This allows teams to see how risk evolves over time and explain decisions with confidence.

When data is connected:

- Alerts are reviewed in the customer context

- Investigations reflect historical behavior, not single events

- SARs are traceable back to the original data sources

3. Preserve Decision Context, Not Just Outcomes

Regulators expect institutions to show why a decision was made, not just what was decided. Leading AML teams capture the full decision trail data used, analyst reasoning, approvals, and supporting evidence—at the time of review.

This practice:

- Improves consistency across analysts

- Reduces reliance on memory during exams

- Strengthens regulatory defensibility

4. Design for Explainability from the Start

AML insights must be understandable to examiners, auditors, and senior leadership. This means documenting rule logic, risk scoring methods, and investigative thresholds in plain, reviewable terms. Explainable data reduces friction during regulatory interactions and internal reviews.

Best practices only deliver value when they are embedded into daily workflow; this is where most AML programs struggle to move from intent to execution.

How VComply Helps Operationalize AML Best Practices

VComply is a US-based, cloud-native GRC platform designed to help regulated organizations manage compliance, risk, policy, and incident workflows with full traceability.

For AML teams, VComply’s GRCOps does not replace transaction monitoring systems; it operationalizes the controls, data governance, documentation, and accountability regulators expect around AML decisions.

Instead of managing AML processes across disconnected tools, VComply provides a structured system of record that ties data, decisions, ownership, and evidence together.

By centralizing and linking AML processes, GRCOps transforms fragmented workflows into consistent, defensible, and auditable practices:

- Unified AML Governance: Connects compliance obligations, risk assessments, policies, and investigations in one oversight layer. CXOs and compliance leaders gain real-time visibility into AML program effectiveness and exposure.

- Audit-Ready Documentation: Maintains a clear trail for every alert, investigation, decision, and approval, reducing reliance on spreadsheets or scattered records.

- End-to-End Traceability: Ensures all data from customer onboarding and transaction monitoring to SAR filing is linked, versioned, and easily retrievable, supporting regulatory examinations.

- Operational Consistency: Standardizes workflows, approvals, and policy adherence across teams, helping AML controls function reliably across all business units.

With GRCOps, AML teams can demonstrate compliance with BSA and FinCEN requirements, reduce operational risk, and confidently respond to audits with evidence-backed decisions.

Book a 21-day free trial and see how VComply helps compliance teams operationalize AML best practices with clear ownership, audit-ready documentation, and end-to-end traceability.

Summing Up,

Mastering AML data is no longer optional; it is a regulatory, operational, and business imperative. Organizations that fail to maintain accurate, complete, and traceable AML data risk regulatory penalties, operational inefficiencies, and reputational damage.

From onboarding and risk assessment to monitoring, investigations, and SAR reporting, every stage depends on connected, high-quality data and clearly documented decision-making.

Traditional AML approaches, fragmented systems, static rules, and inconsistent documentation leave gaps that regulators readily identify.

VComply enables organizations to operationalize these practices, ensuring end-to-end traceability, audit-ready documentation, and consistent enforcement of AML controls. By unifying data, risk, policies, and cases under a single GRC framework, compliance teams can transform AML from a reactive obligation into a proactive, data-driven capability.

Get started with GRCOps today to strengthen your AML compliance program, improve data governance, and ensure every AML decision is traceable, defensible, and regulator-ready.

FAQs

AML data should be validated continuously, with formal reviews at least annually or whenever there are significant customer or transaction changes, to ensure risk scores and alerts remain reliable.

No. Automated tools support detection, but human oversight is essential for investigations, contextual decision-making, and regulatory defensibility.

Most AML records, including KYC, transaction data, alerts, and SARs, must be retained for at least five years from the date of account closure or transaction.

Regulators frequently cite incomplete data, missing decision documentation, and poor traceability as the main reasons AML programs fail examinations.

Linking onboarding, transaction, alert, and investigation data ensures end-to-end traceability, reduces false positives, and enables consistent, auditable decisions for regulatory exams.